End of the goodwill trick?

Share this article

Rebecca Benneyworth considers the case for incorporation in 2015

Key Points

What is the issue?

How does the removal of tax relief in a company when goodwill is purchased from a connected person and the exclusion of goodwill on incorporation from entrepreneurs’ relief affect the decision to incorporate a business

What does it mean to me?

These changes reduce the initial tax benefits on incorporation and, together with the amendments to dividend taxation proposed for 2016, will require advisers to think carefully about how to advice unincorporated businesses

What can I take away?

There is still a significant advantage to those with very profitable companies in setting a high value to goodwill despite the tax liability it creates

Finance Act 2015 includes two changes that affect the decision to incorporate a business and by which method. Although part of the legislation is repealed by the second Finance Bill and replaced by measures in clause 32.

The first change is the removal of tax relief in a company where goodwill or other customer-related intangible assets is purchased from a connected person (FA 2015 s 26). The change prevents those who have started in business since 1 April 2002 selling internally generated goodwill to their company and gaining a tax deduction for amortisation of this. Businesses that launched before 1 April 2002 have been unable to benefit from goodwill amortisation on incorporation because the sale of goodwill into the company does not create ‘new’ goodwill. This puts all businesses on a similar footing for the treatment of goodwill on incorporation. The change applies to goodwill purchased from a related party on or after 3 December 2015. Existing purchased goodwill continues to attract tax relief on any write-down in the accounts.

The proposals in clause 32 of the second Finance Bill 2015 abolish this measure from 8 July 2015, at which point relief is removed for all customer-related intangibles and purchased goodwill, whether third party or connected purchases.

The second change, made by FA 2015 s 42 (inserting s 169LA into TCGA 1992) is the exclusion of goodwill on incorporation from entrepreneurs’ relief. The exclusion applies to the sale of goodwill to a close company that is related to the disposer. Any disposal on or after 3 December 2014 will attract capital gains tax at the usual rates after the annual exemption, if applicable. If a partnership incorporates, any partner leaving the firm at that point will be able to use entrepreneurs’ relief to reduce their tax liability to 10%.

These changes reduce the initial tax benefits on incorporation and, together with the changes to dividend taxation proposed for 2016, will require careful thought about the most suitable structure for a business.

Chargeable assets on incorporation

The goodwill element in the transfer of the whole trade as a going concern can cause problems because this frequently has zero cost to the individual. Some other major business assets, such as property, may also give rise to a chargeable gain on transfer, which is done at market value, because the disposer and the company are connected persons. Most other business assets are not liable to CGT on the transfer.

If the business is to incorporate, there are three possible scenarios to consider:

- pay CGT at full rates, leaving a loan account to draw on;

- shelter the capital gain using relief for incorporation under TCGA 1992 s 162; and

- shelter the capital gain using holdover relief for gifts of business assets under TCGA 1992 s 165.

Each of these will be considered in turn using a goodwill value of £100,000. The potential presence of a business property must also be considered. This has an assumed gain of £100,000 and a market value of £250,000.

Pay CGT at normal rates on goodwill

The disposer would be liable to capital gains tax at 18% and 28%, depending on their income. However, their plan might be that they will create a loan account in the company on which they can draw in preference to drawing taxable income such as salary and dividend.

If the disposer is a higher rate taxpayer – likely in the final period of trade as a successful business ready to incorporate – the tax on the disposal of the goodwill will be £24,892 (25% effective rate), assuming that the annual exempt amount of £11,100 is fully available to them. This provides a loan account balance of £100,000 for them to draw against.

They will then draw income to the extent that the marginal rate is less than 25%. In 2016/17 that would indicate drawing a salary of around £8,000 (the National Insurance threshold), interest at 8% on their loan account, giving £8,000 that is tax-free (£3,000 within the personal allowance and £5,000 attracting the savings starting rate of zero) and dividends of £5,000 that are also tax-free. This provides them with £21,000 after tax. Further dividends can be drawn within the basic rate band as they suffer tax of only 7.5% in addition to the corporation tax which will be paid in any event. When dividends reach £27,000 (total income £43,000) the director would switch and draw from their loan account, rather than bear tax at 32.5% on any additional dividends.

If it is the intention to transfer a business property, this will attract entrepreneurs’ relief and therefore the gain will bear only 10% tax. Using the example figures given, this will provide the client with £350,000 on their loan account that has borne tax of £34,892 (£24,892 + £10,000) – that is a rate of only 10% overall.

Although we have become used to the value of goodwill being challenged, one might expect that, if tax is to be collected at 28% on the value, HMRC will welcome over-optimistic valuations. However, as illustrated here, there is still a significant advantage to those with very profitable companies in setting a high value to goodwill in spite of the tax liability it creates. It is likely, therefore, that HMRC will still look carefully at goodwill valuations.

Incorporation relief

The changes may herald a resurgence of this now rarely used relief. However, the conditions associated with it make the relief largely impractical and this may drive advisers to the other two options.

Conditions for the relief

- all assets of the business, other than cash, are transferred to the company;

- the business is transferred as a going concern; and

- the transfer is wholly or partly in exchange for shares.

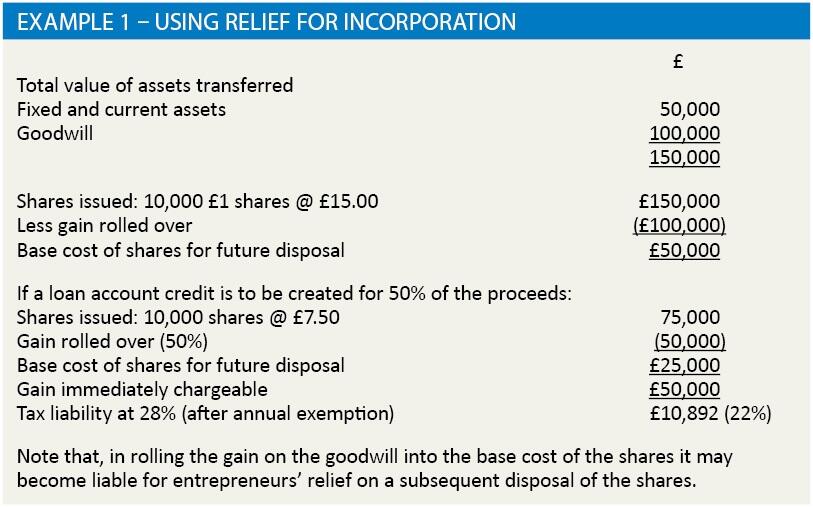

If the conditions are met relief is given by rolling the gains on the business assets into the base cost of the shares, reducing it and therefore inflating the gain on eventual sale. If any part of the consideration is given as cash (or loan account) this produces a gain at the time of transfer, the balance of it being rolled over. The chargeable amount is the proportion of the gain represented by cash as a proportion of the consideration. The assets are treated as acquired by the company at market value for the purposes of subsequent disposal.

Assuming that the value of non-chargeable assets, such as tangible fixed assets, stock and debtors, is £50,000 and there is no property to transfer, the computations are shown in Example 1.

The key disadvantage of this relief is that all of the assets of the business must be transferred for the relief to apply. This means that debtors must be transferred under deed, and if there is a business property, the owner has no option but to transfer it into the company. While this serves well if the company is to continue to own premises in the long term, clients may be reluctant for various reasons to put this property into the company. In that case, the relief is not available.

Holdover relief

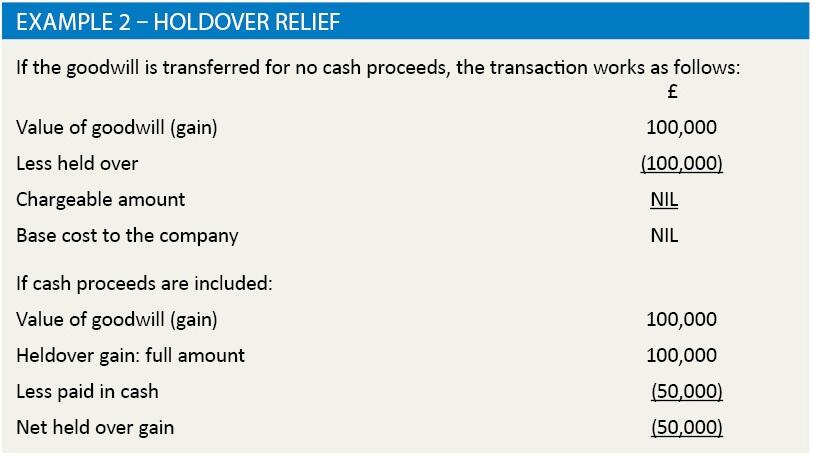

This relief applies to disposals of chargeable assets used in the trade where the disposal is not an arm’s length transaction. It is commonly used in the transfer of a business to a company because it allows the retention of the debtors and creditors by the trader who will then ‘clear down’ the balance sheet of the trade and allow the company to start up with a clean sheet. It will also allow the trader to retain any property used in the business, which may be necessary if borrowings are secured over it. The transfer may be made for no cash consideration at all – in which case the company acquires the asset at the disposer’s base cost, or for some cash consideration. In the latter case only the gain in excess of the cash consideration can be rolled over.

The effect of the relief, therefore, is to reduce the base cost of the asset in the company. Here, the liability for tax on the eventual disposal has passed with the asset to the new owner, whereas incorporation relief leaves the tax liability on the gains with the original disposer. The condition for relief is that the asset has been used in the trade throughout its period of ownership by the transferor. The impact of the relief is shown in Example 2.

As can be seen, by combining cash consideration and triggering a partial gain, the disposer and their adviser have adequate opportunity to plan for the best possible outcome, particularly after taking into account the benefits of having at least some credit on the loan account to enable interest to be paid to the director and income-based drawings to be managed. This is particularly relevant if the disposer has some basic rate band available in the year of disposal, reducing at least part of the tax charge to 18%, or indeed capital losses to be used.

Other issues

VAT transfer

The company will need to be registered for VAT if the trader was exceeding the mandatory registration limit. The trader can notify transfer of a going concern, which will mean that no VAT is chargeable on the assets and goodwill transferred.

There is no possibility of transferring the trade of a VAT registered business to the company without registering the company for VAT immediately. The going concern provisions are structured so that the supplies made by the business are treated as supplies of the company, which are therefore in excess of the VAT limit from the day trade is transferred.

The election to transfer the VAT number is a separate election, which is done on form VAT 68. The impact of this is to transfer the VAT liabilities to the company, which also becomes responsible for any VAT errors made by the individual in the preceding three years. However, the liability accepted by the company is only for output tax errors, and not for input tax over recovered – this remains the liability of the trader.

Capital allowances on incorporation

Where the company is to take over the assets of the trade, the simplest method for capital allowances purposes is to elect to transfer the assets at tax written down value. This will pass the pool values over to the company on termination of the trade. This election is made jointly and must be made within two years of the transfer. Note that if an election is not made the transfer takes place at value agreed between the parties, and first year allowances are not available on any of the assets transferred as they are acquired from a connected person. This can be used to create balancing allowances in the trade if desired. If any of the assets comprise fixtures in a building, the requirements of that legislation must be followed.

Note also, that no allowances will be available in the final period of trade, when only balancing adjustments are available. This could cause the loss of annual investment allowance which would otherwise have been expected.

One alternative is to draw an account before the date of incorporation, secure the allowances and then incorporate after a further short period of trading.