High Income Child Benefit Charge: the traps and opportunities

Share this article

We examine how the high income child benefit charge can operate unexpectedly if your client has a change of circumstances.

Key Points

What is the issue?

The high income child benefit charge calculation always considers annual adjusted net income – but child benefit entitlement and the taxpayer’s relationship status are considered weekly.

What does it mean for me?

The mismatch can mean the charge might operate unexpectedly if a taxpayer has a change of circumstances.

What can I take away?

If there is a change of circumstances, note that claiming child benefit and opting out of payment provides more flexibility than not claiming child benefit at all.

Broadly speaking, the high income child benefit charge applies where a taxpayer has adjusted net income of over £50,000 and either they or their partner claims child benefit.

Most advisers will be familiar with this basic premise, but if only life were so static. Incomes may rise and fall, relationships may begin and end, and child benefit payments may stop and start, or be backdated.

It can also be in a taxpayer’s interests to opt out of receiving payments while still ‘claiming’ child benefit – a complexity in the system which, not surprisingly, HMRC has had an uphill struggle to communicate to the general public.

So where are the edges of the high income child benefit charge’s scope? In this article, we answer this by looking at the key features of the rules. Then we apply these rules to some situations where there is a change in circumstances. Through these examples, we show that the charge can sometimes apply unexpectedly, or that it may sometimes be beneficial to backdate child benefit payments or continue claiming them.

Who needs to pay it?

The legislation for the high income child benefit charge is in the Income Tax (Earnings and Pensions) Act (ITEPA) 2003 Part 10 Chapter 8 ss 681B to 681H. There are two broad conditions for the charge to apply to a taxpayer in a tax year: we call these the ‘income’ condition and the ‘child benefit’ condition.

The ‘income’ condition

This condition is met if a taxpayer’s adjusted net income for a tax year exceeds £50,000.

This is always an annual test. Adjusted net income means a taxpayer’s total taxable income less gross pension contributions, gross Gift Aid contributions and certain other tax reliefs (Income Tax Act 2007 s 58).

The ‘child benefit’ condition

The charge can be triggered by a child benefit claim, which is made by either the taxpayer, their partner, or in some cases, a third party.

The ‘child benefit’ condition is met where one (or more) of the following is true:

- The taxpayer claims child benefit for at least one week in the tax year (and in that week they do not have a partner who has a higher adjusted net income than them for that year); or

- There is at least one week in the tax year where the taxpayer has a partner who claims child benefit in that week (and that partner does not have a higher adjusted net income than the taxpayer for that year); or

- Someone else claims child benefit for a given week in the year on the basis that they are contributing towards the cost of providing for a child which lives with the taxpayer (and neither that person nor their partner are liable for the charge themselves). This ensures that it is not possible for a taxpayer to avoid the charge simply by having their ex-partner claim the child benefit and pay them the money.

The amount of the child benefit used in the calculation of the charge is the total amount of child benefit payments for which this condition is met (we call these the ‘relevant child benefit payments’).

A taxpayer can be affected by the charge if their partner claims child benefit for a child which is not the taxpayer’s (for example, if the partner has a child from a former relationship).

How much is the high income child benefit charge?

The high income child benefit charge calculation is set out in ITEPA 2003 s 681C. It is 1% of the relevant child benefit payments for each £100 of adjusted net income above £50,000. The amount of the high income child benefit charge is therefore 100% of relevant child benefit payments once adjusted net income reaches £60,000 for the year. In practice, the charge only applies when adjusted net income is £50,100 or more because of the rounding in the calculation.

Advisers should be aware of the effect of the high income child benefit charge on their client’s marginal rate of tax in the £50,000 to £60,000 range for adjusted net income. The greater the number of children for whom child benefit is claimed, the greater the impact of the charge on a taxpayer’s marginal rate.

Bringing down adjusted net income in this income range by making pension contributions or Gift Aid donations will reduce exposure to the charge as well as save ‘normal’ income tax. For example, suppose in 2022/23 I am affected by the charge with an adjusted net income of £55,000 and I claim child benefit for two children for the full year (£1,885.00). If I make a £1,000 gross pension contribution, this will cost me only £412 after 40% tax relief (£400) and ‘high income child benefit charge relief’ of £188. If I make the pension contribution via a salary sacrifice arrangement with my employer, the net cost after any NIC saving would be even lower.

Who is my partner?

This is explained in ITEPA 2003 s 681G. In this context, a taxpayer’s ‘partner’ does not need to be a spouse or civil partner, but can also be someone with whom are living as either their spouse or their civil partner.

If the taxpayer is not married or in a civil partnership, and does not physically live with their partner they may be unlikely to be treated as partners for high income child benefit charge purposes. However, as discussed in a previous article in the context of tax credits (‘Put a ring on it?’, November 2021), in some situations where a couple have other very close connections, HMRC may interpret ‘living together’ more broadly and argue that the charge could apply.

If the taxpayer separates from their spouse or civil partner, then one should take the date of separation as the earlier of the date they are separated either:

a) under a court order; or

b) in circumstances likely to be permanent.

Opting out and backdating

If taxpayers are affected by the charge and they need to pay back 100% of the child benefit received, there are a few reasons why it is still beneficial to claim child benefit but to opt out of receiving payment rather than to not claim child benefit at all. These are:

- HMRC will issue the child with a National Insurance number automatically when they turn 16, without the need for the child to apply for one.

- The claimant will receive National Insurance credits, which can be useful if they do not otherwise accrue qualifying years towards their state pension (for example, if they do not work). If they are not required by the claimant, these credits can be transferred to a relative who provides care for the child (in which case they are known as Specified Adult Childcare credits).

- Having a ‘live’ benefit claim means that child benefit payments can be backdated by up to two years, if it transpires this would be beneficial. Otherwise, the claim can only be backdated by three months.

If the high income child benefit charge applies and claimants opt out of receiving payments, then rather than claiming the benefit and paying the charge they can also avoid having to file a Self Assessment tax return if they have no other reason to do so.

Changes in income or relationship status

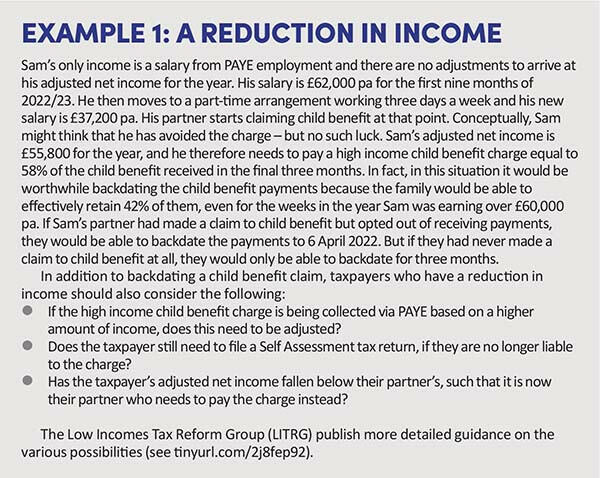

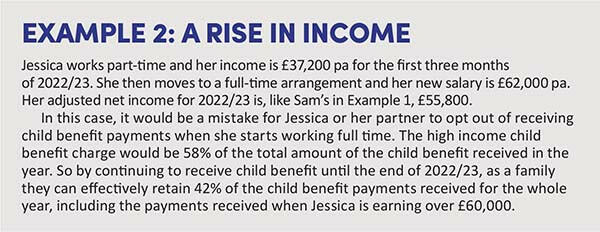

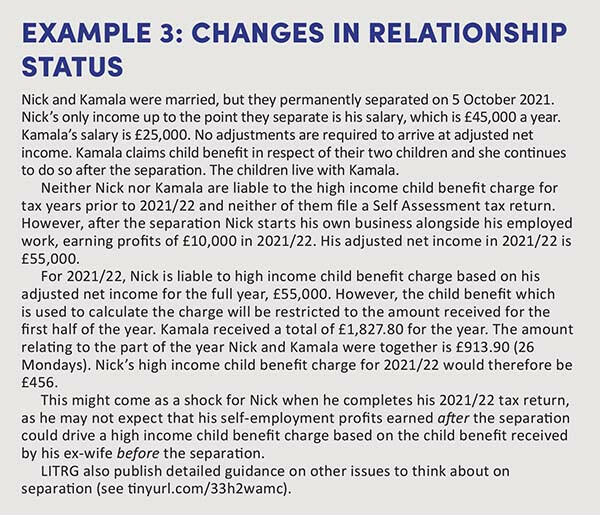

Part of the complexity of the charge comes from the fact that taxpayers need to consider both the year and the week. This can lead to some counterintuitive results (see examples).

Conclusion

The high income child benefit charge is approaching its 10 year anniversary. Despite facing much criticism for the design of the policy, it appears to be with us for the foreseeable future. In addition, the government has resisted repeated calls to raise the £50,000 threshold, which since 6 April 2021 has been overtaken by the higher-rate threshold. Because of fiscal drag, the charge is affecting more taxpayers than ever before. It is therefore increasingly important be aware of the traps and opportunities.