Dealing with double taxation

Share this article

Aude Delechat-Patel and Paula Ruffell provide guidance on achieving relief from transfer pricing double taxation

Key Points

What is the issue?

One of the important changes for international tax practitioners is an increase in enquiries over transfer pricing issues – especially into a group’s transfer pricing policies.

What does it mean to me?

Transfer pricing disputes can be complex, lengthy and onerous. Tax authorities will often request a large volume of information from businesses. Companies may choose – somewhat reluctantly – to settle with tax authorities even when this may give rise to double taxation.

What can I take away?

Knowing which options are available can increase the prospects of a successful settlement that eliminates any double taxation.

One of the important changes for international tax practitioners is an increase in enquiries over transfer pricing issues – especially into a group’s transfer pricing policies. Many of these enquiries follow the changes to the OECD Transfer Pricing guidelines (and those from the UN), mandated by the Base Erosion and Profit Sharing (BEPS) Inclusive Framework. This trend is likely to continue as the changes agreed in October 2015 make their way into general practice globally. This view is supported by HMRC’s recent launch of the Profit Diversion Compliance Facility, which sets HMRC’s sights not only on large businesses, but also the mid-market.

Transfer pricing disputes can be complex, lengthy and onerous. Tax authorities will often request a large volume of information from businesses. Companies may choose – somewhat reluctantly – to settle with tax authorities even when this may give rise to double taxation.

Using an example of a typical double taxation dispute, this article presents some key points to help navigate transfer pricing disputes and reach a prompt resolution. The example uses the UK and Canada but the principles apply to many jurisdictions in a very similar way.

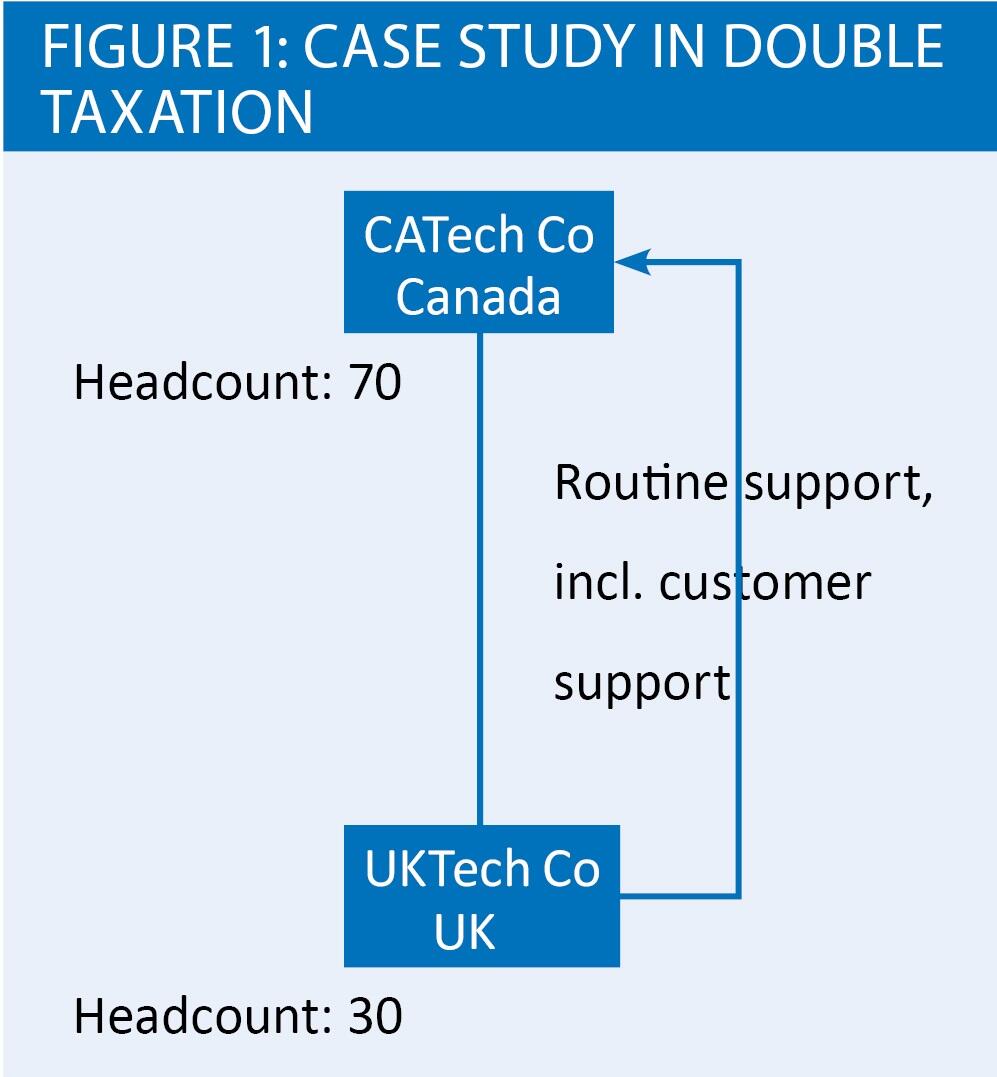

Case study in double taxation

Tech Co Group (‘the Group’) is headquartered in Canada and has developed a platform providing technological services.

- Intellectual property is developed and owned by CATech Inc (Canada) (‘CATech’).

- CATech makes sales to customers worldwide.

- UKTech Co (‘UKTech’) is remunerated on a cost plus 8% basis for its support functions in the UK, including customer support. See Figure 1.

Image

- HMRC issued a transfer pricing enquiry notice during the year following the submission of the UKTech’s tax returns. UKTech submits its contemporaneous transfer pricing documentation in the form of an BEPS-compliant master file and local file.

- HMRC follows up with both informal and formal information requests over a period of two years, leading to UKTech submitting large quantities of information. This includes invoices, financial modelling, accounting records, branding strategy, management profiles, organisational charts and email correspondence.

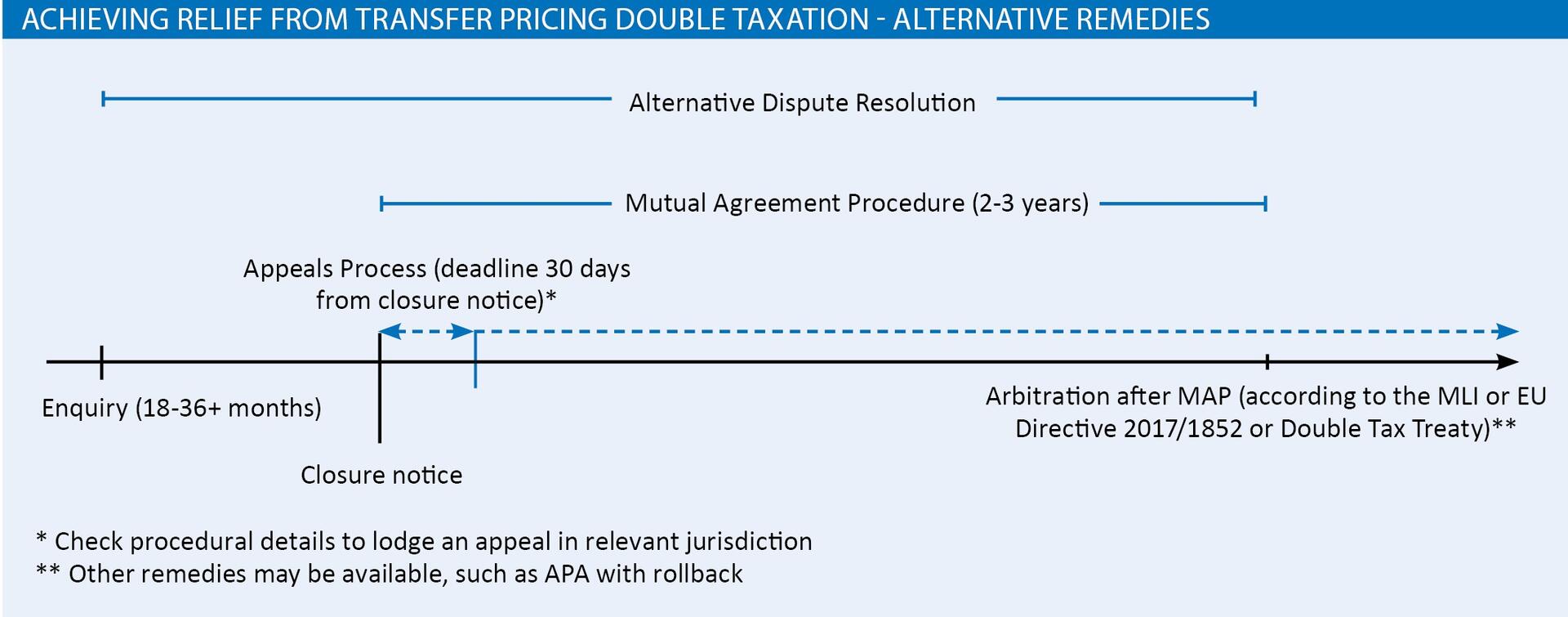

- Although HMRC’s guidance states that transfer pricing disputes will typically be resolved within 18 months for the majority of cases, and 36 months for those which are particularly complex and high risk, little progress has been made so far.

- The Group flies in two key senior Group personnel from the Toronto head office for a meeting with UK local management and HMRC to review the Group’s business model and supply/value chain showing that, although a large volume of support calls from new customers are routed through the UK call centre, the functions and costs associated with providing these functions are low value-adding in comparison to the functions performed and costs incurred in Canada.

- HMRC contends that the Group’s transfer pricing policy does not reflect the economic reality of the functions/risks performed/assumed by the UK entity and rejects the Group’s remuneration of the UK on a cost plus basis. HMRC’s reasoning is that the functions the UK entity performs are client-facing and at the revenue-end of the supply chain, and that, without the functions performed by the UK, customers would quickly get frustrated and leave the platform.

- HMRC uses the profit split method based on headcount as a splitting factor, and issues a closure notice on the basis that as the UK entity employs 30 people and the Canadian entity employs 70 people, 30% of the worldwide revenues should be allocated to the UK entity, and taxed accordingly.

- The Group transfer pricing policy is that the revenue was generated by and is attributable to the Canadian entity, and has, as such, been duly taxed in Canada. For that reason, a significant portion of the Group’s revenue has been taxed in both Canada and the UK.

- This results in double taxation, being the inclusion of the same income in the tax base by more than one tax administration.

What are the options?

Whilst the income between the two Group entities may or may not have been incorrectly allocated, the Group should be entitled to obtain relief for double taxation in accordance with the double tax provisions of the tax convention entered between the two jurisdictions involved (1978 Canada – UK Double Taxation Convention, amended by the 2014 Protocol – in force).

The UK’s double tax treaties (‘DTT’) are largely based on the OECD Model Tax Convention which aims to eliminate double taxation by determining which of the two contracting states has the right to tax a specific income. The UK benefits from one of the world’s largest DTT networks and has double tax treaties with more than 130 countries. Note that the vast majority of the UK’s DTT include a mutual agreement procedure (‘MAP’) provision. The UK has ratified the BEPS Multilateral Convention which significantly enhances the MAP, to the benefit of taxpayers. The UK has accepted binding arbitration. When these new provisions take effect will depend on when the UK’s treaty partners ratify the Convention, or when the two countries reach a bilateral agreement.

Option 1: Do nothing

Seeking effective double tax relief can be a long and arduous process. For that reason, the taxpayer may decide that it is more commercially viable to simply accept the assessment and regard the double taxation as an added cost of doing cross-border business. This might be the case if the business needs immediate resolution (e.g. it is preparing for an IPO) or if the amounts at stake are small and the issues have limited impact on other countries than the two directly affected.

In this scenario, the group would pay the tax as assessed by each jurisdiction, accepting the assessments raised, and bearing the costs of any potential interest and/or penalties imposed by the tax authorities.

This option would bring the matter to an immediate close, with no further action necessary. This would, however, expose the Group to double taxation. In the UK, an assessment that is not appealed can be treated as a ‘settlement’.

Should the company accept HMRC’s assessment, then it will not have any further domestic recourse. If, however, the taxpayer decides to fight the assessment, then there are a number of options open to it.

Option 2: Appeal to First-tier Tribunal (Tax) (‘FTT’)

An appeal may be brought against the closure notice within thirty days after the issue of HMRC’s notice. This appeal would be dealt with before the FTT.

The number of transfer pricing cases that have been litigated differs drastically depending on the jurisdiction. For example, in the UK there has been one transfer pricing case (DSG Retail Ltd & Others v HMRC [2009] UKFTT 31 (TC)) – HMRC’s appetite to litigate transfer pricing disputes has historically been low. On the other hand, Canada does not shy away from litigating transfer pricing cases. Other jurisdictions like India and the USA, also have many transfer pricing cases being litigated.

Appealing to the FTT may be time-consuming (i.e. a hearing is likely to last a week or more and the taxpayer may be waiting for over a year to get a hearing date). Hearings are public, something that many groups would wish to avoid. A settlement could still be achievable right up to the tribunal steps.

Once an appeal has been notified, it is still possible to engage in alternative dispute resolution mechanisms. That said, prospects of litigation should always be considered and using a litigation approach can lead to favourable settlements being agreed, with reductions in penalties also possible.

Option 3: Alternative dispute resolution

In the UK, alternative dispute resolution (‘ADR’) can be engaged at any time during a compliance check, e.g. when a taxpayer is unable to reach an agreement with HMRC, or where progress in the enquiry has stalled.

ADR can be used when, for example, communications have broken down with HMRC; there are disputes about the facts; a dispute appears to be the a result of a misunderstanding; it is unclear why HMRC has not agreed with evidence given, and why they want to use other evidence; it is not clear what information HMRC has used, and/or they may have made wrong assumptions and/or it is believed that additional information is being repeatedly sought without a clear explanation.

HMRC will let taxpayers know within 30 days of receiving an application if they agree ADR is right for resolving the dispute. If the dispute is accepted the taxpayer will be asked to fill in an agreement known as a ‘Memorandum of Understanding’. This sets out the ADR process. If the terms of the memorandum are broken at any time, HMRC can remove the dispute from the ADR process.

HMRC can reject applications for ADR and, if there are multiple factual issues or points of law, then ADR may not be the right mechanism.

ADR can be effective in resolving disagreements of facts and therefore should be ideally considered early on in transfer pricing discussions. Furthermore, ADR does not affect appeal rights, including a statutory review. It is not used often for transfer pricing but in the authors’ view, this may be a missed opportunity.

Option 4: Mutual Agreement Procedure

This option is invoked when a person considers that the actions of one of both countries’ tax administrations result or will result in taxation not in accordance with the relevant tax treaty. The taxpayer can request competent authority assistance under the mutual agreement procedure (‘MAP’) (i.e. under Article 23 of the double tax treaty between the UK and Canada in this case).

The objective of MAP is that the ‘Competent authorities’ (in our example Canada and the UK) interact with each other with a mandate to eliminate double taxation.

Competent authorities can act either unilaterally (e.g. changing only the decision of the UK tax authority to grant the taxpayer relief from double taxation without the involvement of the other contracting state) or bilaterally (where the two competent authorities negotiate with each other to try to reach an agreement over which of them has the best right to tax the income).

One advantage of MAP includes that the taxpayer’s ability to request MAP assistance is not restricted by any statutory dispute resolution process or prior domestic administrative procedures. In theory, MAP may be requested while under enquiry. Be mindful that, in this case, the taxpayer must submit a MAP request ‘within 3 years of the first notification of the action which results or is likely to result in double taxation’ (HMRC Statement of Practice 1 (2018) on Mutual Agreement Procedure (MAP), published 20 February 2018). There are cases where the deadlines to submit a MAP request were missed.

Competent tax authorities consult each other as necessary to determine corresponding adjustments, and the process can be concluded quickly and settle a number of past and future years depending on the jurisdictions involved.

MAP cannot be undertaken in conjunction with domestic judicial processes. Thus, the notice of appeal before the First Tier Tribunal would need to be stayed before entering into MAP.

However, it should be noted that not all jurisdictions are experienced at MAP and problems can arise where local law allows jurisdictions to withdraw decisions made, thereby lengthening the process significantly. This is not the case for the UK and Canada. However, although taxpayers will be involved in the process to a certain degree, they cannot force competent tax authorities to reach an agreement and, above all, taxpayers will not be involved in the actual discussions between competent tax authorities and cannot direct the conclusion towards the result they prefer. The entire process can also take years to reach completion. But the wider adoption of mandatory arbitration will in many cases render MAP more effective.

Option 5: Arbitration

Arbitration was introduced in the Model Tax Convention in 2008. When incorporated into the relevant DTT it is an integral part of MAP. As a result, it should promote a swifter MAP and increase the willingness of the taxpayer to request MAP.

BEPS Action 14 includes a commitment to mandatory binding MAP arbitration for those countries that agree to adopt it (Article 24 Paragraph 6). The purpose of arbitration is to provide an effective conclusion within a reasonable time. Governments therefore have an incentive to ensure that the MAP is conducted efficiently to avoid the necessity of subsequent supplemental procedures.

Furthermore, the adoption in DTTs, through the Multilateral Instrument (‘MLI’), of a mandatory binding arbitration provision to resolve issues that the competent authorities have been unable to resolve within a two (to three)-year period, should considerably reduce the risk of lengthy MAP as the parties will be wary of the ruling of an independent impartial third party. In our view, although arbitration may not actually occur, the threat of the facility should speed up any MAP (should both entities involved in any cross-border negotiations both reside in an EU-territory, the European Union Convention on the elimination of double taxation in connection with the adjustment of profits of associated enterprises, 90/463/EEC (EUAC) could be invoked). The UK has indicated acceptance of mandatory binding arbitration but note that both jurisdictions have to agree before the DTTs will effectively be amended. The OECD has a helpful ‘matching’ tool on its website. In the case of the UK/Canada the DTT already provides for arbitration, which is helpful.

Conclusions

- Don’t accept that double taxation is simply part of the cost of doing cross-border business.

- Don’t be tempted to prematurely enter into a settlement with a tax jurisdiction before considering whether alternative solutions, such as MAP, may be available to you.

- HMRC says it will resolve transfer pricing disputes within 18 months for most cases, however experience is that disputes often last 36 months or more.

- Companies need to be able to explain their business model, supply chain, value chain and functional analysis (i.e. functions, risks and assets) – as well as any changes to the business model and supply/value chain. If there is a clear picture of where value is added in the business, it will be easier to demonstrate why profits should be attributed to a particular jurisdiction. It may be, for example, that the UK is a key part of the supply chain, but not the value driver of the group, as it does not perform key functions for the group.

- Knowing which options are available can increase the prospects of a successful settlement that eliminates any double taxation.

Don’t forget to also consider interest, penalties and time limits for domestic and double tax treaties!