Good Tax – the tax cost

Share this article

Mark Groom considers the main tax and NIC issues related to the determination of status issue

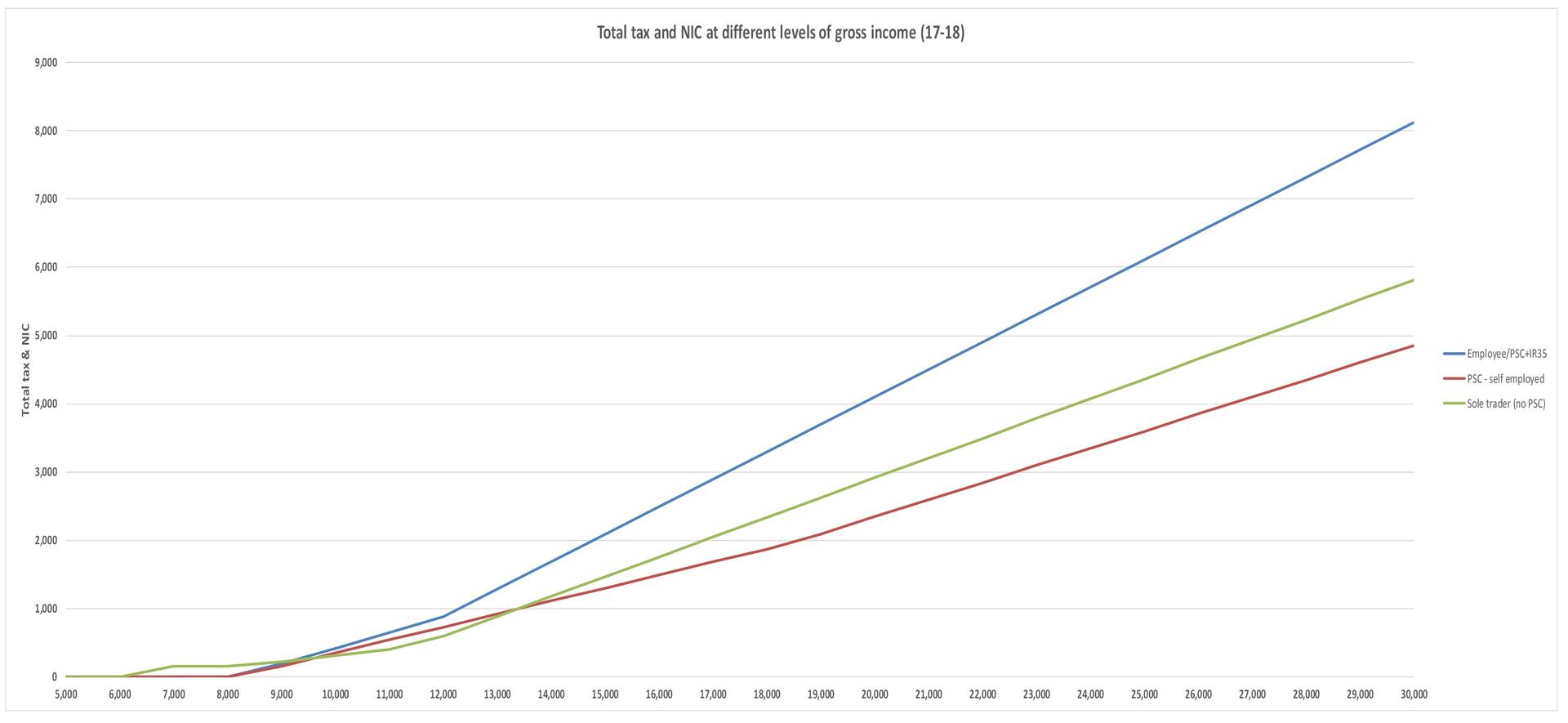

Tax burden is highest amongst employees (and PSCs where IR35 applies), followed by self-employed sole traders, with the least amount of tax being paid by PSCs where IR35 does not apply. A graph of the total tax and NIC paid by each category is provided below.

The difference between employed (blue line) and self-employed (green line) is £1,746 at earnings of £25,000, and is accounted for mostly by employer’s NIC. The difference between the self-employed line and the red-line (PSC where IR35 does not apply) is a further £766, and is accounted for mostly by the rate of corporation tax, which is planned to reduce further over coming years, making incorporation even more tempting.

It is sometimes suggested that a lower rate of NIC for the self-employed incentivises and/or rewards entrepreneurialism, risk, flexibility, and job creation associated with self-employment. No one would argue against these positives and we would canvass for wider tax policy to ensure they are fully supported in one way or another. However, I am not convinced that entrepreneurs are who they are as a consequence of the NIC regime. As advocated by the Institute of Fiscal Studies and many people more learned than me, there are plenty of other ways to provide a more causal link between fiscal incentives and desired outcomes.

I would only add that we really need a modern reassessment of the full economic and fiscal impact of any proposed changes, before we can consider moving forward with any potential alternatives.

Getting it wrong

Many contractors will happily engage on a self-employed basis for years enjoying paying tax through self-assessment and NIC at the lower Class 2/4 rates. Funny though how, when things go wrong, they suddenly consider themselves employees or workers, usually claiming holiday pay, unfair dismissal, and these days possibly also NMW/NLW and auto-enrolment pension contributions.

If employed status is upheld, the employer can also be liable for significant additional PAYE and primary and secondary Class 1 NIC liabilities. PAYE liabilities can sometimes be extinguished through a direction under Regulation 72F of the PAYE Regulations, whereby HMRC will check the tax has been self-assessed instead of insisting on collection through PAYE. In that case, the principal liability remaining will be the 3% difference between Class 4 and primary Class 1 NIC, plus 13.8% secondary Class 1 NIC. Where a number of contractors are involved, and possibly a number of tax years, the amounts soon add up. Exactly the same situation arises if the employer has simply made a mistake in its assessment of employment status which HMRC successfully challenges. It is wrong that businesses can be left with crippling liabilities, and often lengthy court proceedings, simply as a result of vagaries in our definitions of employment status.

Most engagers cannot afford to take these risks, so unless they are absolutely certain that someone will be classified as self-employed, they can mitigate their risk by engaging workers through a personal service companies. In my experience, tax avoidance by the engager is rarely a consideration, although avoiding additional head-count and additional employment related costs maybe. The tax treatment adopted by the individual should depend on whether or not IR35 applies.

Incorporation

Under current rules, where a private sector company pays a PSC, and IR35 is found to apply, the PSC will be liable for any PAYE/NIC. If the individual in that PSC is providing the services of a director to its client, the client should arguably account for PAYE/NIC on payments to the PSC under s62. Since 2013, the PSC is also liable under IR35 in such circumstances, giving HMRC two bites at this sour cherry. It is hardly satisfactory to leave the client and the PSC to fight it out as to who should pay these liabilities.

To make matters worse, if the client pays, Reg 72F will not provide them with any offset facility as noted above. This is because the PSC will have paid corporation tax and the individual will have self-assessed dividends, and the payment made by the client will not therefore be in respect of income which has been self-assessed. Since April 2017, where a public authority pays a PSC and IR35 is found to apply, the public authority is liable. A Reg 72F offset might be available in this situation, but remains untested as yet.

Individuals who are not directors of their client, who fall liable under IR35, can experience considerable distress if they are asked to settle the gross PAYE/NIC arising, without being told they can claim repayment of any corporation tax and/or dividend tax they may have paid. If we are trying to help taxpayers pay the right amount of tax at the right time, it seems equally important to help get them back to the right amount of tax if things have gone wrong.

We are awaiting a separate consultation, not part of the Matthew Taylor current quartet, on extending public sector IR35 to the private sector, so that whoever pays the PSCs will be liable if IR35 applies, whatever sector they are in. HMRC has been reported as saying that the public sector measures have worked well, that c.90,000 new public sector PAYE registrations have been made since the rules were introduced, and that the loss of tax in the private sector due to non-compliance with IR35 could rise to c.£1.2bn per annum by 2022/23. If this is true, combined with the obvious merit in levelling the playing field between the two sectors, the question seems to be when, rather than if this will happen, just as it was proposed 18 years ago. In order to fully take on board the learning points from the public sector implementation of the rules, extrapolated over a significantly broader private sector base, I would be concerned if this was any sooner than April 2020. I refer you to Lesley Fidler’s article on IR35 in the public/private sector for more detail on this highly emotive area.

Equalising tax and NIC rates

I think most people agree that, if we are to retain different statuses for tax purposes, part of any future solution should be to overhaul the definitions of the various statuses as discussed above, to achieve greater clarity and certainty in reaching the correct status classification (once we know how we want each to be defined). However, is this bold enough?

Our Chair, Colin Ben-Nathan, made the excellent suggestion of replacing employer’s NIC with some sort of consumption tax. I had also considered that a levy could be charged on payments by business to anyone who personally provides service, be they workers, fully self-employed or employees. Such a levy would replace employer’s NIC and would only not apply to fully outsourced services. We’re on the same page.

The Office of Tax Simplification (OTS) also considered replacing employer’s NIC with a payroll tax which should be calculated on an Annual, Cumulative, and Aggregated (ACA) basis. This would address the issue of employees working in several part time employments, each one below the Primary/Secondary Threshold, thereby avoiding NIC on all of them. In contrast, someone in a single employment earning the same amount in total, would exceed the thresholds and the excess would be subject to NIC in full.

ACA was a brilliant suggestion as it would prevent this inequity, but further research by the OTS showed there would be too many winners and losers. However, it would be interesting to model where the breakeven point would be and how many winners and losers would arise, if a new levy on personal service was introduced across all workers.

Workers under PAYE/NIC?

I turn to the question of whether bringing Workers (particularly those in the gig-economy) into the PAYE/NIC regime, would raise any more tax or NIC. Well, such is the nature of gigging, that they can work for whoever they like, whenever they like. Say a gigger currently works for three engagers earning £8,000 from each of them. Being self-employed, the gigger includes his/her total earnings of £24,000 as income from his/her trade, which exceeds the Class 4 Lower Profits Limit (currently £8,164) and so pays Class 4 NIC of £1,425 (9% of £15,836).

Now, say, the rules are changed so the gigger is taxed as an employee. Unless the NIC regime is put onto an ACA basis, the amount of NIC that would be raised will be NIL, assuming the three sources of income would be treated as separate employments and not aggregated. So this move would cost £1,425 in lost Class 4 NIC.

As for tax, well that depends on whether or not you believe the gigger is declaring all their income. If so, this change should really only impact cashflow, but not make a material difference to total tax payable given that unlike NIC, tax rates are sensibly the same for employees as for the self-employed. It may be easier to claim relief on some expenses but at this level of earnings, something’s probably wrong if material levels of expenses are being claimed. If not, then applying PAYE or some other system of withholding would make sense.

Summary

This short paper cannot possibly surface all the issues that need to be thought about, but if it brings together things that people are already starting to discuss and crystallises any other thoughts, that will at least be something. Any change to social security needs to be thought through at an international level, and I haven’t mentioned VAT once, but of course, VAT is also relevant when considering incorporation and when moving people from self-employed to employed tax status or vice versa. I therefore conclude as I started, encouraged by the debate the government has started through its consultations (with more to follow), but still hoping for a detailed tax and economic review of all these issues to ensure the success of any future framework adopted.