EMI – simply the best

Share this article

Enterprise Management Incentive schemes are simply the most tax efficient and flexible share option plans. But, says David Marcussen, just make sure you don’t fall foul of the rules – it’s easy to do.

The arrival of the Enterprise Management Incentive share option plan in the summer of 2000 opened up a new landscape for employee share option plans. Now, employees can place a one-way bet over their employer company shares and benefit from the same tax benefits as the founders who have invested real cash in the venture.

That’s right – the option holders are entitled to 10% capital gains tax on the profits they make on their shares, even though they’re not financially exposed to the company shares. If the shares go down, they lose nothing. If they go up, they win. That’s the kind of bet I like. And all this is approved by HMRC.

In short, EMI is by far the most tax efficient and flexible HMRC-approved share option plan. And, of course, that makes it a great way to incentivise senior employees to make the company a success – so they can exercise their share options.

The basic rules

Company qualifying criteria

Not all companies can participate. Much like the Enterprise Investment Scheme (see my previous articles) companies need to satisfy the qualifying criteria:

- The company must be independent – not under the control of another company or quoted. Note that an arrangement to sell the company (ie when heads of terms are signed to sell the shares) would be regarded as breaching this rule, without the actual sale taking place.

- Gross assets must be less than £30m.

- Qualifying trades – same excluded activities as EIS (ie no financial activities, nursing homes, etc).

- The company (or a company within the group) needs a UK permanent establishment. This differs from EIS – there the group holding company needs to have a UK PE.

- There must be fewer than 250 employees – note this means full-time equivalent when the options are granted. Seasonal business can grant options off season when the number of employees is lower.

- The EMI options can total a maximum of £3m – based on the market value at the date of grant.

Option holders qualifying criteria

As well as restrictions on the company, there are restrictions for the option holders:

- The market value of the options can be no higher than £250,000 (based on market value at the date of grant).

- The employees / directors must be full time – or at minimum work 25 hours a week or 75% of the working time (whichever is lower).

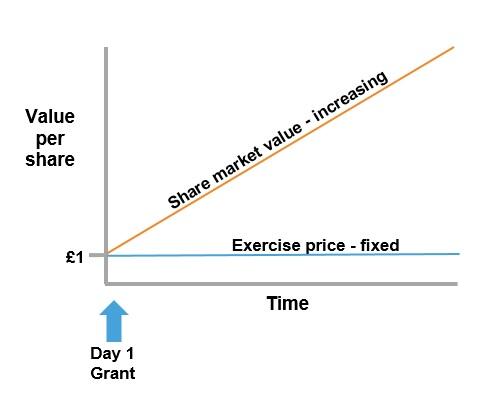

EMI options lifecycle – tax treatment

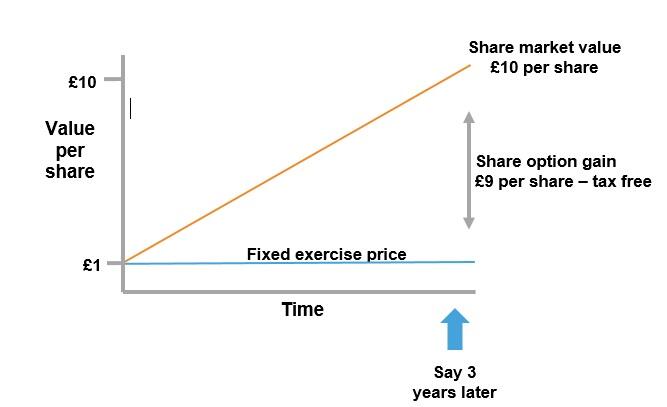

Grant – no tax to pay

Exercise – no tax to pay

There’s normally no income tax (or NI) when the EMI options are exercised. But if the options are granted with an exercise price less than the market value at the date of grant, then this discount is subject to income tax (and NI if the shares are readily convertible assets) at the date of exercise. This will be paid by PAYE if the shares are readily convertible assets, and if not the income tax (no NI) will be paid through the option holder’s self-assessment tax return.

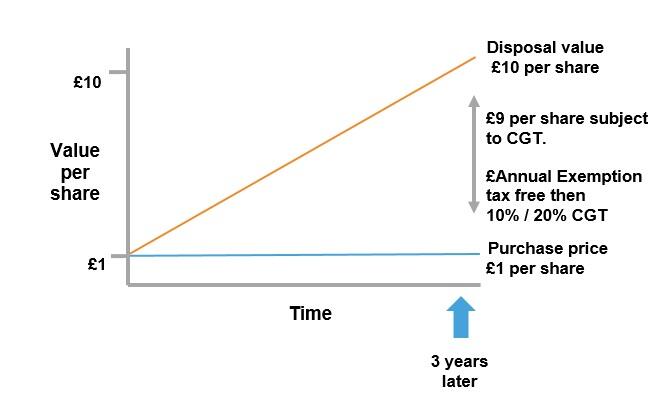

Disposal of Shares – CGT at 10%

Here’s where the big benefits come in. So long as there’s one year (or two years for disposals after 6 April 2019) from the date of grant to the disposal of the shares, and the option holder is still an employee/officer of the company, Capital Gains Tax of only 10% will be due. That’s a massive reduction.

Where to be smart

Entrepreneurs’ Relief for minority shareholders

When someone sells the shares that they’ve acquired via EMI options, they qualify for Entrepreneurs’ Relief, so long as at least 12 months (or 24 months from April 2019) have passed from the date of grant to the disposal of the shares. Not bad.

And unlike normal Entrepreneurs’ Relief rules, there’s no need for the option holder to own 5% of the share capital, or meet any of the further tests introduced in the recent Budget.

Growth shares – £250,000 / £3m limits

As companies grow in value, those limits on the value of EMI options can come under pressure – that’s £250,000 for an individual and £3m for the whole company. But this pressure can be relieved by granting EMI options over Growth Shares, which have a lower market value. Growth Shares are a whole separate subject, but in summary Growth Shares are a separate class of shares that participate above a fixed hurdle, which may be the current market value of the company. So the Growth Shares have no economic rights until the company increases in value in the future, so a low market value can be agreed for them at the date of grant. But take care to make sure all the EMI qualifying criteria are satisfied.

Parallel options

It can be useful to reprice existing options with a lower exercise price and / or lower performance conditions. Parallel options, which are granted alongside the existing options, leaving the existing options in place, are not counted as part of the £250,000 or £3m limits (ie no double counting). They simply offer the option holder a better deal.

It’s not all about tax

Modelling awards – don’t under / over award

Companies put in place EMI share options to attract, retain and motivate employees and directors. But this won’t work if the company under- or over-awards options, or runs out of shares to award to team members who join later in the company’s lifecycle.

So it’s critical to model the allocations of options to all employees over the entire journey of the company right up to the sale of the company. This involves considering not only those individuals who are with the company now, but those who will, or may, join in the future.

To help with the modelling, a rule of thumb can be:

- The total share option pool should not be more than 10%; and

- The ‘benefits’ for the employees are equal to an annual salary.

This is a useful starting point for the model, and both points can then be flexed as necessary.

Option holder communication

It’s all very well designing and setting up the ultimate employee share plan for a company. But this is no good if the employees don’t understand what they’re being given. If they don’t understand it, they won’t value it and it therefore it won’t be effective in attracting, retaining and motivating the employees and directors.

A proper communication event should take place to explain in detail where the company is going and how the employees will take part in this, and crucially why the share option plan means that employees will benefit along with the shareholders. It also needs to explain the tax benefits of the EMI plan – in concrete terms that make real financial sense.

Flexibility / board discretion in documentation

The company can lay end-less clever plans for the future and link the performance criteria of option holders’ share options to these plans. But things change. That’s why you should always include directors’ discretion, so the directors can vary the performance and vesting conditions of the options to give flexibility if needed (for example the options may only allow exercise on an exit event, but the shareholders may decide not to sell yet still want to share the equity ownership with the team). This can also be extended to flexibility around the leaver provisions.

What to remember

Register the EMI options online with HMRC within 92 days

The EMI options must be registered online with HMRC within 92 days of the date of grant. In my experience, this is the single most common reason for EMI options not to be qualifying. Clients just forget to register the options – despite repeated reminders.

HMRC clearance

If there’s one thing you take away from these articles it should be the importance of submitting a highly detailed – and complete – prior clearance to HMRC.

HMRC valuation

The market value of the shares over which EMI options are to be granted can be agreed in advance with HMRC. This valuation is then normally valid for up to 60 days.

HMRC are very easy-going about valuations of early stage companies, so lower valuations can normally be agreed.

However – and this is a strong warning and really matters – the valuation is only valid if all facts are disclosed to HMRC. Take particular care if there’s a sale lined up for the company as this will impact on the valuation – despite the basic principle that hindsight cannot be used to value assets. Don’t be tempted to hold back information from HMRC… ever. It will return to bite you.

Working time declaration

There’s a requirement to provide the option holder with a copy of the working time declaration within seven days of the date of grant for the options to be qualifying. A separate one page document covering this is useful to ensure this rule is satisfied – leave one copy with the option holder at the time of signing.

Entrepreneurs’ Relief and ceasing employment

Shares acquired from the issue of EMI options qualify for Entrepreneurs’ Relief, but the option holder still needs to be an employee of the company when they come to dispose of the shares. Take care, therefore, when option holders cease employment.

There can be benefits for the option holder to exercise the option before they cease full-time employment, and then perhaps maintain some form of part-time or officer status with the company to continue to qualify for Entrepreneurs’ Relief.

Interaction with CSOPs

When a company breaches the qualifying conditions for EMI purposes it’s common to introduce a Company Share Option Plan, under which tax efficient share options can be granted to employees over up to £30,000 of shares.

But remember, these CSOP options count as part of the option holder’s £250,000 EMI limit – so be extremely careful not to breach this limit. For example, if an employee holds £230,000 of EMI options they will be restricted to only £20,000 of CSOP options.

And if they don’t stay within the £250,000 limit? They don’t just lose the tax benefits on whatever is over £250,000. They lose the whole lot – they are disqualified from all the EMI options’ tax efficient status. Whoops. And that is best avoided.

Qualified lawyer

It is extremely easy to fall foul of rules, tax rules, company law and commercial rules in the option documentation. What’s more, these errors normally only become apparent at the time of a sale of the company – when, of course, it’s far too late to do anything about it.

10% tax suddenly becomes 54.59% tax. Not good. So wherever possible work with a lawyer who is familiar with EMI.

Corporation tax

When the EMI options are exercised, the company is entitled to corporation tax relief on the difference between the exercise price and the market value at the date of exercise. This could be a significant sum.

As an example, if a company is sold for £20m and it has EMI options in place over 10% of the share capital (with nominal exercise price), the benefit to the company could be as much as £380,000 (i.e. £20m x 10% x 19% corporation tax).

This tax asset belongs to the company and arises before the company is sold. And that means it’s an asset of the selling shareholders.

In the example above, the shareholders should receive £20,380,000 for the sale of the company, rather than just the £20m. Negotiate this into the heads of terms at the outset, otherwise it may be lost in negotiation.

Also, it’s possible to agree the market value of the company – where for example there’s deferred consideration – with HMRC for corporation tax purposes after the sale has completed. This is recommended to maximise the benefits.

EMI annual return

As well as registering the EMI options, the company is required to file an EMI annual return for each tax year. HMRC now impose automatic penalties for late filings, so don’t miss the 6 July deadline each year.

Register the EMI options online with HMRC within 92 days

No, this isn’t a printing mistake. It’s another reminder not to overlook this point. If necessary, set up an agent’s access to the online portal and register the EMI options on the client’s behalf. It’s that important, and that easy to forget.

What’s next?

So, my 3 articles have covered the SEIS / EIS rules, helping companies raise funding, Entrepreneurs’ Relief for the founders, and now the tax breaks for the employees with the EMI plan. What next?

Well, when all of the individuals benefit from all of these tax reliefs on the eventual disposal of their shares in the company, they will become high net worth individuals. Their personal tax profile changes and they need to adopt a strategy to optimise their personal tax position going forward. This can be achieved in a very, very tax efficient way. How exactly? I may well cover this in a future article…

Until then – don’t forget those HMRC clearances and to register the EMI options within 92 days of the date of grant!