A grey area of VAT

Share this article

Neil Warren gives some practical examples of VAT issues on business sales and highlights potential pitfalls and planning opportunities

Key Points

What is the issue?

If key conditions are met the sale of a business will be outside the scope of VAT in most cases, ie avoiding an unnecessary VAT charge

What does it mean to me?

Both buyers and sellers need to take great care to ensure the correct VAT treatment is applied because large amounts of tax are often involved in business sales

What can I take away?

It is possible for the sale of part of a business to qualify for TOGC treatment and HMRC may allow an input tax claim by a buyer in some cases where TOGC treatment should have applied if they are satisfied, however, that the seller has accounted for output tax

Here is an opening question: on which particular aspect of the VAT legislation will HMRC normally (possibly always) refuse to give a written ruling? The answer is whether the sale of a business sale qualifies as a transfer of a going concern (TOGC) and if the proceeds are therefore outside the scope of VAT if certain conditions are met by the buyer. HMRC’s policy on giving rulings (or clearances to use the more commonly used phrase) is that the legislation or guidance on a particular issue must be unclear before the department puts pen to paper. In the case of the TOGC rules, the guidance is pretty clear in both VAT Notice 700/9 and HMRC manual VTOGC.

So why does this subject often cause big problems for advisers? The reason is because it is often a ‘grey’ area as to whether business assets are being sold (subject to 20% VAT in most cases) or an actual business when the proceeds are usually outside the scope of VAT, that is, because the legislation deems that neither a supply of goods or services is taking place (Value Added Tax (Special Provisions) Order 1995, Art 5(1)).

Is a business being sold?

I was recently asked by an accountant if the sale of stock between two associated businesses in the UK related to a TOGC. The basic scenario was that the first business selling sports equipment was transferring its activity to the second company, so that it could wholly concentrate on providing services in the sporting sector. So the second company would handle all future sales of the goods in question.

In this situation, it is important to consider whether the buying company is acquiring any other benefits (apart from the stock) as a result of the transfer, in other words, that indicate a business sale is taking place:

- Are there existing orders that will transfer to the second company?

- Is there a trading name that will be utilised by the second company that has some prestige or market status in the sporting industry?

- Will the second company take over a list of potential customers with which it can do future business? And possibly a list of suppliers that provide favourable discounts and good credit terms?

- What about staff and premises – will these transfer to the second company?

An important tip is that a payment for ‘goodwill’ by the buyer is an indicator that there is a TOGC, but this is not always the case. Some businesses may have performed so badly that goodwill is not relevant.

So the key to dealing with VAT is first to identify whether a business has been sold and then consider whether the deal meets the TOGC conditions in the legislation as far as the nation’s favourite tax is concerned.

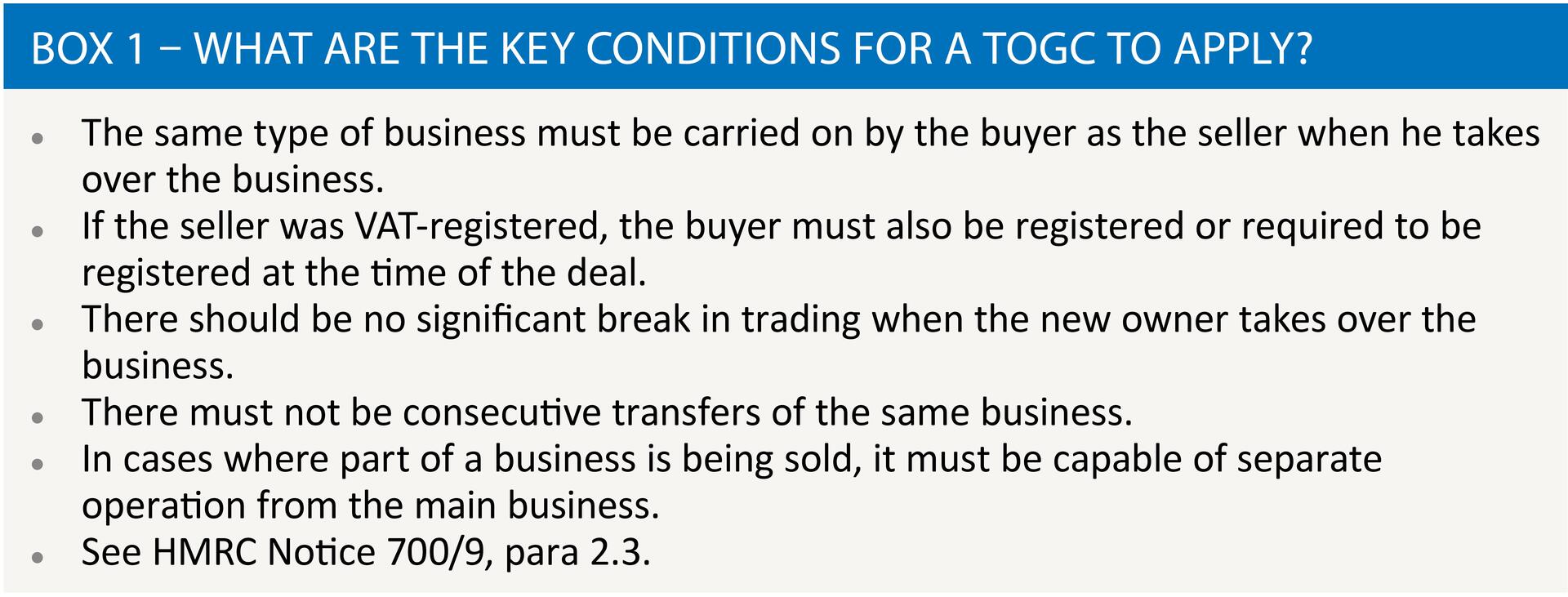

Key conditions for a TOGC

The main TOGC rules are shown in Box 1. Each of the six bullet points presents a specific challenge. For example, I had a very worried accountant phone me last year, whose client was selling a nursing home and he was concerned that the buyer was not VAT-registered. This was not a problem because the seller was not registered either because his income was exempt from VAT. And even if the seller was registered, the buyer would not be liable to be registered if he only had exempt income from elderly care services.

A frustrating issue for buyers in recent years has been the delays getting VAT numbers from HMRC in many cases because of its checking of applications for possible carousel fraud. There have been many deals in which we have had to rely on the words ‘required to be registered’ because no VAT registration number had been issued by HMRC to the buyer before the sale. What does this mean exactly? The answer is that when a buyer determines their date of VAT registration, they must take into consideration the taxable sales of the seller. So if the seller had taxable sales of more than the annual registration threshold in the 12-month period before the transfer, the buyer is ‘required to be registered’ from their first day of ownership.

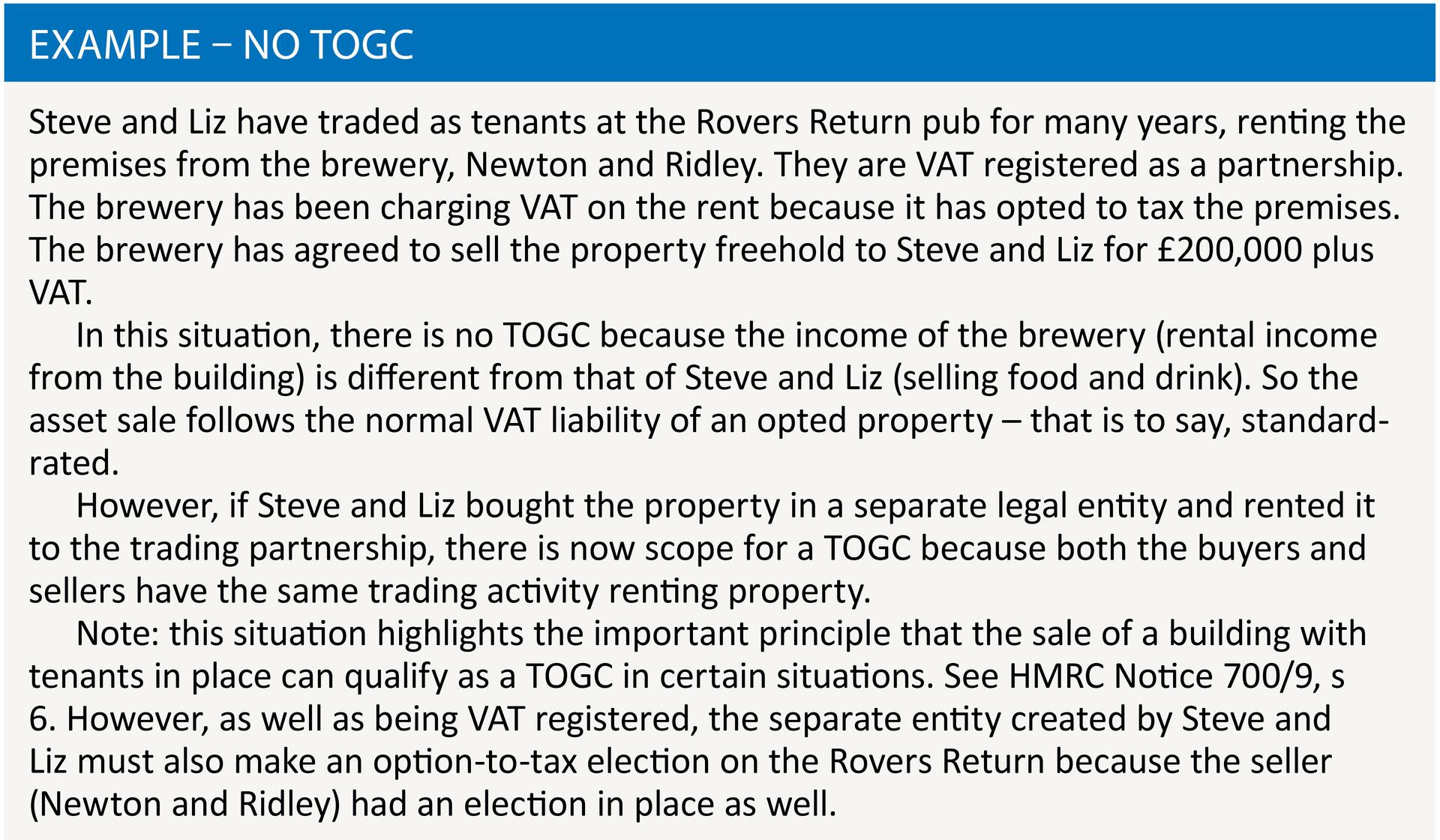

A potential pitfall and planning opportunity with the first bullet point in Box 1, on the need for the buyer and seller to have the same trading activity, is shown in the Example.

As an aside, with Steve and Liz’s tax planning, there is no problem with their tax planning arrangement as far as anti-avoidance legislation is concerned. This taxable (no input tax block under the rules of partial exemption). But if their trading business had been exempt or partly exempt and the property value was within the capital goods scheme (net cost exceeding £250,000 excluding VAT), they would need to consider the anti-avoidance legislation (HMRC Notice 742A, s 13).

Warning … input tax for buyers

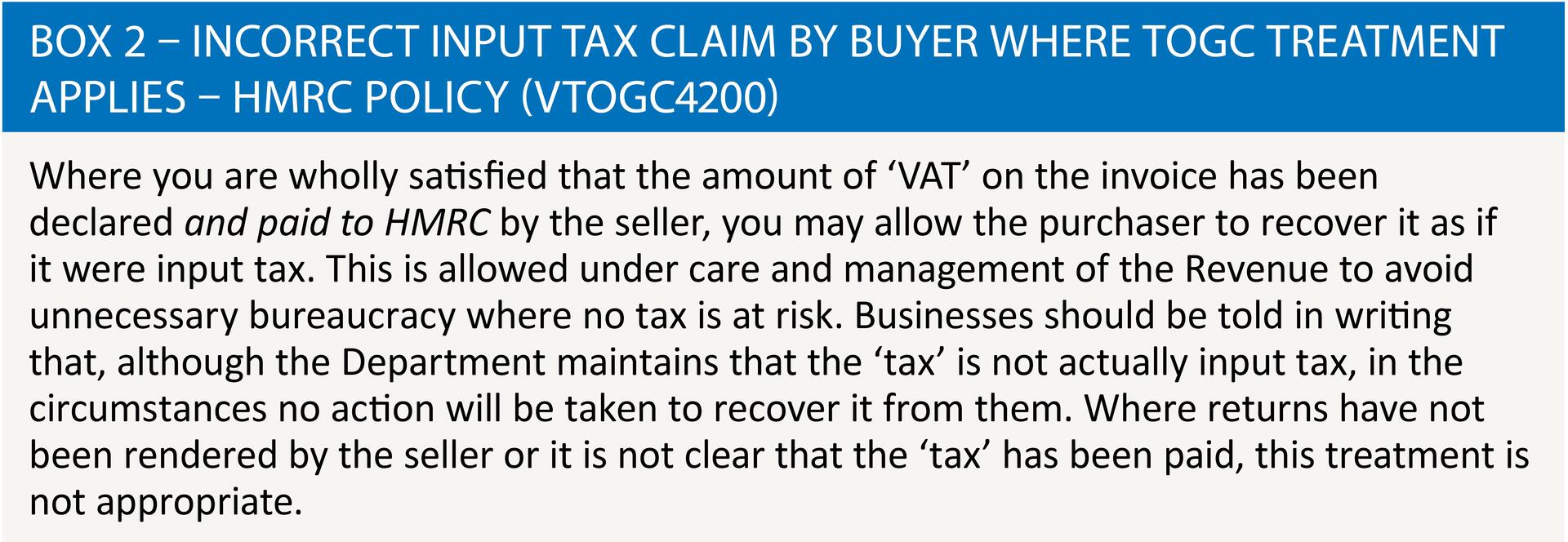

What is the worst-case scenario with a TOGC deal? It is probably the situation where a seller incorrectly charges VAT on the proceeds, helped by a complacent buyer who takes the view that VAT is not a problem because their business is fully taxable (like Steve and Liz trading as a pub) and therefore they can claim input tax as long as they get a tax invoice from the seller. However, this approach is totally flawed. A condition of claiming input tax is that it can only be claimed by a business if VAT has been correctly charged in the first place. So what would happen if I bought a tax practice from a seller who incorrectly charged me VAT on the proceeds? An incorrect tax invoice issued by the seller is not an HMRC issue – it is a commercial issue between the seller and me. But there is potential good news to dig me out of a very deep hole – and that is the potential discretion given by HMRC if it is satisfied that the seller has declared and fully paid the incorrect VAT – see Box 2.

Note: the correct approach in my example would be for me to go back to the seller when I first discovered that the VAT charge was incorrect and ask them for a VAT credit.

Conclusion

The issue of whether a TOGC is evident depends on a clear analysis of all relevant arrangements to determine the VAT position (substance over form). The rules are not optional, so neither the buyer nor seller should ‘play safe’ and allow an incorrect VAT charge and hope that the buyer can claim input tax.

To share a final story, I was asked to advise on a hotel sale in Devon about ten years ago. The deal was taking place in October and the seller was keen to charge VAT on the basis that the hotel was seasonal and the buyer would not trade again until the next April, in other words, producing a ‘significant break in trading’ after the sale and therefore failing one of the TOGC conditions. The seller’s proposal was incorrect because seasonal issues are ignored. See HMRC Notice 700/9, para 2.3.6.