Disguised distributions: Private equity considerations

Share this article

We consider the real life experience of anti-avoidance legislation to prevent privately owned companies from providing loans as a form of disguised distribution in the context of a typical private equity backed group.

Key Points

What is the issue?

The ‘close’ company and ‘loan to participator’ legislation exists as anti-avoidance to prevent privately owned companies or groups from providing loans to shareholders or directors as a form of disguised distribution.

What does it mean for me?

This adds an additional degree of complexity in respect of company and shareholder transactions.

What can I take away?

Where a company or group is deemed to be ‘close’ for UK corporation tax purposes, consideration should be given to potential tax charges under the ‘loans to participator’ provisions (commonly known as a ‘section 455 charge’).

The ‘close’ company and ‘loan to participator’ legislation exists as anti-avoidance to prevent privately owned companies or groups from providing loans to shareholders or directors as a form of disguised distribution. The legislation essentially seeks to treat the loan as if it were a distribution for tax /purposes and charges tax on the company at a rate equivalent to the higher dividend tax rate.

Whilst this is generally the intention of the provisions, the drafting of the legislation is extremely broad, such that seemingly unintended scenarios (such as intra-group loans within close groups) can still be caught.

This article deals with real life experience of these provisions in the context of a typical private equity backed group.

This issue may not be considered until it is picked up as part of pre-transaction structuring or due diligence. It adds an additional degree of complexity in respect of addressing the tax risks that may be identified by interested parties as part of an already time pressured process.

Technical recap: ‘close’ company

Broadly, a company or group is deemed to be ‘close’ where it is controlled by either five or fewer ‘participators’ or any number of participators who are directors (Corporation Tax Act (CTA) 2010 s 439). This is an over-simplification, as concluding on whether or not a company or group is ‘close’ can take a significant amount of analysis. However, for the purposes of this article this overview should be sufficient.

A ‘participator’ is defined as a ‘person having a share or interest in the capital or income of the company’ (CTA 2010 s 454).

When determining the level of ownership by a particular ‘participator’, it is also necessary to include shares owned by their ‘associates’ (CTA 2010 s 451). Associates include, amongst other things, a participator’s relatives and any partners of the participator in any partnership (CTA 2010 s 448).

An ‘associated company’ is a company that either at that time, or at any other time within the preceding 12 months, has controlled or been under the control of the other; or alternatively have both been under the control of the same person(s) (CTA 2010 s 449). This effectively means that a company which is controlled by a close company is itself treated as a close company.

It is common for a private equity fund to acquire more than 50% of a business in order to secure control, and the fund investment vehicle. The aggregator vehicle behind which the limited partners and general partners sit tends to be some form of partnership. This means that all of the investors in the fund are treated as one participator due to all of the partners being associates.

On this basis, many UK companies that are private equity backed are often considered as ‘close’ companies for UK tax purposes, even where the company is controlled by a large private equity fund with potentially hundreds of investors.

Implications of being a ‘close’ company

Where a company or group is deemed to be ‘close’ for UK corporation tax purposes, consideration should be given to potential tax charges under the ‘loans to participator’ provisions (commonly known as a ‘section 455 charge’). There are other close company implications too, but they are not covered here.

Under CTA 2010 s 455, if a close company makes a loan to a ‘relevant person’ who is a participator or an associate of such a participator, the gross amount of the loan is liable to a temporary corporation tax charge at a rate equivalent to the upper dividend rate for the tax year in which the loan is made (Income Tax Act 2007 s 8(2)), provided that the loan remains outstanding nine months after the relevant lending company’s year end. This rate has recently increased to 33.75% (from 32.5%) for loans made from 6 April 2022, in line with the dividend upper rate for individuals.

There are some limited exceptions to the charge, set out in CTA 2010 s 456. This typically covers situations where either the loan is made in the ordinary course of business of the company; or where the loan is less than £15,000, the borrower is a full-time employee of the close company and the borrower does not have a material interest (broadly defined in CTA 2010 s 457 as being not more than 5%) in the close company or any of its associates.

Extension of the s 455 provisions

CTA 2010 s 459 extends the remit of the loan to participator rules by treating certain indirect loans made to a participator from a close company through another person, as being made directly to the relevant participator. The rules broadly apply where:

- a close company makes a loan or advance which does not otherwise give rise to any charge under s 455;

- a person other than the close company makes a payment or transfers property to or releases or satisfies (wholly or partly) a liability of a relevant person who is a participator in the close company or an associate of a participator; and

- the two events – the loan and the payment/release/satisfaction – are part of arrangements made by ‘a person’.

Section 459 does not apply if the total income (defined in Income Tax Act 2007 s 23 as the sum of the amounts of income on which the taxpayer is charged to income tax for the tax year) of the relevant person includes an amount that is no less than the loan itself. This effectively means that if the receipt of the payment is subject to tax in the hands of the individual, s 459 will not trigger a second charge. Section 459 will also not apply where arrangements are made by a person in the ordinary course of business carried on by that person. What is meant by arrangements and ordinary course of business is not covered in this article. Section 459(4) confirms that participators in the top holding company of a close company group should be treated as also being participators in the rest of the group.

Real life example

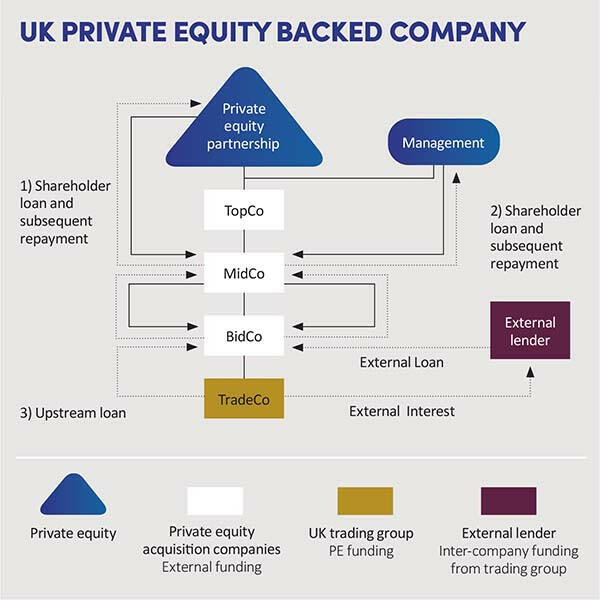

The diagram UK private equity backed company shows an example of how seemingly unintended consequences can occur in the context of a UK private equity backed company. The timeline of events is:

- BidCo has external bank debt.

- The private equity fund and management each provide shareholder loans to MidCo which are then on-lent to Bidco.

- TradeCo generates profits. External interest payments on the bank debt are settled by TradeCo on behalf of BidCo (as BidCo has no readily available cash).

- This creates an inter-company payable due from BidCo to TradeCo in respect of the interest payment.

- Some of the profits generated by TradeCo are also used to repay the shareholder loans.

In this case, on the wording of s 459, notwithstanding that there is no extraction of value from the group, a s 455 tax charge potentially arises as follows:

- A close company (TradeCo) has made a loan or advance that does not in itself give rise to a s 455 charge (in this case, the inter-company payable due from BidCo).

- A person other than the close company has made a payment (the loan repayments) to a relevant person who is a participator in the company (i.e. management and potentially some investors in the private equity fund).

- The payment has not been included as ‘total income’ in the hands of the participator.

Not the end of the story?

In a private equity context, the initial loan from the private equity fund, and therefore the subsequent repayment, can be significant, which in turn means the possible s 455 liability would also be sizeable. In such situations, the exceptions set out in CTA 2010 s 456 would typically not apply. There is, however, another possible way in which the exposure to the s 455 charge can be reduced if the private equity fund is prepared to work with the business and provide certain information in relation to the investors in the fund.

The s 455 charge should only apply where there has been some form of payment to a ‘relevant person’ which is defined in the legislation as either an individual or a company receiving a loan or advance in a fiduciary or representative capacity (s 455(6)).

Whilst the payment to management is likely to be caught in full as it is a payment to individuals, some of the private equity investors may be institutional or corporate investors, which would not meet the definition of a ‘relevant person’. In this case, the s 455 charge should be apportioned such that it only applies to the investors which meet the definition of ‘relevant person’.

Securing a s 455 repayment from HMRC

The s 455 charge is temporary in nature and CTA 2010 s 458 details how relief is obtained for s 455 tax paid to HMRC – either where the loan or advance is repaid to the lending company or the debt is released or written off. In our example, the advance we need to consider is the intercompany loan made between TradeCo and BidCo. In order to recover the s 455 charge, it is necessary to eliminate this intercompany balance, being the balance within s 459. The elimination of this balance should mean that s 459, and therefore by extension the associated s 455 charge, would no longer be in point.

Whilst there are a number of ways this balance could be eliminated (further commentary on this is outside the scope of this article), these may require distributable reserves to be available.

Where the balance cannot be eliminated, the s 455 charge effectively becomes a sunk cost to the business, rather than a temporary cash flow impact. In the context of the s 455 exposure being a potential adjusting item to the value the owners are expecting to receive as a result of the exit process, the further analysis required to fully understand the ownership structure and potentially mitigate a significant portion of that value adjustment can be critical.

Summary

- As TradeCo is considered to be a ‘close company’, in a straightforward scenario we would generally only expect CTA 2010 s 455 to apply where TradeCo directly or indirectly makes a loan to a ‘relevant person’ who is a ‘participator’ or an ‘associate’ of such a participator.

- However, as TradeCo has made an upstream loan to BidCo, and BidCo has made a payment that has been received by a participator, CTA 2010 s 459 extends the possible application of s 455.

- Any s 455 charge should, however, only apply to the proportion of the payment that is deemed to have been made to a ‘relevant person’ – typically an individual or a corporate entity which holds the interest on behalf of an individual.

- Any s 455 charge is technically temporary in nature, but securing a repayment in this situation can be tricky as sufficient distributable reserves may be needed in order to eliminate the upstream intercompany loan balance between TradeCo and BidCo.

- Where the balance cannot be eliminated, the s 455 charge effectively becomes a sunk cost to the business and its investors.