HMRC powers' survey

Share this article

Stephen Barnfield reviews the results of February’s CIOT and ATT members’ survey

Key Points

What is the issue?

The joint CIOT and ATT survey looks at how HMRC applies legislation on penalties, enquiries, information powers and reviews

What does it mean for me?

The survey reports on the views of CIOT and ATT members on HMRC’s application of these everyday tax compliance issues

What can I take away?

Members think some penalties are unfair and disproportionate and their comments highlight some inconsistent legislative application by HMRC

The CIOT and ATT’s survey of members in February 2015 was their first in five years to seek views on on HMRC Powers: Penalties, Compliance Checks and Reviews. The survey asked a number of questions about the operation of the powers in practice and asked for comments.

This survey follows our first into HMRC powers in March 2010 – HM Revenue and Customs Modernising powers, deterrents and safeguards – shortly after the commencement of the new legislation on penalties for incorrect returns, late filing and late payment of tax and HMRC’s information powers.

Summary

Overall, the survey reveals that the system for penalties and compliance checks is not operating as well as we had hoped. Due to the nature of such a survey, it is inevitable that the detailed comments tend to focus on problems rather than positive experiences. In particular, members’ responses and comments highlight inconsistent legislative application by HMRC. Also, some penalties are seen as unfair and disproportionate.

Many answers and comments support the HMRC’s review of penalties now under way, and we have fed the results of the survey into our responses to that consultation.

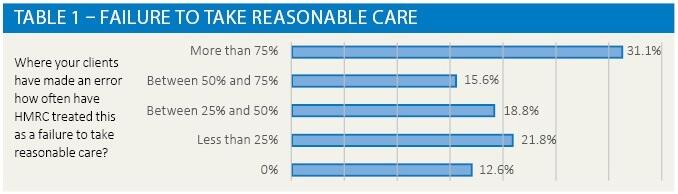

Penalties for incorrect returns: failure to take reasonable care

Many respondents think HMRC are too quick to conclude that there has been a failure to take reasonable care – see Table 1. Indeed, many believe that HMRC’s default position is to charge a penalty regardless of the circumstances. As one respondent said:

‘[The] penalty can seem very high for what clients see as an oversight. HMRC does not seem to accept that mistakes can be made and always argue reasonable care has not been taken. HMRC does not accept that completing a tax return fully and accurately is quite an onerous task for almost anyone who does not have a tax background.’

The range of experience illustrated by Table 1 is so wide that further research is needed. Perhaps some of the divergent experiences are due to differences in the type of work respondents take on, in particular the profile of their clients, since some taxpayers are more likely to make mistakes than others.

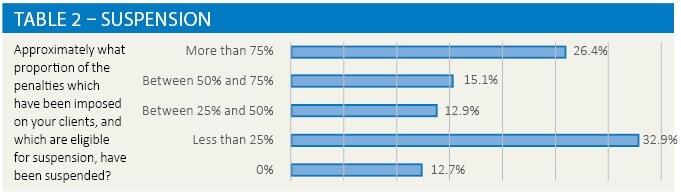

Penalties for incorrect returns: suspension

Fully 72% of respondents believe that clients who have had suspended penalties for incorrect returns have improved their compliance processes as a result – see Table 2. Also, 73% of respondents say that the HMRC decisions they have seen on suspended penalties are, by and large, fair and that the conditions imposed are appropriate. However, some comment that HMRC practice in this area can be inconsistent.

The responses reveal a variety of experiences with suspension of penalties, illustrated by the following comments:

‘HMRC do not apply the penalties consistently – we had two identical cases; both ideal cases for suspension. In one circumstance, HMRC offered a suspension; in the other, HMRC imposed the penalty and would not oblige to suspension.’

‘You have to fight to ridiculous lengths to get a penalty suspended.’

The last comment is supported by some of the survey responses. For example, a small majority of respondents say that suspension was secured in 50%, or less, of cases where it was possible. A similar proportion reports that HMRC have disagreed with them over whether a penalty should be suspended.

Respondents say that, in general, suspension was suggested by the taxpayer or agent instead of HMRC. When the guidance on suspension was first drafted the CIOT expressed concern that it was difficult to see who would be eligible for suspended penalties. Competent tax advisers will know to ask about suspended penalties, but unrepresented taxpayers may not. It would appear that HMRC could do more to raise awareness of the suspension process and to ensure its consistent application.

Late filing and late payment penalties

Some respondents thought it was unfair that normally-compliant taxpayers are penalised for making one-off mistakes and are not treated any differently from those who repeatedly file or pay late.

‘I have a client who is about to be surcharged £250 for late payment of £5,000 2013/14 tax, and is upset about it. This is a very willingly compliant taxpayer, who only missed paying the tax by accident (who happened to be using her professional medical expertise, gratis, in a Delhi slum during half of February).’

Several respondents noted that they often encountered penalties issued in error by HMRC. One particular problem is that penalties for late corporation tax returns are often incorrectly imposed in respect of periods of account in excess of 12 months.

Penalties for late self-assessment income tax returns

Many respondents observed that the automatic late filing penalties for missing the self-assessment tax return filing deadline is disproportionate if there is no outstanding tax liability. Before 2012, this penalty was cancelled if no tax was owed. HMRC’s published statistics show that, since this change, on-time filing has improved. However, it penalises taxpayers if no tax is at risk.

Alternatively, some respondents felt that the late filing penalty is not a strong enough incentive for some taxpayers to file on time.

Compliance checks

In the past, HMRC’s approach to enquiries caused them to be excessively long, so there was strong support for a change in direction.

This survey showed that 45% of respondents reported an increase in informal HMRC requests for information outside a formal enquiry. Not all respondents preferred HMRC’s use of informal checks, as indicated by the following comment:

‘I wish HMRC would stop asking for information on an informal basis whilst implying that not providing that information on an informal basis is not cooperative behaviour.’

Many comments concerned the relevance of the questions being asked and the information being sought.

‘Increasingly finding one has to send all that is asked for in by the date stated, but when able to speak to someone more senior a different approach is seen and more reasonable demands agreed. I very much dislike the letters which are clearly standard ones, covering all possible scenarios and requiring a lot of work which may well not be warranted.’

That is one of several comments suggesting that many questions are not well directed. A few concerns were also raised about the attitude of some HMRC staff when conducting enquires.

Most respondents told us that, when they had been involved in a compliance check HMRC had explained the rules clearly, had applied them appropriately and had acted reasonably.

Discovery assessments

Responses to the survey accord with feedback received from members that use of this provision is not as exceptional as it once was. Some 37% had experience of discovery assessments and, of those who had challenged them, 48% were successful.

As with our 2010 survey into HMRC powers, the CIOT and ATT are concerned that the law on discovery is unbalanced. The 2015 study reiterates the previous recommendation that this area needs to be reviewed.

HMRC’s internal statutory review process and alternative dispute resolution (ADR)

Respondents had contrasting experiences of these two. Roughly half of the members who had used internal review found the process fair and reasonable.

Comments were mainly negative. For example:

‘I have never experienced or heard of any [cases] where an internal review process changed the original decision. It is therefore seen by most clients as irrelevant and merely delaying any tribunal procedure.’

On the other hand, out of the respondents who had experience of ADR, 72% found it fair and reasonable. Many positive comments were made about

the process:

‘The facilitators, in my experience, are well trained, knowledgeable and scrupulously fair.’

‘ADR was excellent, impartial and fair. Reviewer went to some length to distance himself from the caseworker and came across as unbiased.’

Further information

Read the survey results in full here.