Furnished holidays

Share this article

Liz Fisher considers the advantages of a property qualifying as a furnished holiday let

Key Points

What is the issue?

A furnished holiday letting (FHL) is subject to tax treatment that differs from that of other residential property income

What does it mean to me?

There are several detailed conditions that must be met for a property to qualify as an FHL and some important tax implications

What can I take away?

An overview of the relevant conditions that must be met in order for a property to qualify as an FHL & details of the elections available if the conditions are not met. Details of the main tax implications arising if a property qualifies as an FHL

Furnished holidays lettings have a lot going for them. The special regime accorded them includes tax advantages normally associated with trading properties, while the profits derived from the lettings are still treated as rental income.

To qualify as a furnished holiday letting (FHL), several conditions must be met:

- It must be within the UK (England, Wales, Scotland and Northern Ireland but not the Isle of Man or the Channel Islands) or the European Economic Area (EEA). The EEA comprises the member states of the EU plus Iceland, Liechtenstein and Norway.

- It must have furniture for ‘normal occupation’ and the tenants must be entitled to use it.

- The letting of the property should be carried out commercially with a view to profit.

- Three occupation requirements must be met as follows:

Availability threshold

During the year the property must be available for commercial letting as holiday accommodation to the public for at least 210 days.

Pattern of occupation condition

Longer-term occupation is defined as a letting of more than 31 days in the year but not for longer than 155. The property can be let for periods longer than 31 days in one stretch but none of the days will count towards the letting condition (unless the 31-day threshold is exceeded due to exceptional circumstances, for example a flight delay or illness which entails a person extending their stay). If the total of all or any longer-term occupation lettings is more than 155 days in the year, the property will no longer qualify as an FHL for that period.

Letting condition

During the year the property must be occupied by the public as furnished holiday accommodation for at least 105 days.

For all three occupational requirements the period in question is usually the tax year in which the owner of the property is an individual or a 12-month accounting period if the owner is a company. The only exceptions to this will be the years in which the letting starts and ends. On commencement the occupation requirements are applied to the first 12 months of letting and on cessation to the final 12 months.

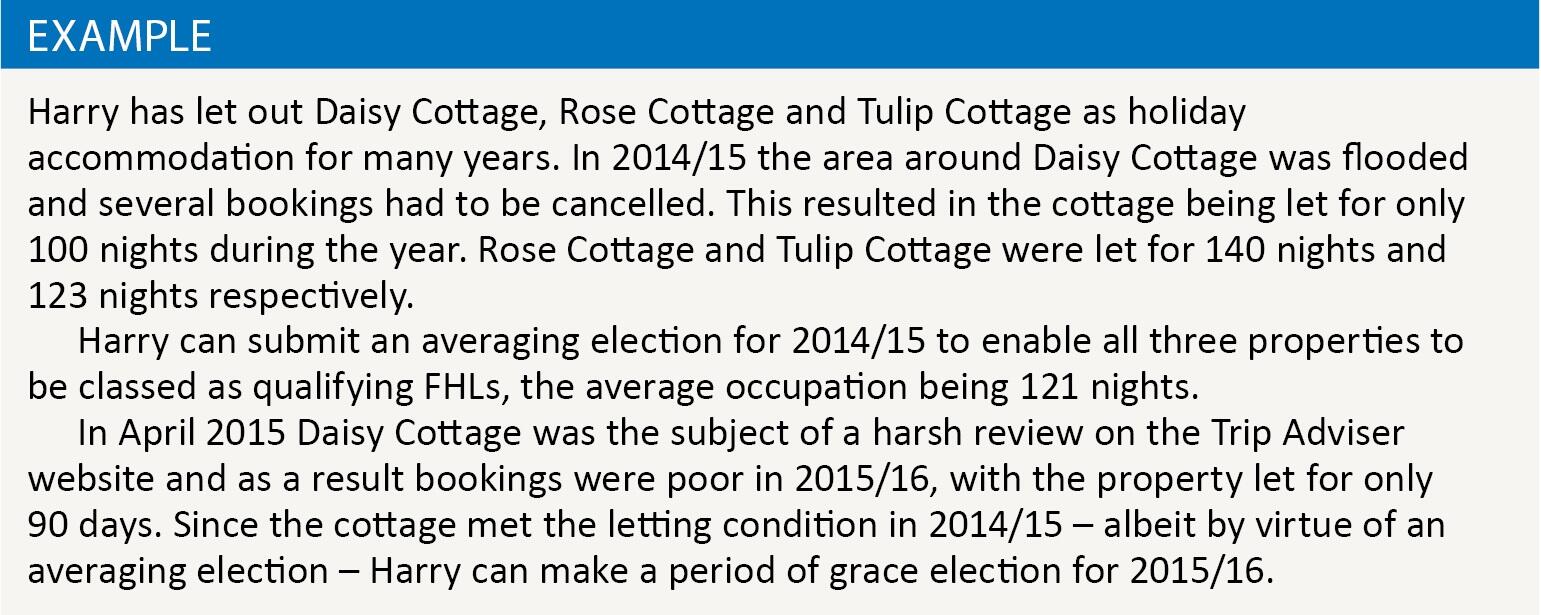

It is fairly common for the availability threshold and pattern of occupation requirements to be met but not the letting condition. This might occur if the weather over the summer is poor, in which case the owner may be able to make use of an averaging election or a period of grace election.

Averaging election

If more than one FHL is let and one or more of those properties does not meet the letting condition (but all of the properties meet the availability threshold and the pattern of occupation condition) an election can be made to average the rate of occupancy for all of the FHLs.

It is not possible to average lettings of UK FHLs with those in the wider EEA; they must be kept separate.

The election is made under ITTOIA 2005, s326 for individuals and must be submitted to HMRC on or before the first anniversary of the normal self-assessment filing date for the tax year.

Companies elect under CTA 2009, s268 and must submit their election within two years of the end of the accounting period in question.

Period of grace election

As long as there was a genuine intention to let the property and the letting condition was met in the previous year (even if this was by virtue of an averaging election) a period of grace election can be made.

Once an election has been made for one year it can be made in the next year too if the letting condition is still not met. However, if the condition is not met in the third consecutive tax year, the property will cease to qualify as an FHL.

The election is made under ITTOIA 2005, s326A for individuals and under CTA 2009, s268A for companies, with both submission deadlines being as for the averaging election.

Implications of a property qualifying as an FHL

Non-FHL letting income is usually taxed as investment income, whereas an FHL is treated as trading income for the purposes of some tax rules.

- Profits from an FHL are classed as relevant earning for pension contributions whereas other letting income is not.

- Capital allowances can be claimed on expenditure incurred for an FHL business, including on integral features. These allowances are not available on other residential property income.

- For capital gains tax purposes let property is classed as an investment. However, an FHL is classed as a business asset and will therefore qualify for three reliefs – entrepreneurs’, rollover and holdover – that are not available on investments.

- It used to be the case that losses from an FHL could be offset against other income. This changed from 6 April 2011. Now FHL losses can be carried forward and offset only against future profits from the same rental business. For this purpose a taxpayer’s UK FHLs are treated as one business and their EEA FHLs as another; losses from one cannot be offset against profits on the other. Nor can the losses be set against other non-FHL rental income.

- The provision of holiday accommodation is within the scope of VAT. Therefore if the income from the FHL exceeds the VAT threshold the owner must register for VAT. The supply will be standard-rated. Care should be taken if the sole owner of the FHL is also self-employed and making taxable supplies. In this case the turnover from the sole-trade and the FHL must be taken into account in determining whether the VAT threshold has been breached.

- No National Insurance is payable on FHL income.

- Although an FHL is treated as a business asset for capital gains tax purposes, it is unlikely to be so treated for inheritance tax and would not therefore qualify for business property relief (BPR) unless the owner was providing services significantly above what would usually be expected. Cleaning, garden maintenance and laundry constitute services that would usually be expected but if the owner provides meals or organised daytrips this might increase the chances of a successful BPR claim.

- FHLs are excluded from the rules announced in July 2015 that restrict relief for finance costs on residential properties.

Conclusion

Although the changes to the rules for using losses from FHLs removed one of the key tax savings available there are still significant tax advantages for owners of holiday lets. Record-keeping is crucial to ensure all of the conditions are met.