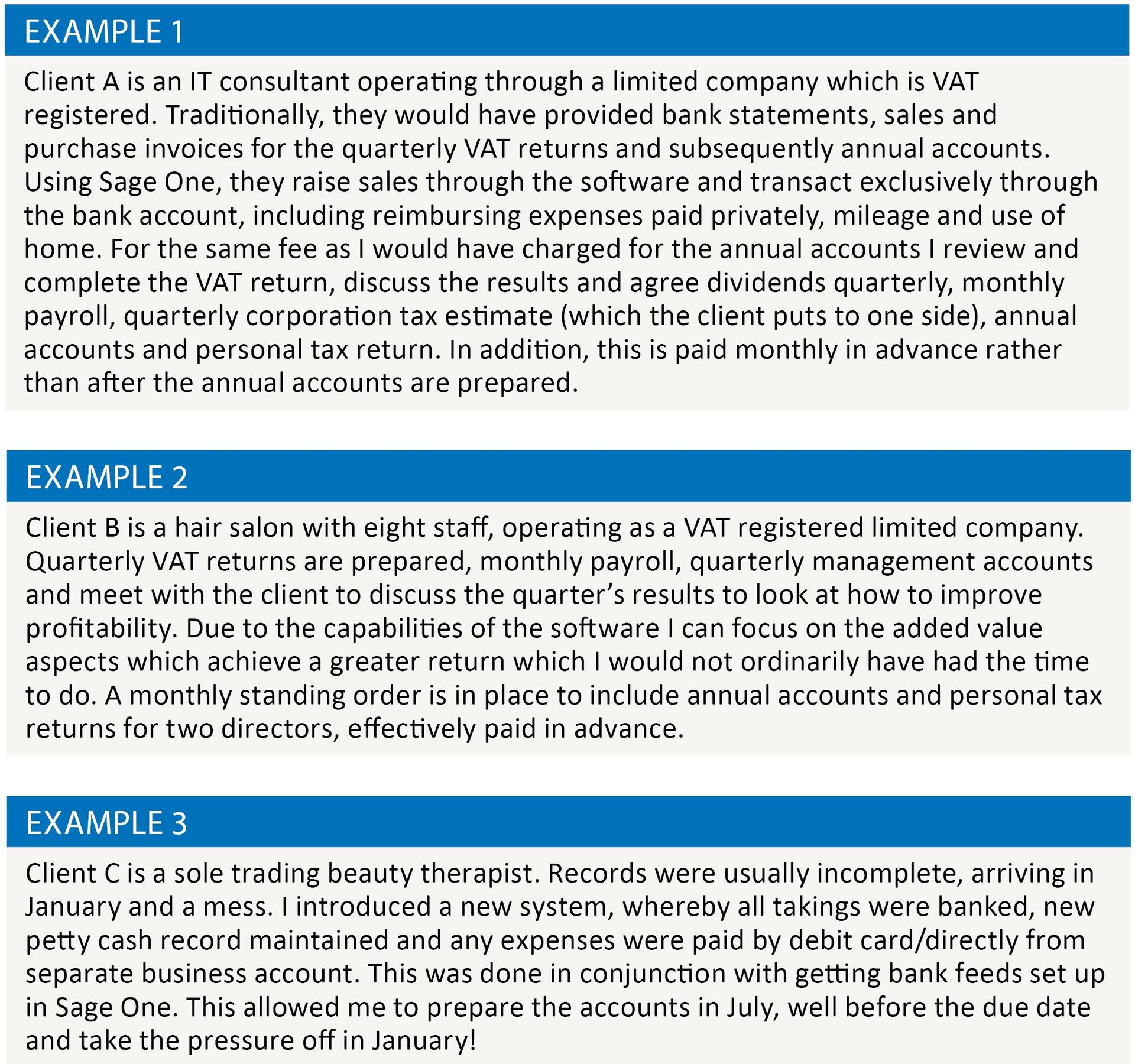

Getting your hands dirty

Share this article

Tim Andow provides a practical overview of considerations when planting seeds for a successful implementation of MTD

Key Points

What is the issue?

The Making Tax Digital proposals will become a reality very soon, and it is well worth getting ahead on your planning for this. It can seem daunting to know where to start with the cloud accounting products and how to communicate and implement the transfer of information to them with clients. Also, it is not always easy to see the advantages to the practice.

What does it mean to me?

There are many benefits to cloud accounting software, both on the time-saving aspects and on the ability to provide more profitable services to clients through timely tax planning and other proactive services.

What can I take away?

An overview of the opportunities cloud accounting software can give to a practice to become more efficient and profitable, and some practical advice on implementation of the systems needed to get the most from the software for both your business and your clients’ business.

Despite the recent announcement of the deferral of the implementation of Making Tax Digital (MTD) there are still many compelling arguments to adopt a cloud accounting package for clients. As a reminder, the system automates many aspects and allows you to provide more advisory and pro-active services than you may otherwise have been able to do. In addition, it gives efficiencies in processing information which could make previously unprofitable work profitable, less profitable work more lucrative and lucrative work super-lucrative.

The opportunities

In my mind, there is no doubt that the processing time for accounts preparation is going to reduce. Where clients are using cloud software you can access and review/amend the information throughout the year. When it comes to preparing accounts, you can go into the software, amend any items as necessary before entering any annual adjustments. From here, export the trial balance into your accounts package and its basically ready for review.

What now becomes more valuable is the opportunity to look at the information throughout the year and undertake tax planning, dividend strategies, and business improvement advice. Having up to date financials offers the Adviser the information to give pro-active, insightful comment which business owners can act on. Alternatively, you could choose to simply provide management accounts which add value to the client but are simple to produce, thus generating more revenue from minimal extra work.

In most cases you can have frequent contact with your clients, building stronger relationships as your understanding of the business and the client grows, leading to better advice, happier clients and less ‘churn’ in client numbers.

For those clients who do not want or need regular management information, the availability of the bank transactions in the software means you can prepare accounts earlier in the year, so you may consider targeting persistent late offenders! By having information earlier you can estimate tax liabilities earlier and look to reduce payments on account. Where clients claim tax credits, again, it allows the preparation of accounts earlier so final claims can be submitted for the July deadline, rather than being dragged out to later in the year and risking overpayment requiring clawback.

Planning work flow can be improved as the basic accounts information is available earlier.

Another advantage of the cloud software is that where you supply the package you can structure fee plans so you are paid monthly, smoothing income. I have found clients like the idea of a fixed fee spread over a period.

Software selection

This is probably the most important aspect of the whole process. I have used several different software packages (Xero, Sage One, Quickbooks Online and Kashflow) and they all have their merits for different clients. Some have more features, some have shortcuts to make entry quicker, the cost is different for different capabilities, some look prettier. My personal view is that you should not restrict yourself to one particular software package, instead have the ability to use several, which will give you the most options when trying to convert clients into a different way of working. Also, be mindful that some clients will be swayed by ‘friends’ who favour one product over another.

Don’t forget that there are some Excel based products which can create a trial balance to import into standard accounting software. This may be an option where the client is used to spreadsheets or the client doesn’t have internet banking.

Bank feeds

Cloud accounting packages rely on pulling through bank transactions from the clients online banking system. If a client doesn’t have internet banking this is your first obstacle! The bank feed is often set up by entering the online banking login details and ‘refreshing’ the feed. This will bring the transactions from a certain point in time into your chosen package. You need to consider the risks of who undertakes this aspect but if you get the client to input the details themselves this should mitigate any security concerns.

Once the data is in the system you need to allocate the items. Here you will get the option of selecting the relevant nominal heading and a VAT rate where applicable. Once you allocate an item the system automatically suggests the same nominal and VAT rate (e.g. if you post an item to accountancy and VAT standard rated, the next time that item occurs it will be pre-filled with those details).

If you have entered purchase invoices into the system, you can match the entry to the purchase invoice. The software will suggest a match and learns what goes with what.

If you raise sales invoices through the system then the software will suggest a match for the banked amount.

Bank transactions do not appear in the system until they are allocated, so by default you need to reconcile the bank to produce meaningful and accurate figures.

Non-bank items

If the business pays cash for any expense, it is my approach to bring this in via a weekly or monthly journal. Where the business owner pays for items personally, again, I consider it best to bring this in via a monthly journal.

Alternatively, if the owner is reimbursed from the bank account you can merely allocate the bank transaction when it appears from the bank rather than making the extra entry of a journal.

The same principal can be used for items like use of home and mileage claims. If they are physically paid from the bank account then you can allocate the payment rather than making an additional entry.

Grossing up adjustments may be required. This is where deductions are made before the transaction passes through the bank account, such as credit card charges deducted from takings banked or estate agents retaining management charges before paying rent to the landlord.

Depreciation and amortisation can be set up as journals and either be entered so they automatically recur each month or you can enter pre-dated journals for the year’s charge.

Sales

Where you raise sales invoices through the system it makes keeping on top of debtors relatively straightforward as you allocate the banking against an invoice to reconcile the bank.

If the business is cash based, such as a newsagent, I would have a slightly different approach. You can journal the weekly takings summary to create a cash control, credit card control and bank receipt control. Thereafter, the daily banking can be allocated to the appropriate control account.

Purchase invoices

As a suggestion, not all businesses need to maintain a purchase ledger. If you decide that you do need this, look very carefully at how best to get those purchase details into the system. There are several addon products which will produce a file to import from scanned purchase invoices. However, consider the cost of the addon and the time to scan the invoices in case that outweighs doing it another way. Some software allows you to list the information in a template csv file (which you can obtain through the software) and then import that into the system, making many entries relatively quick.

VAT basis

You may see that where everything is passing through the bank account a cash basis for VAT may seem logical. Careful consideration should be given to the cash flow effect this may have on individual clients, especially if they receive income ahead of paying creditors. However, if you work on a cash basis for a quarter and then journal in the trade creditors for the VAT at the quarter end you can get the best for your client but not substantially increase the work required.

Record keeping

In many smaller businesses, the record keeping can be much simplified, especially if the bank transactions form the basis of the accounts. I usually recommend an A–Z indexed file for paid purchase invoices. Unpaid invoices are kept in a separate ‘unpaid’ file. Paid sales invoices are filed in numerical order with unpaid sales kept in a separate file.

System set-up

This is a fundamental part of the process and it cannot be underestimated how important this is, especially where clients are allocating or entering information themselves. The chart of accounts should be structured to reflect the management information required and also so it can easily be transferred into statutory format (whether limited company or onto a tax return). Do not have duplicate or ambiguous headings where clients could misinterpret where to put something, as you will want to reallocate as little as possible. Be aware that some systems do not allow you to delete certain codes or where a transaction is included on a VAT return you may only be able to make limited changes, if any.

Client education

The critical part to embracing this and the opportunities it can create is to educate clients to operate in a way that makes the most of the software. For example:

- Keep a separate business bank account (this is ok for limited companies but not all smaller businesses may currently operate in this manner)

- pay for everything from the bank account using direct payment or debit card

- do not use cheques

- bank takings intact (or with minimal cash deducted before banking)

- keep a separate petty cash system where cash is withdrawn separately

- if the business owner wants to keep a ‘wage’ get them to set up a standing order or make a separate withdrawal

Which clients to convert and when?

The deferral of MTD now allows a more planned conversion of clients. Some will be up for it as soon as you mention it whereas others will resist right up to the point it becomes mandatory.

A strategy for implementing the new system will be important, especially where some banks only allow a limited backdating of the bank feed, so you may consider that a yearend or VAT quarter end is most appropriate.

Other considerations

Where a client has a bookkeeper, you need to get them on-side. They may resist as, if they have limited capabilities or capacity, they will see the amount of work they need to do will diminish which obviously reduces their income.

As a strategic move, I can see that there may be alliances forming between bookkeepers and accountants. However, to what extent that becomes appropriate for individual firms is yet to be seen. Alternatively, I can foresee a rise of in-house processing staff who have less technical skills than accountants/tax advisers but who are extremely adept at getting information into the system to allow the higher value work to be done in a timely manner.

Conclusion

Even though the date from which mandatory Digital Record Keeping has been deferred, it is important to keep those reporting capabilities in mind and take a longer-term view.

Experimenting with different packages and different methods of entry to see what works is essential. I put my practice onto Sage One early on so I could see what worked and what opportunities it gave. Like anything, there is no substitute for getting your hands dirty!

The practice business model will need to be reviewed. A strategic view of when to convert clients, what services to offer, how to package those, the opportunities to upsell to clients and, therefore, the effect on the practice’s cash flow now and into the future will need to be taken.