Electric Cars – reimbursement of employee expenses

Share this article

Peter Moroz looks at the tax complexities that arise when recharging an Electric Vehicle used for business travel

The Advisory Electric Rate increased on 1 December 2021 from 4ppm for 5ppm for the reimbursement of business mileage. But reimbursement for business mileage is the tip of the iceberg when it comes to tax questions.

Electric cars are becoming ever more popular. They are a key part of the Government’s Net Zero Carbon initiative. So, one would expect it easy to find clear guidance on all of the tax issues relating to the charging of electric cars.

However, this is not the case. The HMRC guidance on the income tax is complex and also regrettably does not always seem to match what the law says.

HMRC guidance

The HMRC manuals try to give comprehensive guidance. When I look hard enough, I find a large table coupled with 3 further flowcharts. I already get the feeling this is going to get complicated!

The guidance is set out like this because there are so many different combinations and fact patterns just on the question of the electricity provided (not including the provision of a home charging point):

- Company car or employee-owned car

- Electric car or hybrid

- Business use only, private used only, or a mixture

- Workplace charging or home charging or motorway charging

- Provision of electricity or reimbursement of electricity costs

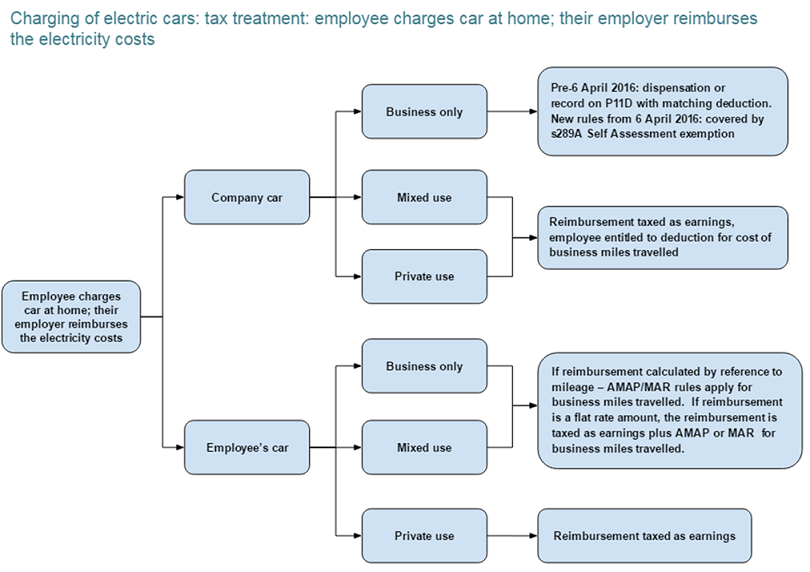

The chart below is one example of what HMRC provide and relates to the reimbursement of electricity expenses. There are separate charts for workplace charging and for the provision of electricity by an employer where charging takes place at home.

The chart seems comprehensive on the face of it but there are some oddities when you look at it closely.

For example, suppose an employer pays an employee (who has their own electric car) for their home charging electricity cost of £1,000 including VAT during the tax year. The employee happens to have driven 8,000 business miles. The chart says that:

- If the employer paid the electricity bill without calculating it by reference to mileage (or do they mean business mileage?), then the whole amount is taxable and subject to NIC (although the employee can claim Mileage Allowance Relief for tax but not NIC).

- If the employer says, I think I will pay for business mileage at 12.5ppm x 8,000 = £1,000, then the whole amount is tax free and NIC free.

There is no guidance given by HMRC for an employer who says:

- “I will pay the electricity, and I will make sure that the total amount reimbursed is below 45ppm per business mile.”

- “I will pay the electricity in full, and the employee will pay me back for all private mileage at, say, 5ppm.”

These are both realistic examples of a practical arrangement. Why after all would an employer pay for all electricity if it were not clear how much business/private mileage was being driven?

I do of course have some sympathy with HMRC for trying to make sense of a plethora of rules brought in at different times to cover so many different scenarios; with much of the law written without electric cars in mind. However, given that this is such an emerging area, I think they should urgently revisit the guidelines.

As well as the absence of guidance on some fairly typical scenarios, there is a further example of how the guidance above just does not seem to match the law when it comes to Company Electric cars:

Company Car Electric Car (used for business and private mileage) – Reimbursement of Electricity costs

The table says that the reimbursement is taxed as earnings with the employee entitled to a deduction for business miles travelled (although it is unclear whether we are to use 5ppm figure or the actual cost of electricity).

Either way, HMRC are saying that the reimbursement is earnings and subject in full to NIC (with no relief for business mileage).

This is not however what the law says.

The relevant legislation is at Section 239 ITEPA 2003:

S239(1): “No liability to income tax arises in respect of the discharge of any liability of an employee in connection with a taxable car or van…”

S239(2): “No liability to income tax arises in respect of a payment to an employee in respect of expenses incurred by the employee in connection with a taxable car or van…”

S239(3): “Subsections 1 and 2 do not apply to any liability arising by virtue of section 149 or 149A…”

[It is important to note that Section 239(3) is not in point as Section 149(4) obviates any liability under Section 149:

S149(4): “References in this section to fuel do not include any facility or means of supplying electrical energy…“]

S239(4): “No liability to income tax arises by virtue of Chapter 10 of Part 3 (taxable benefits: residual liability to charge) in respect of a benefit connected with a taxable car or van or an exempt heavy goods vehicle.”

With the current Smart meters around, the exact electricity cost associated with charging an electric car can be readily identified and distinguished from any other domestic electricity usage.

In view of the above, it appears that neither the reimbursement for a home charge point, nor the reimbursement of the cost of electricity for the electric car should be taxable. Furthermore there should be no NIC due nor any P11D reporting requirements. This is regardless of whether there is any reimbursement by the employee of private mileage.

VAT issues and the charging of Electric Cars

The question of VAT is also closely entwined with charging electric cars. HMRC issued a short Revenue and Customs Brief (7 – 2021) on the topic last year, but there are also some oddities contained in it and some other strange omissions. For instance, there is no guidance at all on the use of public charge points.

On the subject of VAT recovery for employees charging an electric vehicle (which is used for business) at home, there is the stark message from HMRC:

“You cannot recover the VAT. This is because the supply is made to the employee and not the business.”

However, this is at odds with HMRC internal manual VIT13400 which specifies when input VAT can be reclaimed by the business on supplies generally to employees. Specifically, it gives “examples of supplies which are to be regarded as made to the employer (provided the employer meets the full cost) even when it may look as if the employee has received the supply:

This includes road fuel and other motoring expenses…. “

The guidance goes on:

“You should decide whether the supply is legitimately paid for by the employer for the purposes of the business. If it clearly is then input tax should be recovered. This is in keeping with the intent of the legislation.”

The second oddity in Brief 7-2021 relates to the situation where:

“Employees charge an employer’s electric vehicle (for both business and private use) at the employer’s premises.

Your employee needs to keep a record of their business and private mileage so that you can work out the amounts of business use and private use for the vehicle.

You can recover the full amount of VAT for the supply of electricity used to charge the electric vehicle. This includes electricity for private use. However, you will be liable for an output tax charge on the amount of private use. This is because a “deemed supply” has been made…”

I have a few issues that concern me with this guidance:

- Why are employer vehicles singled out – does the guidance not apply to privately owned cars?

- What if most of the charging is done at home and only a little at work? HMRC state they deny any input VAT recovery for home charging, but now seem to seek additional output VAT because there has been some charging at work.

- What if the driver pays the employer for the private mileage? This is clearly a supply and output VAT will be due. But what if the charging took place mostly at home, so that input VAT recovery was denied? This will result in a double charging of VAT.

I appreciate that drivers will have to maintain mileage records for VAT and general commercial reasons (if not necessarily for income tax) and that seems wholly appropriate. In practical terms, (with the spiraling cost of electricity), I can also appreciate that more employers will want employees to pay for their own electricity costs insofar as it relates to private mileage, and employees will not always be content with a reimbursement for business mileage at only 5ppm if their own costs are higher.

As I observed at the outset, electric cars are a key part of the government’s Net Zero carbon initiative, and their use is escalating significantly. Given this, there is an urgent need for comprehensive guidance on the tax implications of typical scenarios arising from their use, guidance reflecting not only the letter of the law but also the spirit of the legislation.

Addendum – Stop press: Since I made these points to HMRC, I am pleased to report than in January 2022, HMRC have announced that they are indeed reviewing the VAT position where an employee is reimbursed by the employer for the actual cost of electricity used to charge a car. They are considering what evidence can be provided to allow the employer to reclaim the related VAT and also considering other simplification measures. They have also given guidance on VAT recovery and public charge points.