An extra layer of complexity

Share this article

Juliet Minford provides an overview of the new rules regarding the extra 3% SDLT which will apply to some residential property acquisitions

Key Points

What is the issue?

An additional 3% stamp duty land tax/land and building transaction tax will apply to some residential property acquisitions in the UK from 1 April 2016.

What does it mean for me?

This creates an extra layer of complexity when quantifying SDLT/LBTT for purchasers of residential property.

What can I take away?

The scope of the additional 3% charge is far-reaching and should be considered for all acquisitions of residential property.

Following an announcement in the November Autumn Statement and a subsequent consultation process, legislation has been introduced that adds an additional 3% to the SDLT/LBTT liability for certain transactions. The amendments cast a wide net, include both second homes and buy to let properties and are rife with complexities and surprises.

The additional charge applies where transactions are completed on or after 1 April 2016 unless contracts were exchanged before 26 November 2016 for SDLT (27 January 2016 for LBTT).

Scope of rules

The stated purpose of the new rules is to reduce competition for first time buyers by making it more expensive for those who already own a property to purchase a second property. Yet the legislation is understandably and necessarily fraught with complexity.

Only natural persons can escape the additional 3% charge. The charge applies to individuals where, following an acquisition of a UK residential property, the buyer owns more than one house, anywhere in the world. Where the purchaser is married or in a civil partnership, the charge will apply where the spouse or civil partner already owns a home.

An exemption is available where the UK property acquired is replacing an existing main residence which has been sold in the last three years (18 months for LBTT). Where the existing residence hasn’t yet been sold, the additional 3% will need to be paid upfront and then reclaimed if the existing residence is sold within three years (18 months for LBTT).

The requirement to be replacing an existing main residence potentially results in some anomalies. For example, a buy-to-let investor moving out of rented accommodation into their first ‘owned’ home will pay the extra 3%, whereas a buy-to-let investor who already owns their own home and is replacing it will not.

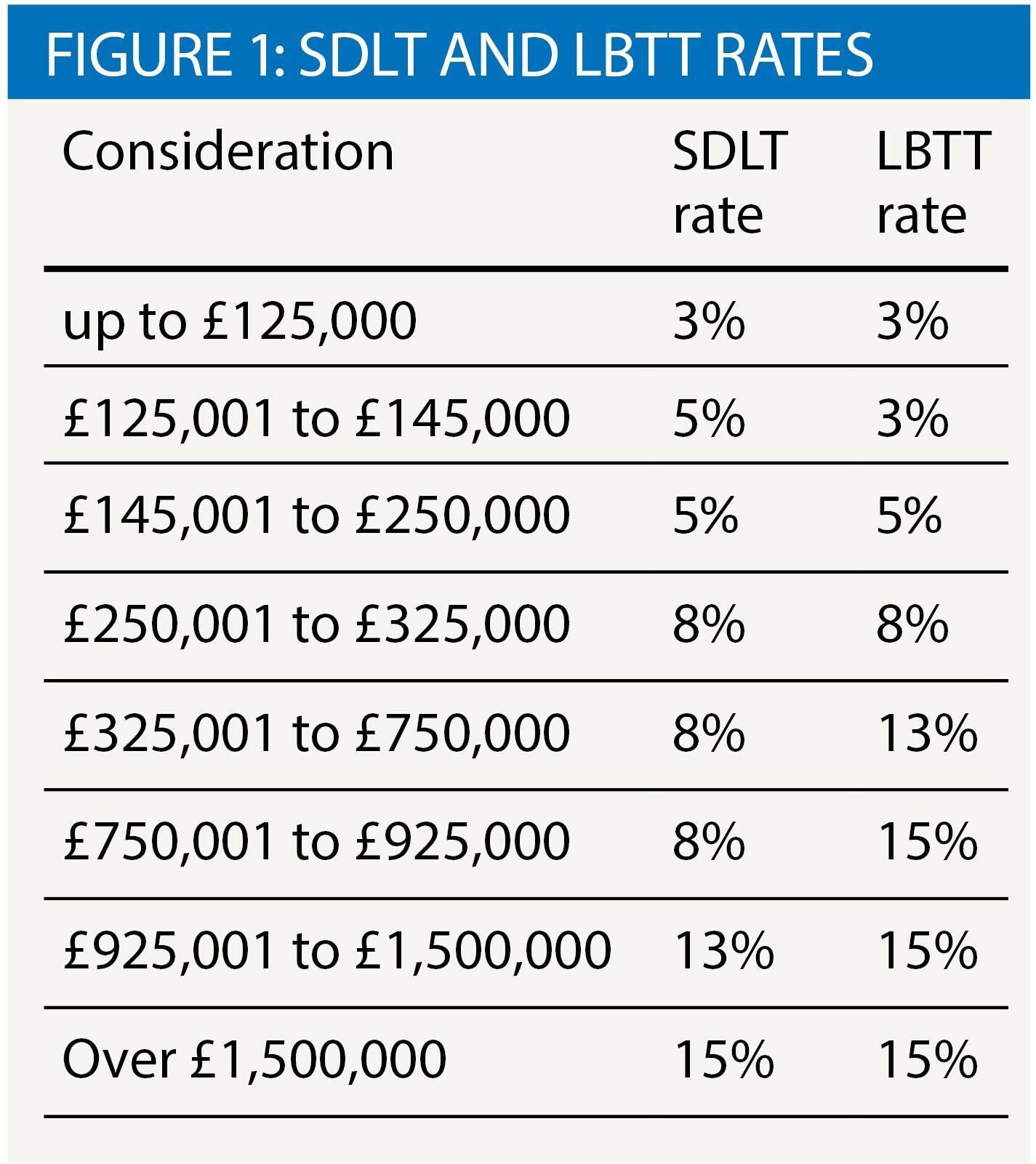

Where the additional 3% applies, the SDLT and LBTT rates for consideration which falls within the relevant bands are shown in Figure 1.

Annexes and basement flats

As things currently stand, where an annexe (for example, a granny flat) is purchased with a main residence and the price apportioned to the annexe is £40,000 or more, the transaction is potentially within the scope of the additional 3% on the entire transaction. We anticipate that changes to the legislation will address this unexpected result.

The proposed 3% charge applies to what are called ‘higher rates transactions’ which includes a transaction where:

- the purchaser is an individual;

- the main subject-matter of the transaction consists of a major interest in two or more dwellings; and

- in respect of at least two of the purchased dwellings (A) the chargeable consideration attributed to purchased dwelling is £40,000 or more and (B) the purchased dwelling is not subject to a lease upon which the main subject-matter of the transaction is reversionary.

This means that the annexe taints the entire transaction, rather than the annexe itself simply being subject to the additional 3%. HMRC’s published guidance confirms that:

‘Where an individual purchaser purchases two or more dwellings in the same transaction, different tests determine whether the transaction is liable to the higher rates of tax. A transaction involving more than one dwelling will either be liable to the higher rates of tax or it won’t, the rules do not allow for a single transaction to be a combination of higher and normal residential rates.’

After significant public pressure, the Treasury has announced that they have agreed to relax these provisions. It now appears likely that the transaction will suffer the additional 3% only where the annexe represents a third or more of the total property value. However, at the time of writing, the proposed amendment to the draft legislation has not been published.

The annexe must be capable of being used as a separate dwelling, which means that it must have separate access and it must have the usual functionality of a place to live i.e. a bathroom and a kitchen.

Exemptions

Bulk purchases

Another surprise is the lack of any exemption for large commercial investors. The Treasury originally proposed an exemption for purchases of 15 or more properties and considerable time was invested during the consultation process on this point. The Chancellor decided that ‘the case for an exemption was not compelling’ apparently confident that ‘housing development will remain attractive for investors’.

Investors will be relieved to learn that bulk purchases of 6 or more properties will continue to be treated as non-residential and therefore subject to 5% duty (4.5% in Scotland). This is where some confusion could arise though, and in particular where the additional rate interacts with Multiple Dwellings Relief.

A claim for MDR brings the transaction back into residential rates. It involves dividing the total consideration by the number of dwellings, calculating the rate of duty that would apply to the ‘average’ unit and then applying that effective rate to the total number of units.

The rate of SDLT includes the additional 3%. However, under LBTT there is a ‘bulk purchase’ exemption from the additional 3% rate. This means that MDR is available in Scotland for the purchase of 6 or more units without the additional 3%.

Whether a claim for MDR is worth making will have to be assessed on a case by case basis. As the average unit price increases, so does the effective rate of SDLT per unit and a residential SDLT rate of 5% (which includes the 3% supplement) is reached at an average unit price of c. £333k. At average unit prices above this cut off, the buyer is likely to be better off with a commercial rate of 5%. For LBTT, an effective residential rate of 4.5% (disapplying the additional 3%) is reached at £c.485k.

Student housing

Under the proposed SDLT legislation, ‘… a building or part of a building counts as a dwelling if (a) it is used or suitable for use as a single dwelling, or (b) it is in the process of being constructed or adapted for such use.’ However, the types of accommodation used for a purpose listed in FA 2003 ss 116(2) and (3) are rendered not dwellings for these purposes. Student housing, being one of those listed, therefore escapes the additional rate of SDLT where it is so used. Student housing is not specifically carved out of the additional 3% LBTT.

Although student accommodation eludes the definition of a dwelling for higher rate purposes, it still falls within the definition of dwelling for the purposes of MDR. MDR can be claimed in respect of student housing at the usual residential rates of SDLT, ignoring the additional 3% charge. This is only the case for LBTT where 6 or more units are acquired, otherwise MDR is calculated using the higher rates.

Finally, it is noted that the drafting seems to require student housing to be ‘used’ for that purpose at the time of the transaction. What therefore is the answer where the accommodation is not so used because it is in the course of construction or renovation? It seems likely that a purposive construction should be taken here but HMRC consultation may be required.

Closing thoughts

There is no doubt that these higher rates of duty will have a significant impact on the market. One might think that by introducing the higher rates, the government is simply seeking to cash in on the rise of the housing market. Perhaps they have missed the boat, or perhaps the boat will now leave a bit faster.