Health and Social Care Levy

Share this article

Bill Dodwell summarises the tax changes announced in the Health and Social Care Levy Bill

On 9 September, the Prime Minister announced to the House of Commons (see bit.ly/2XgFe6B ) that the government would:

‘…create a new UK-wide 1.25% health and social care levy on earned income, hypothecated in law to health and social care, with dividends rates increasing by the same amount. This will raise almost £36 billion over the next three years, with money from the levy going directly to health and social care across the whole of our United Kingdom.’

Details of the changes were published by the government (see bit.ly/3hzcjSn) with a distributional analysis (see bit.ly/3nClsgZ). The House of Commons supported the measures with an indicative vote on 8 September.

From 6 April 2022

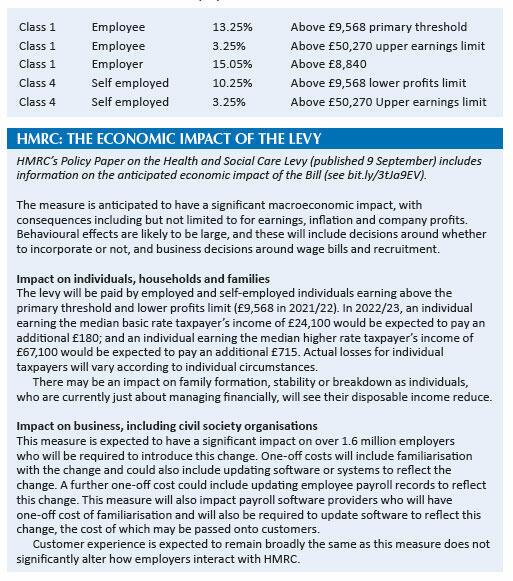

From 6 April 2022, the rates of Class 1 and Class 4 national insurance will be increased by 1.25%, to become those shown in the table on the right. There are no changes to Class 2 (self-employed) or to Class 3 (voluntary contributions).

The rates of income tax on dividends will increase by 1.25% from 6 April 2022 and will become 8.75% (basic rate); 33.75% (higher rate); and 39.35% (additional rate).

From 6 April 2023

From 6 April 2023, a new Health and Social Care levy will be introduced at 1.25% and the national insurance rates will be reduced by 1.25%.

The levy will be payable by employed and self-employed individuals, including those above state pension age in relation to their employment/self-employment income.

The national insurance threshold of £9,568 (individuals) and £8,840 (employers) will also apply to the levy, which will use the national insurance base and be collected through PAYE or Self Assessment.

Existing NICs reliefs to support employers will apply to the levy:

- Companies employing apprentices under the age of 25, all people under the age of 21 and veterans will not pay the levy for these employees as long as their yearly gross earnings are below £50,270.

- Employers in freeports will not pay the levy for freeport employees with yearly gross earnings below £25,000.

The Employment Allowance, which reduces the smallest businesses’ employer NICs bills by up to £4,000, will also apply to the levy.

Forecast

The government will present detailed figures on the revenue raised at the next Budget. It estimates these changes will raise about £12 billion annually, of which £11.4 billion will come from NIC/the new levy and £600 million from the dividend tax increase.

The government will provide additional funds to compensate departments and other public sector employers in England at the Spending Review for the increased cost of the levy and provide Barnett consequentials on this funding to the devolved administrations.