Directors' meetings

Share this article

David Hughes considers the importance of directors meetings in relation to the determination of where a company is resident

Key Points

What is the issue?

Following Laerstate the tax residence status of foreign incorporated companies is an area of increased interest to HMRC

What does it mean to me?

It is important to recognize the key characteristics influencing the determination of corporate residence

What can I take away?

The location of directors’ meetings, although an important factor in determining corporate residence, must be considered in the context of all the facts and circumstances.

De Beers: the case law test

De Beers Consolidated Mines Ltd v Howe (Surveyor of Taxes) 5 TC 198 is often quoted as authority for the rule that a company is resident where its board of directors meet, provided that the real business of the company is carried on at those meetings. This rule enunciated over a century ago still prevails in the determination of the corporate residence status of foreign incorporated companies and in most instances, the preliminary determination of such a company’s residence may simply involve an investigation into those meetings.

In the De Beers case, directors were resident in both London and Kimberley and separate board meetings were held in both places. However, the London board determined the company’s business policy, for example, major contracts, sales, asset development, profit investment and the appointment of directors. In contrast, the board at Kimberley mainly concerned itself with the day-to-day running of the South African mining business.

A similar fact pattern arose in New Zealand Shipping Company 8 TC 208. In this case, the New Zealand board considered local issues concerning the Australasia business and in particular, arranged for the necessary cargoes and freights for commodities. The London board however, had control of the company’s financial and administrative business, and made all the important policy decisions. For instance, the construction, acquisition and manning of ships was under the control of the London board.

Unsurprisingly, in both cases central management and control was held to emanate from the respective London boards. At the time these cases were decided, the question of whether a company could be dual resident had yet to be considered. It was not until the Swedish Central Railway 9 TC 342 case, heard in 1925, that the House of Lords affirmed that a company could be dual resident under the case law test.

Rubber stamping

Even where decisions are recorded as being made at board meetings, HMRC may challenge the residence status of a company by alleging that the overseas board of directors merely rubber stamped decisions made elsewhere. For example, in Untelrab [1996] STC (SCD) 1 HMRC argued at para 55: ‘The boards of the subsidiaries rubber-stamped decisions which had been made by Unigate and did not address their minds to what they were being asked to do. They did not really make the decisions and could not be said to be exercising central management and control. In answer to the question – who is taking the decisions – it had to be said that documentation was brought into existence in Bermuda and the decisions were taken in London.’

HMRC has had mixed success with this strategy. In the cases of Untelrab and Wood v Holden, [2006] STC 433, CA which both involved the determination of the residence status of subsidiary companies, it was held that, where the overseas board was not usurped, ie the directors functioned as a board and met, then ‘so long as the board exercised its discretion when coming to its decisions, and would have refused to carry out an improper or unwise transaction’, that board exercised central management and control. This is regardless of the fact that the directors may not engage in detailed analysis, but merely accept the advice they receive.

Laerstate: the importance of substantive director’s meetings

The importance of holding substantive board meetings was underscored in the Laerstate case. Indeed, Laerstate exhibits a catalogue of fundamental flaws which undermined the assertion that the real business of that company was being conducted at those meetings.

- For a substantial period, no board meetings were held, even though significant management activities were being undertaken in the UK by the UK-based director;

- Where board meetings were held, many of these were simply attended by one director, i.e., they were meetings in name only;

- The non-UK director attending those meetings was not immersed in the business of the company;

- Of the meetings attended by both directors, the tribunal found that certain of these merely recorded a decision made earlier in the UK.

In the absence of the board exercising control over the company’s business the tribunal found that the taxpayer made the decisions, personally, in the UK. At para 40, in relation to the period in which the taxpayer was a director, it stated: ‘We have found that Mr Bock’s activities as a director of the Appellant in the UK went much further than ministerial matters or matters of good housekeeping. His activities in the UK as a director of the Appellant were certainly concerned with policy, strategic and management matters, and, we have found, included decision-making in relation to the Appellant’s business in this period.’

UK-based directors

The question of whether directors are UK based or foreign based remains a very significant factor affecting the determination of a company’s residence status. Many of the early cases, e.g. The American Thread Company [1913] AC, 29 TLR 266, De Beers, and New Zealand Shipping, involved scenarios, where there were both local and London boards.

From the 6 April 2013, the old mainly case law based rules, determining an individual’s residence, are replaced by a new statutory residence test.

Under both the old and new regimes the inadequacy of residence as a measure of nexus, is exacerbated by developments in modern transportation, since it is now possible for a person to regularly spend time, and be resident in, various countries, to the extent that nexus with any particular country is of diminished import.

Unfortunately, the precise extent of nexus required to be meaningful has not been specified, nor has any formal calibration been prescribed. Indeed, sufficient nexus may be satisfied without an individual actually fulfilling the residence criterion, conversely it may not necessarily be met even where the residence condition is satisfied.

The phrase ‘UK-based director’ is used in HMRC’s manuals at INTM120150, which sets out certain HMRC guidance on corporate residence. However, in that guidance, the phrase ‘UK resident’ is used interchangeably, so that it is not suggested by HMRC that ‘UK based’ is a distinct category.

Notwithstanding the above it should be remembered that there is no requirement that an individual director be UK based for a company to be held to be UK resident by reference to that director, see for example, the case of John Hood 7 TC 327.

Committees

In the context of the role of directors meetings, it is important to underscore the fact that the directors have wide discretion of how the affairs of a company are to be governed. In particular, the board of directors may delegate certain of their powers to committees of directors. The precise roles, procedure, and powers of the committee should be set out in the company’s articles of association and bylaws etc. For example, a Finance Committee may be established comprised of several directors. That committee may meet and effectively determine the company’s dividend policy and key strategic investment decisions. If that Committee meets regularly in the UK, then it may be argued that central management and control over the company’s business is being exercised from there. This would remain a risk, even where the main board meets and rigorously discusses any proposals of that committee, since it is likely that the committee’s proposals would be routinely followed.

The dangers of holding committee meetings in the UK was highlighted in the Datacom case [2006] STC (SCD) 732. In this case, an executive committee was formed to undertake certain of the management functions of the company, most of the meetings of that committee took place in the UK. At para 65, the tribunal found: ‘that there was an executive committee, however constituted, and it was concerned with day-to-day operational matters. We have seen no evidence showing that the executive committee exercised all or part of the controlling brain of NDSP [Datacom]. The evidence that was presented to us was to the contrary.’

The above emphasises the risks inherent in holding committee meetings in the UK, since in determining that management and control was not being exercised at those meetings, the tribunal placed significant weight on the fact that it was against the interests of certain of the shareholders for it to have been so exercised. Clearly, if Datacom had been 100% owned by a sole shareholder, the tribunal may well have found that the committee had been exercising management and control in the UK.

Datacom also highlights the importance of specifying the role of any committee, since a particular weakness in Datacom was that ‘The precise timing of its creation and the extent of its authority and, indeed its membership, is not as clear as one could wish, from the evidence and documents.’

Notwithstanding the above, if it is considered necessary that a committee does meet in the UK, it is important to ensure that the matters which it considers and has responsibility for, are purely administrative, or ‘day-to-day operational matters’, and cannot be seen as matters pertaining to central management and control.

Modern communication technologies

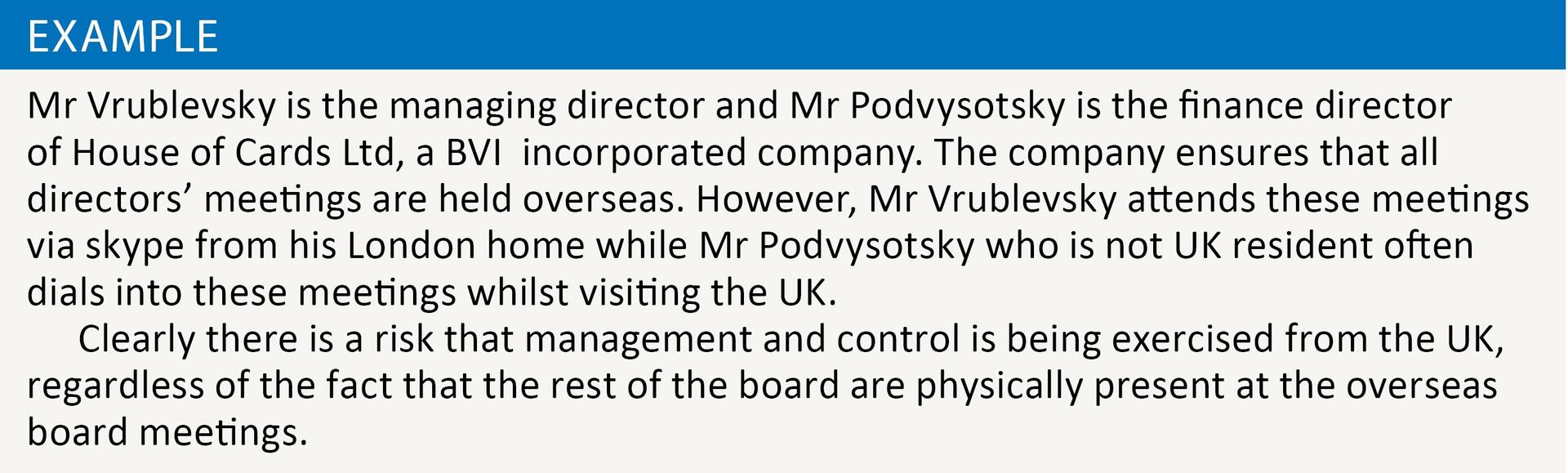

Clearly, where it is sought to preserve the non-residence status of an overseas company, it is advisable to ensure that no UK-based directors dial into meetings from the UK. Where appropriate, they should travel overseas and attend board meetings in person (see example). HMRC has provided useful guidance at INTM120150 regarding participation by UK-based directors, which applies to give comfort to certain overseas subsidiaries, provided that very strict conditions are met.

Board meetings exclusively overseas

Following from the above, the position may not be clear-cut where there is a mix of UK and overseas directors, even where the board meets exclusively overseas.

Mere oversight

In certain circumstances a person may be held to exercise ‘control’, although they do not appear to physically instruct or partake in the company’s decision making process. Lord Sumner, in the case of The Egyptian Hotels Ltd v Mitchell (Surveyor of Taxes) 6 TC 152 albeit in a different context, commented on what was sufficient to constitute control: He noted that Ogilvie v Kitton 5 TC 338 provided authority for the fact that ‘mere oversight regularly exercised’ would be sufficient ‘even though actual intervention never becomes necessary’. However, Lord Sumner provided further clarification by then going on to state ‘Some actual participation in carrying on the trade is necessary, though it may not go beyond passive oversight and tacit control. It is not enough that the proprietor merely has the legal right to intervene, otherwise Colquhoun v Brooks, 2 TC 490 would have been otherwise decided.’

Scenarios where residence will not be reviewed

HMRC has stated in its manual at INTM120140 that, where certain criteria are met, it would not normally open a review of a company’s residence status, even if it was apparent that central management and control was, in part, to be found in the UK. INTM120150 then sets out the criteria which includes that the overseas company is a subsidiary of a UK parent company, or a UK headed subgroup where the ultimate parent is non-UK resident. Various scenarios are considered, including where boards meet overseas, but contain UK-based directors.

Peripatetic boards

This section considers the implications of holding full board meetings, in both the UK and abroad, at which strategic business decisions etc are taken. Where full board meetings are held in various jurisdictions, then prima facie central management and control is being exercised in each of the relevant jurisdictions.

In INTM120150, Example 5 sets out a scenario where the board of the overseas subsidiary habitually holds in any one accounting period, a small minority of board meetings in the UK (no more than one or two). HMRC provides comfort that where specific conditions are satisfied, the residence status of the relevant company will not normally be enquired into.

In circumstance not falling within INTM120150, HMRC’s likely attitude to a scenario involving ambulatory board meetings is unclear. In its IM at ITH338, (now withdrawn) it merely notes that where ‘the company is peripatetic in the sense that relevant acts of control and management are exercised at different times at perhaps a variety of different locations, it is considered that the Courts have not yet fully addressed the question’.

Notwithstanding the above, in circumstances other than those within the ambit of Example 5 INTM120150, it is not clear whether the holding of an isolated board meeting in the UK would cause a company to become UK resident. Perhaps the closest the courts have come to considering this fact pattern is in Datacom. Here, the board met in various locations, including, on one occasion, the UK.

At para 63 the tribunal made a key finding of fact regarding that meeting: ‘We find as a primary fact that this meeting was concerned only with ministerial matters and matters of good housekeeping. The meeting was not concerned with policy, strategic, or management matters relating to the conduct of the business of NDSP. It did not reflect a manifestation of the controlling brain or where the business of the company was really carried on. It was not an exercise of central management and control.’

The fact that the tribunal went to such lengths to disconnect any question of the exercise of central management and control from one isolated meeting held by non-UK based alternate directors, who visited the UK for temporary purposes only, is ominous; although it is possible that the approach taken by the tribunal was influenced at least in part by the fact that the company did have a pre-existing nexus with the UK.

It should also be remembered that even if central management and control were found to be exercised from the UK, in treaty tiebreaker scenarios, the residence issue would, under many treaties, ultimately be determined by the ‘effective management’ criterion.