Homes under the tax hammer

Share this article

Kevin Ashman and Tom Eyre-Brook explain the onerous reporting obligations of the non-resident capital gains tax charge

Key Points

What is the issue?

The NRCGT charge will have the biggest impact on small, non-UK resident property rental and property investment businesses and non-UK resident individuals (to whom the principal private residence relief is not available). It should have minimal impact on property developers and property traders

What does it mean to me?

The regime involves onerous reporting obligations. In particular, a return is required regardless of whether tax is payable and even when the disposal is made by a person exempt from the charge

What can I take away?

In its simplest form, the NRCGT charge arises only on gains since 5 April 2015. However, if it proves to be advantageous, a taxpayer can elect between three calculation methods

Capital gains tax (CGT) has been extended to cover disposals of UK residential property made by some non-UK residents. Although the annual tax on enveloped dwellings (ATED) and its related CGT charge (the ATED-related CGT) came into force in April 2013, the introduction of the non-resident capital gains tax charge (NRCGT), which came into force on 6 April this year still marks a significant turning point in the tax treatment of non-UK residents.

This is because, unlike the ATED, the NRCGT has not been designed simply to counter a known tax avoidance strategy (the avoidance of paying stamp duty land tax). Rather, its stated objective is to ensure that the tax treatment of non-UK residents (who invest in UK residential property) is comparable to that of UK residents.

The government’s view is that most non-residents disposing of UK residential properties will already be subject to tax on gains in their country of residence and, in those cases, the NRCGT merely alters the balance of taxing rights in the UK’s favour. If a non-resident is liable for tax, both in the UK and in their home country and there is a double tax treaty between them, relief should be available. Typically, the agreement will provide that gains derived from the disposal of immovable property in one state should be taxed only in that state.

Which disposals are within scope?

The NRCGT charge applies to all disposals of UK residential property interests (UKRPI) including reversions in long leases.

A property is a UKRPI if:

- the relevant land has, at any time since 6 April 2015, consisted of, or included, a dwelling; or

- the interest in land subsists under rights to acquire a dwelling ‘off plan’ (that is, before it is constructed). For these purposes, ‘dwelling’ has the same established definition as in the context of SDLT.

The NRCGT charge applies to disposals of UKRPIs that are let out as part of a property rental business. Although these properties are excluded from the ATED (and the ATED-related CGT charge), they are deliberately not excluded from the scope of the NRCGT charge.

However, the NRCGT is not relevant to the disposal of any non-residential property. This includes commercial property that cannot be used (and is not being converted for use) as a dwelling and bare land on which no residential construction has started.

The NRCGT charge also does not apply to disposals of UKRPIs in relation to a trade carried on in the UK (as such, proceeds are already chargeable to UK income tax or CGT, if made by a non-resident individual, or UK corporation tax, if made by a non-resident company). Accordingly, the NRCGT is not a relevant consideration for non-UK resident property developers and property traders. Rather, the NRCGT is targeted at investment activities.

It is worth noting that the NRCGT does not apply to indirect disposals UKRPIs (via disposals of shares or units in companies or funds holding UKRPIs). Rather, the NRCGT operates only at the company or fund level. However, the introduction in 2013 of the ATED charge on UK residential property held in corporate structures has made these arrangements less desirable as a means of holding UK residential property.

Who is within scope?

As a general rule, and in line with the government’s stated objectives, the NRCGT charge will not apply to disposals made by institutional investors or any other ‘widely held’ entities. Rather, it is targeted at non-UK resident individuals and other small and private investors.

More specifically, the NRCGT charge can apply to non-UK resident individuals, trustees, companies that are closely-held, and unit trust schemes and open-ended investment companies (OEICs) that, as well as being closely held businesses, fail a genuine diversity of ownership test.

For NRCGT purposes, a company is closely held if, broadly, it is controlled by five or fewer persons. However, a company is excluded from being a closely-held company where it can only be treated as closely-held if the required five or fewer persons include:

- a company that is itself not closely held;

- a qualifying institutional investor; or

- a limited partnership that is a collective investment scheme.

For these purposes, a qualifying institutional investor includes any widely marketed schemes, pension schemes or companies carrying on a life assurance business.

Unit trusts and OEICs will fail the genuine diversity of ownership test and be subject to the NRCGT charge if they are also closely held. The exception is if they actively market themselves widely enough to reach the intended categories of investors and do not place any undue constraints or limitations on them.

The general exemptions from UK CGT also apply to the NRCGT. Accordingly, pension schemes, investment trusts and charities will also be outside its scope.

How much tax is payable?

The basic position is that only gains that relate to the period after 5 April 2015 should be subject to the NRCGT charge at a rate of 18% or 28% for individuals, 20% for companies, and 28% for trustees and personal representatives.

However, a taxpayer can choose, by entering into an election, to calculate any tax payable by one of three methods.

A taxpayer who decides to make an election in relation to a particular UKRPI will find it irrevocable. However, if disposing of more than one UKRPI, a taxpayer can elect for a different method of calculation for each of them.

The default position (where no election is made)

If no election is made, the NRCGT gain is calculated as if the taxpayer had acquired the UKRPI on 5 April 2015 for consideration equal to its open market value at that date. Accordingly, only gains in excess of that market value will be NRCGT gains.

Accordingly, a valuation as at 5 April 2015 will be required to calculate the gains. Although there is no requirement to obtain a valuation until the property is sold, it may be sensible to obtain one close to that date, even if a disposal is not envisaged in the immediate future. On this point, HMRC have stated that it is the taxpayer’s responsibility to accurately value the property.

Straight-line apportionment election

A taxpayer can elect to time-apportion the total gain over its period of ownership of the property. If so, the NRCGT gain is calculated as the fraction of the total gain of the post-5 April 2015 days of ownership divided by the total number of days of ownership.

A taxpayer cannot make this election if the property in question also falls within the scope of the ATED-related CGT.

Retrospective basis election

A taxpayer can elect to treat the total gain accruing over its period of ownership of the property, whether this is pre- or post-April 2015, as a NRCGT gain. This can be made regardless of whether the property also falls within the scope of the ATED-related CGT.

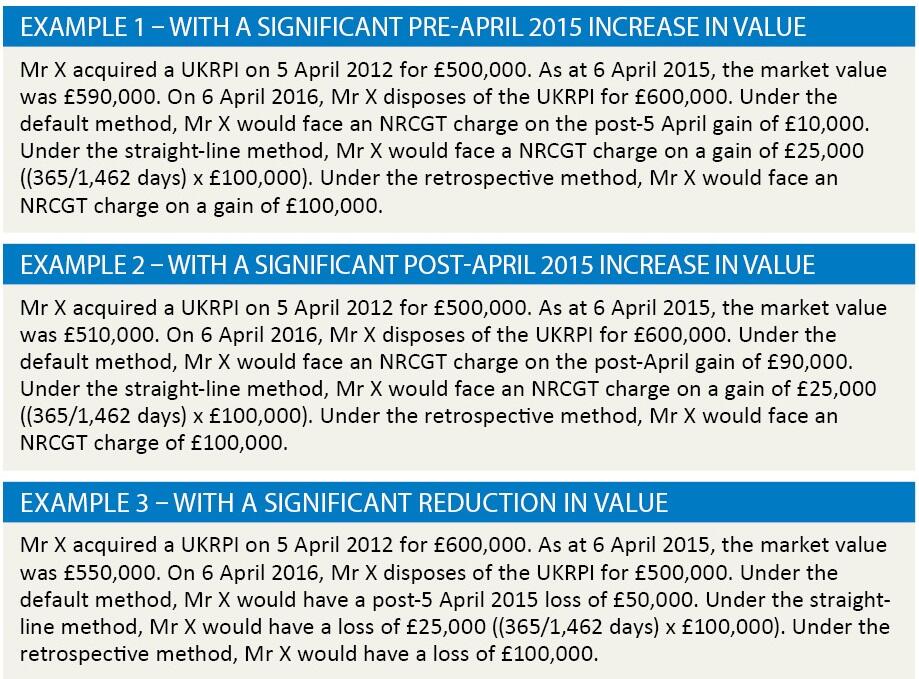

Clearly the most advantageous calculation method will depend on the circumstances of each disposal. A straight-line apportionment election may be useful if there has been a significant increase in the value since 5 April 2015 and a retrospective basis election may be useful if there has been a significant reduction in the value of the property since it was acquired as illustrated in Examples 1– 3.

It is important to note that the ATED-related CGT (with a higher rate of 28%) takes precedence over the NRCGT charge, with only the balance of any post-5 April gains being subject to the latter. This is the case irrespective of where the corporate structure is resident.

Onerous reporting obligations

As a general rule, any non-UK resident who makes a disposal of a UKRPI will be required to deliver what is known as an ‘NRCGT return’ to HMRC within 30 days of completion of the disposal (that is the date when title is conveyed) containing the specific information prescribed by HMRC.

Unless the non-UK resident has been given notice to file a self-assessment return, a corporate tax return or has delivered an ATED return for the property in the preceding year, the NRCGT return will need to include an assessment of any tax due. This will need to be paid within the 30-day period. Otherwise, assessment and payment of the relevant tax will be required by the normal due date for the tax year in which the disposal is made.

The NRCGT return is required to be filed whether a gain or a loss has been made and regardless of whether any tax is due. Any applicable exemption must be claimed in the return.

In particular, the NRCGT return is required to be filed even if the disposal is made by a non-UK resident that is outside the scope of the charge. For example, a non-UK resident company owned 100% by a pension scheme will still be required to file an NRCGT return on which it will claim exemption, even though the nature of its ownership means that it will always be exempt. However, it should be noted that if, on completion of the disposal of the UKRPI, it is uncertain, and not reasonable to expect, that the disposal will be a NRCGT disposal (because it is uncertain, and not reasonable to expect, that the person making the disposal will be non-UK resident for the tax year or part tax year in question) then the NRCGT return must be submitted within 30 days of the day on which it becomes certain that the disposal is a NRCGT disposal.