Down on the farm

Share this article

Sara Bonavia considers the income tax aspects of loss relief for farmers

Key Points

What is the issue?

As well as being governed by the normal loss relief rules for trading businesses, additional rules apply in respect of farming trades.

What does it mean to me?

Where activities within a farm have been diversified, careful consideration should be given to the results of activities that fall into the category of ‘farming’ as opposed to other activities, such as letting income and income from feed in tariffs.

What can I take away?

Advisers should be clear on the difference between a farming client’s accounting period and the tax year, as well as the specific rules for each type of loss claim.

As well as being governed by the normal loss relief rules for trading businesses, additional rules apply in respect of farming trades. Providing a farmer’s trade meets the normal commerciality tests, these additional rules can offer benefits, such as the ability to average their profits over two or five years (thus giving relief against significant annual fluctuations). The rules can also be restrictive, such as where the five year rule denies sideways loss relief if losses have arisen in the five consecutive previous tax years. This article considers the income tax aspects of loss relief for farmers.

What is farming?

The definition of ‘farming’ in ITA 2007 s 996 is ‘the occupation of land wholly or mainly for the purposes of husbandry but does not include market gardening’, albeit that the following rules also apply to market gardening trades as defined. In practice, there are areas that are clearly within the definition (for example, livestock rearing and the growing of crops), but as farmers increasingly seek to diversify, it is becoming more common for them to have multiple activities and sources of income (for example, from feed-in tariffs for solar panels sited on their land or renting a surplus field for caravan storage).

ITTOIA 2005 s 9(2) generally requires that all the farming activities of a trader in the UK are aggregated and treated as one trade. Therefore, it is not possible to have, say, separate cattle and sheep rearing trades, although in practice there may be scope for a farmer to have two, geographically distinct farms. However, this does not mean that all the activities carried out are farming – it may be that the farming activities make a loss, whilst the other activities are profitable. This distinction is important and can have an impact on the loss relief position.

Normal rules

Profits and losses are calculated for farmers in the same way as for other trades, with loss relief being available under the normal rules. Under these rules, losses from the continuing trade can be set against other income of the same or the previous tax year under ITA 2007 s 64, and/or capital gains of either the same or the previous tax year under ITA 2007 s 71 and TCGA 1992 s 261B, subject to the loss relief capping rules found in ITA 2007 s 24A.

Similarly, the extended carry-back rules for losses arising in early years of trading and on cessation also apply to farmers.

Claims for sideways loss relief are capped in the normal way under the rules for non-active traders (being those engaged for less than 10 hours a week) in ITA 2007 s 74A (applied to individuals by Finance Act 2008) and are subject to the normal rules on trading commercially with a view to realising a profit contained in ITA 2007 s 66.

Averaging

Recognising the potential for fluctuating farming profits, farmers are able to elect to average their profits over either two or five tax years (ITTOIA 2005 s 221 et seq). These claims can be made if the profits for one year are less than 75% of the other and can provide valuable tax relief for farmers who remain profitable but may be subject to tax at different rates year on year.

Five-year rule

Additional rules apply to losses generated from farming. The ‘five-year rule’ was introduced in 1967, specifically to prevent hobby farmers claiming to be farming and offsetting the losses against their other income, thus generating a tax saving. The theory was that genuine farmers wouldn’t make losses, and therefore wouldn’t be impacted. In the Parliamentary debate on an earlier 1960 restriction that required trading losses to be offset to have arisen on ‘a commercial basis and with a reasonable expectation of profit’, Anthony Crosland MP is quoted as saying, ‘it is impossible to believe that farming is growing less and less prosperous every year so that genuine farming losses are growing. On the contrary, common sense suggests the conclusion that farming is prosperous, that genuine farming losses are not on the increase and that what has been on the increase in recent years are hobby-farming losses’.

The five year rule is very specific – ITA 2007 s 67 denies sideways loss relief if losses have been made in each of the previous five tax years, not accounting periods, before any claims for capital allowances. This ensures that the rules cannot be manipulated by changes in accounting reference dates.

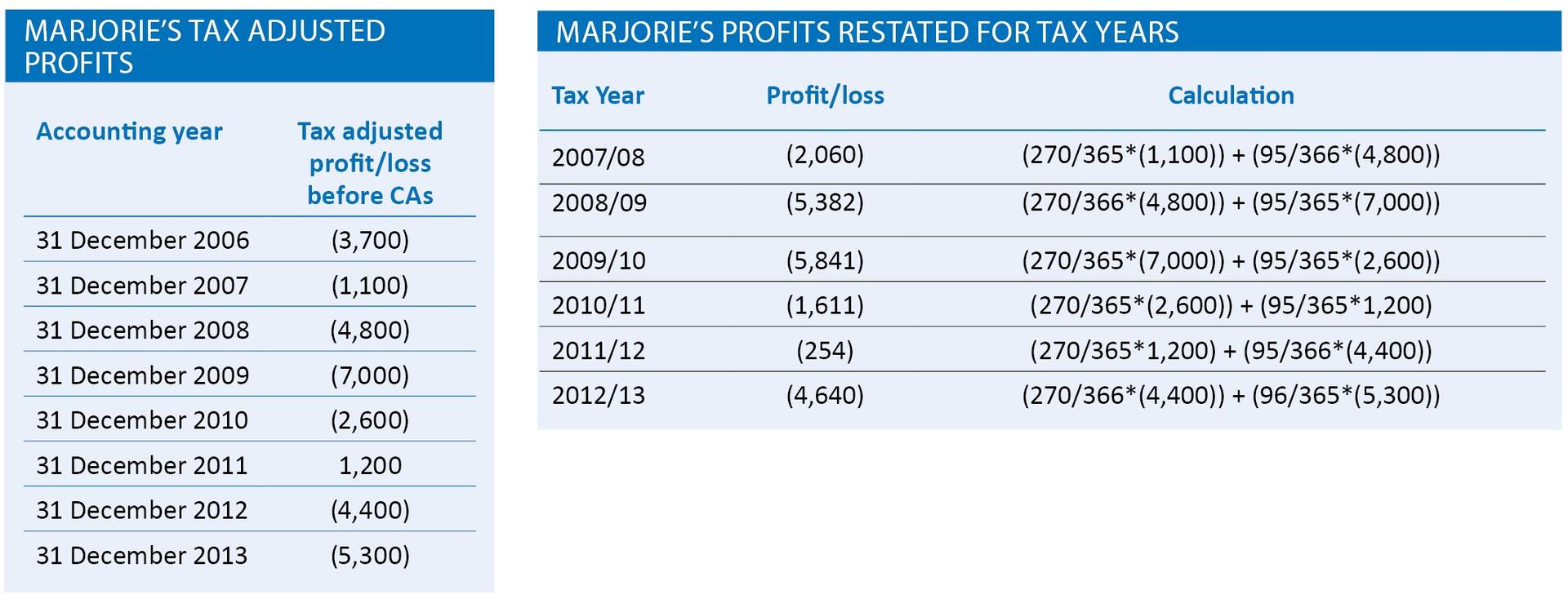

The application of this rule can give unexpected outcomes, as illustrated by the example of Marjorie Brown, found in HMRC’s manuals, BIM85630.

On an initial glance, Marjorie has made a profit in the year to 31 December 2011 after five consecutive years of losses. She then makes a loss in the year to 31 December 2012 which she wishes to set against her other taxable income for 2012 /13. However, when adjusted to calculate the losses on a tax year basis, she has made losses in all five preceding tax years, including 2010/11 and 2011 /12, such that the five year rule applies and no sideways loss relief claim is possible in 2012 /13 (or any subsequent tax year until a profit is realised in a tax year and the five year rule clock is reset).

An additional quirk in this rule is that the year of commencement is disregarded for the purpose of counting the five tax years.

31 March

The application of the five-year rule, and the need to apportion tax adjusted business results to tax years rather than accounting periods raises an interesting question. Although it is clear that the figures for accounting periods to 31 December need to be apportioned, can the same be said if the accounting period is instead to 31 March? Interestingly, the guidance published by HMRC only references 31 December and 5 April accounting periods.

In practice, 31 March and 5 April are generally treated as coterminous for purposes of identifying taxable profits, and this approach has been included within the opening year rules legislation in s 208 ITTOIA 2005, meaning that no overlap profits are generated in the case of a 31 March (or 1–4 April) year-end, unless the taxpayer elects to disapply the rule. Advisers should note that this and other sections concerning basis periods comprise new legislation on the introduction of ITTOIA in 2005. No corresponding rules existed in ICTA 1988 and hence, in particular, there will be many current businesses established before these rules were enacted with overlap profits to deal with on cessation or a change in accounting reference date.

Notwithstanding this, the author has seen an example of HMRC not accepting that 31 March can be treated as coterminous with 5 April when applying ITA 2007 s 67 and still expecting an adjustment to be made, even in the case of a taxpayer who has consistently used 31 March as the accounting date since commencement. As in the example of Marjorie Brown, this can lead to unexpected results in the case of a year of small profit in a run of years of larger loss. This concept of requiring adjustment for the five-day period seems to be a cause of confusion within HMRC, with the advice given in its Talking Points agent webinar on basis periods on 8 January 2016 being that there is no need to adjust between 31 March and 5 April, citing BIM81020 as a reference, even though ITTOIA 2005 ss 208–210 strictly only apply for the purposes of identifying opening years.

ITA 2007 s 68

ITA 2007 s 68 provides that loss relief can be claimed for a longer period, if the farmer can demonstrate that a hypothetical competent farmer would reasonably expect future profits, but would not reasonably have expected to become profitable until after the end of the particular tax year – the legislation in this area is prescriptive and strictly interpreted by HMRC, meaning that the bar to disapply s 67 by virtue of s 68 is high. The case of Christopher John French and Margaret Alexander French v HMRC [2014] UKFTT 940 (TC) considered this point – confirming that, ‘the objective of s68(3) is to preclude a farmer from enjoying the sideways and carry-back offset for farming losses, only if the actual farmer has been slower in anticipating profit than “the notional competent farmer”, so denying relief to the incompetent farmer.’

There is, however, specific guidance in relation to the restriction of losses after five years in connection with stud farms (BIM55725). Following an agreement reached in 1982 with the Thoroughbred Breeders Association, HMRC will accept that, as stud farming is a long term venture, sideways loss relief can be available for up to 11 years after commencement, providing that the business has the potential to be profit making in the future. This interpretation only applies to the period following commencement of a new business, not at any later point in the life of the business, including the period following the transfer of an existing business as a going concern to a new owner.

Timing expenditure

Although there is certain expenditure the timing of which cannot be controlled, there may be revenue (as opposed to capital) expenditure over which the farmer is able to influence the timing. In the event of a run of losses, exploring the future expected profitability and forecast significant expenditure with farming clients can be a very valuable exercise. Care must be taken here, as it is essential that the results declared are valid in accordance with generally accepted accounting practice and tax legislation. HMRC’s guidance in BIM42201 is well worth reading.

Settling cases

Although advisers would hope to resolve HMRC compliance checks into their farming clients’ affairs through the normal enquiry process, this is not always possible. This leaves the option to take a case to Tribunal, although many farming cases may be suited to the alternative dispute resolution (ADR) process. This gives the valuable opportunity for the client, adviser and HMRC to sit around a table to discuss the case and develop a rapport that can ensure that the relevant facts are explored and conclusions drawn. A passionate farmer can clearly demonstrate their aims and objectives, the history of their business and involvement. This can prove invaluable in convincing HMRC that they are trading with a view to realising a profit and are a genuinely competent farmer – although this does not mean that there is then carte blanche for claiming losses – is still governed by the rules as set out in statute.

Conclusion

Clearly the farming landscape has changed significantly from the 1960s when the five-year loss rule was introduced; however, the legislation, is still very relevant today. Advisers should be clear on the difference between a farming client’s accounting period and the tax year, as well as the specific rules for each type of loss claim. Where activities within a farm have been diversified, careful consideration should be given to the results of activities that fall into the category of ‘farming’ as opposed to other activities, such as letting income and income from feed in tariffs.