Customs duties and transfer pricing: can we bring these more in line?

Share this article

Customs duties and transfer pricing valuations used to be broadly in line. Now that they are much more divergent, can we bring together these old friends?

Key Points

What’s the issue?

Brexit has significantly increased the number of cross-border transactions that now fall within the scope of customs duties in the UK. There is often an assumption that the transfer price can be used as the customs value for transfers between related parties.

What does it mean to me?

Customs valuation and transfer pricing outcomes may be divergent, particularly where there are large year end transfer pricing ‘true ups’. Businesses importing goods where the customs value is based on a transfer price should consider whether this approach is compliant from a customs duty perspective.

What can I take away?

Fundamentally, the specific customs valuation approach to pricing at the time of importation must be documented to satisfy HMRC in the event of a customs valuation audit. The new customs advance valuation rulings may remove uncertainty, particularly where there is divergence between these valuations.

Following updates to HMRC customs valuation guidance issued in late 2022, the interaction between transfer pricing and customs valuation is causing businesses that purchase goods for import into the UK increased uncertainty. Internationally, there is also no consensus on how to rationalise the potentially different outcomes arising from applying the two taxes, leading to further challenges for businesses that want to take a consistent global approach. To understand the reasons for this uncertainty, this article explores the similarities and differences between customs valuation and transfer pricing and how the two potential different outcomes can be managed.

Similar but different

On the face of it, customs valuation and transfer pricing have the same purpose: to ensure that goods, and additionally services in the case of transfer pricing, are supplied cross border on a basis that is demonstrably not affected by the relationship between the parties (in customs language) or an arm’s length basis (in transfer pricing language).

In some cases, however, customs valuation and transfer pricing can appear to be in conflict, with what is acceptable for one being unacceptable for the other. The challenge for taxpayers is deciding when and how to reconcile the two and when to accept the need for a separate approach for each. The root of the conflict between the two taxes is the different approaches and tools they use to achieve their aims.

Customs duties, for the most part, are calculated as a percentage of the value of the goods. The value of the goods in the majority of cases is based on the transaction or sales value of the goods. This means that HMRC’s main concern is ensuring that goods are not undervalued.

Transfer pricing aims to ensure that profits are recognised in a territory in accordance with contributions to value creation in accordance with the arm’s length principle. This means that HMRC’s focus from a transfer pricing perspective is that goods and services provided into the UK do not confer a potential advantage in relation to UK tax (e.g. that goods are not overvalued).

Whilst the administrative approach of Customs Authorities continues to evolve, the basis for customs valuation has remained largely static since the introduction of the WTO Agreement on Customs Valuation in 1979. Business models have, however, become more complex since this time with the globalisation of the economy. Transfer pricing guidance has also changed at an accelerated pace in recent years in part in response to this. This has led to a greater chance of divergence between the customs and transfer pricing valuation methods which post Brexit can matter much more in the UK and the EU.

For example, the OECD Transfer Pricing Guidelines on the use of customs valuations stated in 1995: ‘both customs and tax administrations …. generally seek to determine the value of the products at the time they were transferred or imported.’ Even by 2010, however, these words were removed and the OECD recognised: ‘Valuation methods for customs purposes … may not be aligned with the OECD’s recognised transfer pricing methods.’

The potential for difference between the two taxes is further emphasised by WCO commentaries and HMRC guidance, which make clear that whilst a transfer pricing study can be informative for customs purposes, it is not sufficient in isolation to justify the customs value of goods.

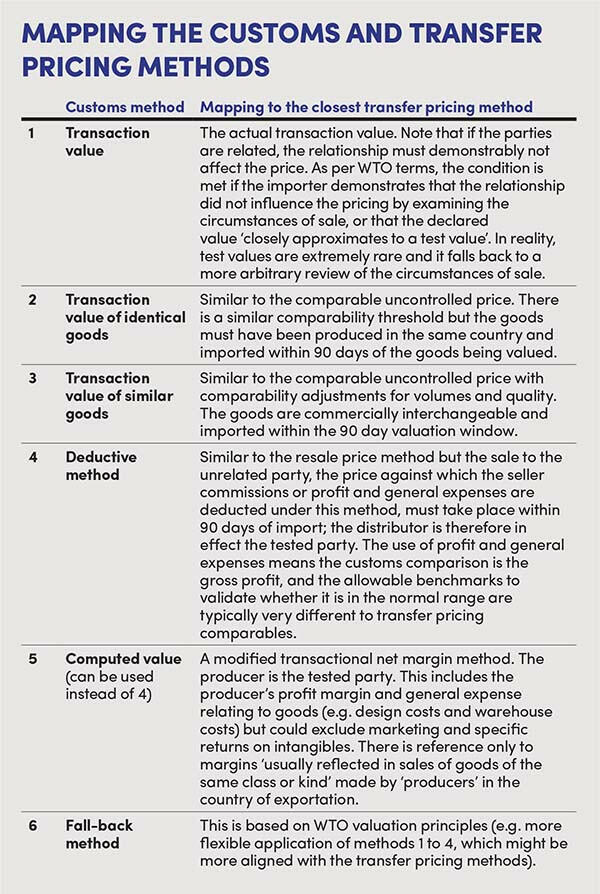

Mapping the customs valuation to transfer pricing methodologies

The use of arbitrary values is expressly forbidden within customs legislation and the WTO valuation agreement. There is a strict hierarchy of methods for determining the valuation of goods, some of which require data within 90 days of the valuation date (date of importation).

Transfer pricing, on the other hand, involves selecting the most appropriate method for the circumstances, with particular reference to the specific functional, assets and risk analysis. In applying a cost plus, resale price or transaction net margin method, the OECD Transfer Pricing Guidelines state, as a general rule, that the tested party (i.e. the party whose margins should be tested) should be the one for whom the method can be applied in the most reliable manner. This is usually the one with the less complex functional analysis. In the equivalent customs methods, the taxpayer has flexibility to choose the method and tested party. The table opposite provides a broad mapping of the customs methods to the transfer pricing methods.

Further divergences in the two valuation standards

Whilst a transaction by transaction approach is encouraged for transfer pricing purposes, the OECD recognises that there are often situations where transactions are so closely linked and/or continuous that it is impractical to evaluate each on a separate basis. In practice, therefore, a cost plus, resale price or transaction net margin method is typically applied across all product lines for a financial period of account. Customs valuation is, however, by its nature applied on a product by product and shipment by shipment basis.

On the question of timing, the OECD recognises both an ex ante (predictive) and ex post (actual returns) basis for demonstrating compliance with the arm’s length principle. The OECD notes, however, that different approaches can lead to different outcomes. This can include discrepancies between the market expectations taken into account in the ex ante basis and the actual outcomes observed in the ex post approach.

Whilst there are different approaches to applying the arm’s length principle, for practical purposes taxpayers often take an ex post approach – perhaps also to avoid potential criticisms of information and judgements made on an ex ante basis. This may lead to a reliance on year end ‘true-ups’ to bring the basis of actual pricing during the year within an arm’s length range based on the final financial results.

Therein lies perhaps the critical issue from a customs valuation perspective. HMRC’s concern is that where it is clear that a transaction value is likely to be adjusted at a later date, and it isn’t known whether that adjustment will be up or down, the value initially declared at import is, from its perspective, arbitrary. In that case, Method 1: the actual transaction value (see table) strictly cannot be applied. It is arguable that there is no transaction value at the point of import, just an estimate (even with a correcting year end true up) and one of the other methods should be applied.

Where potential year end adjustments are anticipated for transfer pricing purposes, it is unlikely, in HMRC’s view, that the actual transaction value at the time of importation will therefore be acceptable as the customs value.

Conclusions: reuniting old friends

Depending on the facts, it may therefore simply be the case that there are different values for goods for transfer pricing and customs purposes; noting the valuations standards. The differences could , for example, be reconciled by identifying and unbundling non-dutiable elements, such as certain intangibles, from the customs value. So the two old friends document their respective positions, acknowledging their differences, and go on to live side by side.

For many, this may be an uncomfortable position which perhaps invites further enquiry and challenge. A potential solution may be to bridge the gap between the two positions by making in-year, prospective price adjustments. This may narrow any year end transfer pricing adjustment, so this is less material. It may then be possible, under customs Method 1, to demonstrate that the actual price is uninfluenced by the relationship between the parties by analysing the circumstances of sale, which will be supported by the data used to inform the prospective adjustments. Data driven tools and strong operational transfer pricing process will assist in the implementation and harmonisation of the two valuations.

In either case, taxpayers would be well advised to review the positions and strategies/options available and document their final positions (supporting separate or aligned positions).

The recent introduction of customs advance valuation rulings could provide taxpayers with some welcome certainty. With HMRC required to provide a decision within 90 days of acceptance of the application for a ruling, advance valuation rulings may offer a practical solution to concerns around potential customs valuation approaches based on a transfer price. Applicants, though, will need to ensure that they have a robust and documented valuation approach to provide the best chance of a ruling being granted.

Particularly in the case of distributors making large year end transfer pricing adjustments, consideration needs to be given to the relationship between their customs and transfer pricing valuations.