A global issue

Share this article

Increased globalisation in recent decades has changed the way in which multinational enterprises conduct their business across the world. Vanesha Kistoo and Mark Abbs consider the options.

Key Points

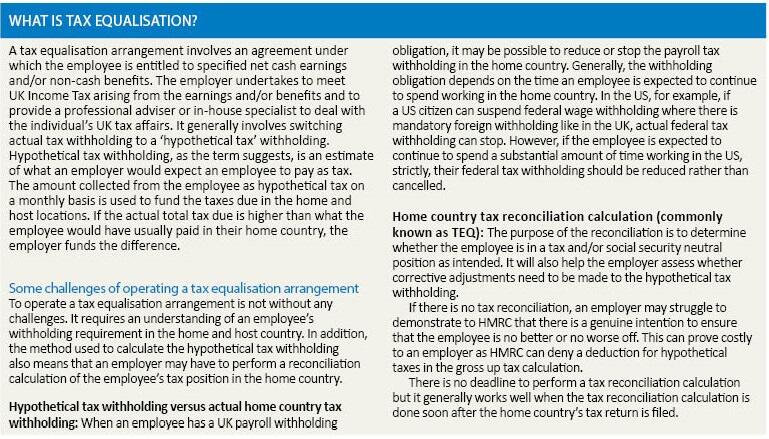

What is the issue?

HMRC recognise that for internationally mobile employees, employers are faced with challenges. Therefore, HMRC offer a concession to help address complex payroll issues in multiple countries.

What does it mean to me?

As payroll reporting in the UK is on a real time basis, employers who need to operate a UK and a non UK payroll for their expat population often struggle to comply because payroll deadlines do not align or they simply do not have enough resource to manage a dual payroll reporting properly. With the zero tolerance approach being adopted by HMRC, we have outlined a welcome payroll concession that may be relevant.

What can I take away?

Usually, the payroll options are a standard payroll or a shadow payroll. However, there is an alternative and it is a modified payroll but it comes with responsibilities which should be complied with.

Increased globalisation in recent decades has changed the way in which multinational enterprises conduct their business across the world. More freedom from restrictions, ease of travel and communication, together with the growth of new markets has contributed to a wider spread of activity. As part of this trend to increased globalisation, movement of employees across borders has evolved, from a pattern of extensive assignments to one of increasingly short term engagements by internationally mobile employees. Payroll reporting in the UK is not only relevant to UK employers but also non UK employers under the ‘host’ employer rules. This article looks at a modified payroll arrangement, the responsibilities and challenges.

Modified payroll arrangement

This is a more relaxed payroll reporting approach which can be adopted where an employer has employees who need to remain on their home country payroll but have host payroll reporting obligations.

The reporting under RTI is done on an estimate basis but the arrangement comes with responsibilities which should be complied with to avoid penalties.

Who can be reported on a modified payroll arrangement?

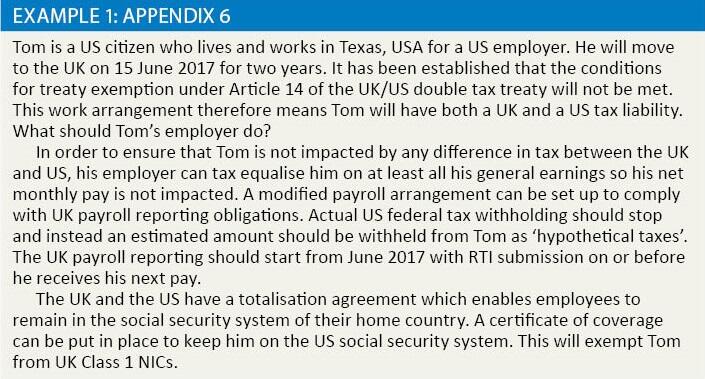

This payroll arrangement only applies to employees who are tax equalised on all their general earnings under part 2 Chapters 4 and 5 of ITEPA 2003 for UK income tax.

Employees who are not tax equalised on specific employment income, i.e. they are responsible for the UK tax/social security on employment related share awards, can be included under a modified payroll arrangement provided the other conditions are satisfied.

Putting in place a modified payroll arrangement

The first step is to determine which application(s) need to be made. For employees who come to work in the UK there is one application for tax withholding and another for social security withholding; appendix 6 and appendix 7a. Employees can only be covered by an appendix 7a agreement if they are under an appendix 6 arrangement. Where employees leave the UK to work abroad and continue to have a UK social security withholding obligation, then the relevant application is appendix 7b.

Appendix 6

Such an agreement is relevant for overseas employees coming to work in the UK, and broadly, the rules for these modified payroll schemes are:

- All general earnings are tax equalised;

- At the start of each tax year the employer estimates the total taxable pay (including benefits) for the year and calculates the estimated annual tax liability which is spread out in the tax year;

- A review should be carried out between December and April in the year to adjust for material changes, bonuses, share gains, etc.;

- The deadline to submit modified form P11ds is 31 January following the end of a UK tax year;

- A self assessment tax return should be filed by the employee and further liability due is settled by the employer;

- Quarterly payment of PAYE to is due to HMRC where the total number of employees does not exceed 5. If the total number of employees exceeds 5, payment of PAYE changes from quarterly to monthly from the beginning of the next tax year and vice versa where the number falls to below 6;

- PAYE due can be adjusted for foreign tax where an agreement has been reached with HMRC;

- PAYE can also be adjusted for employee contributions into an overseas pension scheme where the employee qualifies for tax relief in the UK.

See example 1: Appendix 6.

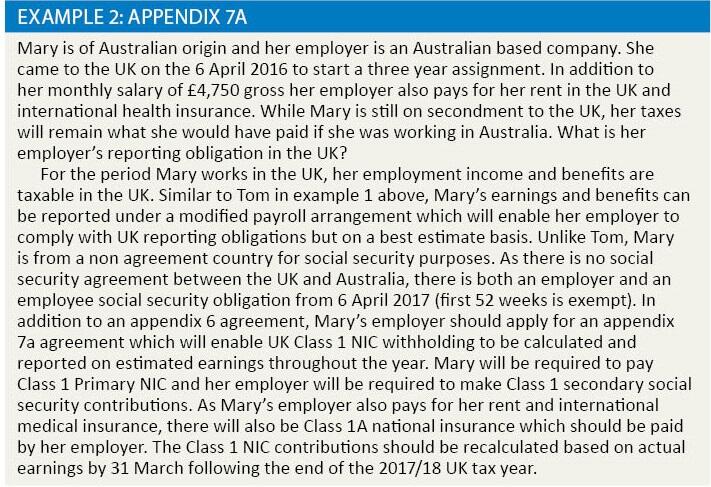

Appendix 7a

In summary, the rules under a modified social security arrangement for overseas employees working in the UK are:

- The scheme only applies to employees under an appendix 6 agreement;

- Similar to the appendix 6 agreement, at the start of each year the employer estimates the earnings, including non cash benefits subject to Class 1 NIC for the year, calculates the estimated annual NIC liability and pays 1/12th of that tax each month;

- A review is carried out in December to April in the year to adjust for material changes;

- If there is additional Class 1 or Class 1A NIC, the amount must be paid by 31 March following the end of the tax year;

- Annual NIC settlement prepared to reconcile NICs.

See example 2: Appendix 7a.

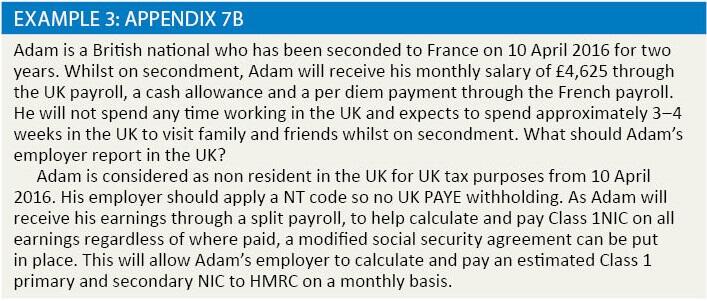

Appendix 7b

The rules for a modified social security arrangement for employees assigned from the UK to work overseas are:

- The scheme applies to employees assigned to work outside the UK for more than one complete UK tax year;

- The employee breaks UK residence;

- The employee does not have UK taxable earnings but they remain liable to UK NIC;

- At the start of each year the employer estimates the earnings, including non cash benefits subject to Class 1NIC for the year, calculates the estimated annual NIC liability and pays 1/12th of that tax each month;

- A review is carried out in December to April in the year to adjust for material changes;

- The deadline to submit form P11ds is 31 January following the end of a UK tax year;

- If there is additional Class 1 or Class 1A NIC, the amount must be paid by 31 March following the end of the tax year;

- Employees must be paid at a rate above the Upper Earnings Limit (UEL) throughout the year except in arrival and departure months, which may be a part month.

See example 3: Appendix 7b.

Conclusion

The current trend in employee mobility indicates a growth in short term (training related) assignments and short term business travellers. Although there are regulations and guidance in place such as the OECD model and social security agreements to harmonise cross border tax and social security reporting, they do not offer a solution all the time. A modified payroll arrangement can help, especially for employees who spend time working in countries which are more challenging than others such as Brazil, Russia, India, China and the USA. A modified payroll arrangement can help with cash flow and the employer can report best estimates so there are no penalties provided the terms and conditions of the arrangement are complied with. Interest and penalties still apply to tax and NICs paid late