The hidden economy: how to improve compliance

Share this article

We consider the findings of research commissioned by HMRC into the hidden economy, the latest tax gap statistics and what more could be done to improve compliance.

Key Points

What is the issue?

HMRC research shows almost 9% of UK adults participate in the hidden economy. Its estimates indicate that 30% of the tax gap arose due to evasion-type behaviour. HMRC needs to tackle this to increase compliance and tax collections.

What does it mean to me?

Forthcoming measures such as digital platform data sharing and, potentially, adopting the OECD’s Cryptoasset Reporting Framework should help HMRC to increase compliance activity in this area.

What can I take away?

While those in the hidden economy tend not to have advisers, when they choose or are nudged towards compliance and filing returns, it is important to ensure their past is regularised via disclosures too. Taxpayers may benefit from being made aware of new data sharing provisions in case this also prompts them to correct historic mistakes.

Improving tax compliance so more people file correctly and on time is one of HMRC’s key aims. The Public Accounts Committee’s May 2023 report (see tinyurl.com/2hn24ch9) demonstrated that HMRC remains under pressure to ‘ensure it is never easier to cheat the tax system than comply’ and to help those who want to pay their taxes correctly. Consequently, HMRC seeks to estimate the tax gap and better understand why some people consistently do not meet their tax obligations and to help it tackle non-compliance: its findings shed light on what advisers may expect next from HMRC.

The tax gap

On 22 June 2023, HMRC published its latest estimate of the 2021/22 tax gap (see tinyurl.com/a83f6da5). The tax gap is the difference between the tax that HMRC thinks should, in theory, be paid and the amount actually paid.

Its causes include non-payment, simple mistakes, carelessness, fraud (deliberate wrongdoing), tax avoidance, organised crime and differences in legal interpretation of tax laws.

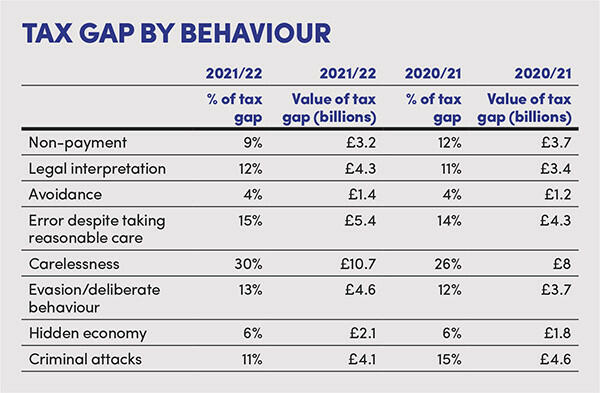

The figures show that the tax gap remains unchanged – stubbornly high at 4.8% of total liabilities. However, while the percentage remained constant, the estimated monetary total increased by £5 billion to £35.8 billion. HMRC’s statistics categorise the tax gap by taxpayer behaviour, tax and taxpayer type. Individuals and small businesses accounted for 62% (£22.1 billion) of the tax gap, up from 59%. Income tax, NIC and capital gains tax together comprise the largest ‘tax type’ segment at 35% of the tax gap (£12.7 billion).

As in 2020/21, ‘carelessness’ was the biggest behavioural cause of the tax gap: up 4% at 30%. Given the amount of media publicity it receives, some may be surprised to see that tax avoidance is again the lowest contributor but this illustrates HMRC’s successes from focusing on promoters and scheme users over recent years.

Together ‘evasion’, the ‘hidden economy’ and ‘criminal attacks’ comprise 30% (£10.74 billion) of the tax gap, down from 33% for 2020/21. HMRC had some success tackling criminal attacks. More could be done by its Fraud Investigations Service if HMRC can identify taxpayers to target. HMRC’s 2022/23 statistics show the number of suspected serious fraud investigations under Code of Practice 9 fell (more cases were closed than opened) (see tinyurl.com/bddvbcup). However, a different approach may be needed on the hidden economy.

Hidden economy

HMRC defines the ‘hidden economy’ as economic activities which are entirely hidden from HMRC. HMRC is so concerned about this that they recently released new research on it, ‘The hidden economy in the UK: wave 2’ (see tinyurl.com/2p9yhxhb).

It estimates that 8.8% of UK adults participate in the hidden economy, up from 4.8% in its 2017 research, which is perhaps unsurprising given the growth in digital platforms over the period. Participation was split between three key types of behaviour:

- ‘moonlighters’, whose hidden economy activity supplements declared activity;

- ‘ghosts’, who have not declared any of their sources of income; and

- VAT non-registered businesses, despite their turnover being assumed to exceed the VAT threshold.

Of those participating in the hidden economy, around half (54%) had a total personal income above the income tax threshold. In most cases (56%), their hidden economy income was not their main source of income. Although 12% of participants’ activity was their main source of income, only 1.1% are estimated to generate over £5,000 from their hidden economy activity.

The most popular supplementary (moonlighting) activity was buying things to sell, closely followed by making things to sell. With the continued popularity of online marketplaces such as eBay and Vinted, this is not surprising.

The main reasons research participants gave for not declaring their hidden economy income was that they considered it too small, temporary or irregular, and so did not consider that declaring it was worth the time, or were unaware of the need to do so. Only 47% thought that they should tell HMRC if they were buying and selling on eBay to make money. The majority of research participants considered it acceptable to not declare occasional or small amounts of income and 15% considered it acceptable not to declare amounts up to £10,000.

These outcomes echo those of HMRC’s research on individuals holding cryptoassets (see tinyurl.com/mwr579xx). This affected one in ten of the adult population and, although most of them had holdings of less than £5,000, many of them were unaware of the correct tax treatment.

Cross border reporting rules

Along with 22 other early adopting countries, the UK is implementing the OECD rules for digital platform transparency. On 19 July 2023, the government issued The Platform Operators (Due Diligence and Reporting Requirements) Regulations 2023, setting out rules requiring digital platforms to share data with HMRC.

From 1 January 2024, digital platforms must collect information for HMRC about the income of sellers of goods, accommodation, transport and personal services on their platform. Businesses must identify whether their online operations are within the scope of the rules and, if so, set up reporting systems and familiarise themselves with the penalties for non-compliance before 1 January 2024. The first reports will need to be submitted to HMRC by 31 January 2025. For overseas resident traders, HMRC will exchange the information with the other participating tax authorities for the relevant jurisdictions.

One positive about this measure for taxpayers is that, unlike Common Reporting Standard data, they will receive a copy of the information provided to HMRC. This will provide them with a statement of the amount earned through the platforms, as well as any fees, commissions and taxes paid or withheld by platform operators (albeit on a calendar year basis) to help prepare their tax returns.

Additionally, the OECD has announced that the Common Reporting Standard is being extended to include a Crypto-Asset Reporting Framework (CARF). The CARF provides for automatic exchange of tax relevant-information on crypto-assets – although we await formal confirmation that the UK will adopt it.

What may HMRC do in future to encourage compliance?

HMRC already receives a plethora of information from a variety of public and private sources, including banks, the DVLA and the Land Registry. This data is analysed via HMRC’s Connect system and compared to taxpayers’ tax returns. If discrepancies are identified, HMRC initially issues ‘nudge letters’ to prompt taxpayers to review their tax affairs and rectify any errors or omissions.

Earlier this year, HMRC issued nudge letters to individuals using some online marketplace platforms (including ‘content creators’), encouraging them to either confirm that their tax position is up to date or make a voluntary disclosure of undeclared tax. Further nudges on online trading can be expected when it receives data from the digital platform and cryptoasset initiatives. HMRC can follow up by opening compliance checks too if individuals do not voluntarily bring their tax affairs up to date.

HMRC consulted on streamlining bulk data collection to make it easier for HMRC to obtain and process large data sets from third parties (see tinyurl.com/2b6vy5by). The consultation also considered pre-population of taxpayers returns using data that HMRC holds and who should be responsible for accuracy in such situations.

Cross-border data sharing, including for digital platforms, is on a calendar year so this data may not help pre-population, although HMRC may design in other pop-up prompts for those using its portal to file returns. HMRC also consulted on updating the criteria for individuals to file returns and other changes to encourage more taxpayers to register for self-assessment and file online. Making processes simpler may overcome some of the concerns identified in the hidden economy research and improve compliance rates.

HMRC’s 2018 research indicated that the Publishing Deliberate Defaulters’ regime (Finance Act 2009 s 94) is ineffective at pushing taxpayers to comply, probably due to low awareness of this measure. Instead, taxpayers’ experiences of direct contact with HMRC via compliance checks and the imposition of financial penalties was more effective at encouraging future compliance. Creating or enhancing potential ‘sticks’ to punish non‑compliance via its ongoing Tax Administration Framework review may be a poor substitute for direct contact with the individuals involved in the hidden economy.

HMRC’s successes in using targeted nudge letters illustrate that contacting and educating taxpayers directly is likely to be more effective. Its digital platforms measure will be a good test. Platforms will have to go through a process of checking sellers’ identities before data sharing starts, and then notify them of the data shared with tax authorities: this should make tax obligations obvious to individuals. If this is bolstered by a wide-ranging multi-media campaign by HMRC to encourage people to regularise their historic years’ tax via disclosures and user-friendly information and disclosure options on gov.uk, then we might finally see a step change in the hidden economy tax gap.

Conclusion

Although the tax gap percentage remained the same, the increase in revenue lost to suspected deliberate behaviour and the increasing hidden economy population highlight the size of the task HMRC faces.

Implementation of digital platform data sharing and the CARF should provide more data for HMRC to use, although the Treasury should ensure that HMRC is resourced to use it to close the tax gap.

Advisers should ensure existing clients are aware of these developments just in case some do not realise they should declare their hidden economy or cryptoasset activities. For new clients wanting to file for the first time, it will be essential to understand their financial history and make disclosures to regularise any historic tax liabilities, taking into account discovery assessment time limits and penalty rules.