How do tax thresholds impact our financial behaviour?

Share this article

Tax thresholds play a significant part in our financial system. But how do they impact our behaviour and what would happen if we increase them?

One of the traditional means of apparently simplifying the tax system has always been to lift thresholds. The personal allowance is perhaps the best example of this, as it has virtually doubled since 2010/11. The result has been that several hundred thousand people no longer pay income tax, since incomes generally have grown by less than the growth in the personal allowance.

However, whatever its broader merits, this expensive policy hasn’t proved to be the solution to simplifying income tax. Firstly, until the current year, the national insurance equivalent (which confusingly has two names) was thousands of pounds apart – so individuals remained part of the tax system. Secondly, those receiving benefits found that 63% of the personal allowance increase was clawed back (the clawback rate is 55% from 1 December 2021). Individuals may be better off – but their tax and benefits have not been simplified.

The VAT registration threshold

The VAT registration threshold was the subject of an Office of Tax Simplification review (see bit.ly/3OA2pOF), which reported in November 2017, shortly before that year’s Budget. The UK has the highest registration threshold in Europe and in the OECD, which naturally reduces the number of VAT registered businesses.

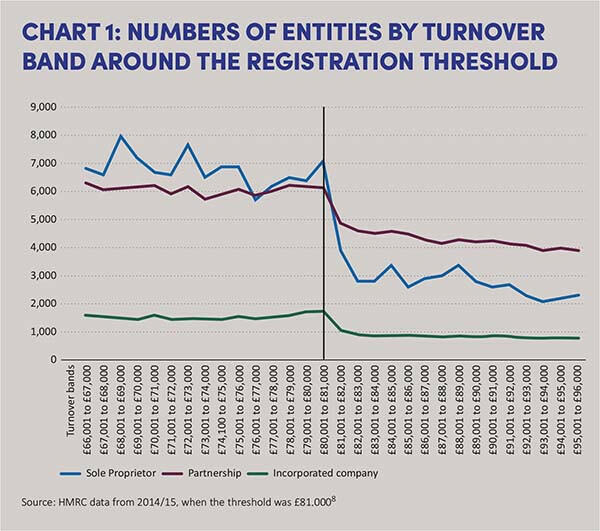

However, the high threshold creates distortions. Chart 1 shows significant bunching just below the threshold, as businesses (especially individuals) are well aware that increasing turnover could reduce profit. Businesses not registered for VAT bear some VAT costs on their purchases, no doubt reflected in the prices they charge. The big difference, though, is that VAT is not charged on what is effectively the owner’s labour. Consumer facing businesses would face a pricing challenge should they grow, meaning that the best policy would be to aim for significant growth to help avoid lower profits.

The 2017 report estimated that freezing the VAT threshold – which turned out to be the policy adopted by the government – would affect about 4,000 businesses annually and bring in about £10 million extra revenue. We are all very well aware of inflation today, though, and a continued freeze will mean that many more businesses will need to adopt a strategy to manage potential or actual VAT.

Changing the threshold?

The OTS also posed the question in 2017 whether there could be a significant reduction in the overall VAT threshold. It estimated that halving the threshold to £43,000 would impact between 400,000 and 600,000 businesses, raising between £1 billion and £1.5 billion a year. This would be significant, with a likely large drop in profits for these businesses and no straightforward way to help. The OTS also noted there would be ‘impacts on economic growth and productivity, on pricing, and the impact of VAT on those in different income brackets.’

However, the high threshold continues to build in a price advantage for small businesses, which are able to undercut larger businesses. Following the Supreme Court’s decision in Uber v Aslam [2021] UKSC 5 and the Administrative Court’s decision on the implications for private hire licensing (see bit.ly/3NdpHc8), it became clear that operators of private hire businesses would need to charge VAT on fares, since they could not act as agents for individual drivers (who themselves did not need to charge VAT, as their sales were below the VAT threshold). The result is that parts of the taxi market charge VAT, whilst other parts do not. This is surely not a sensible policy; perhaps the UK might consider adopting the Australian policy of requiring that all taxi drivers must register and charge GST to avoid this market distortion and resulting complexity (see bit.ly/39HNzHe).

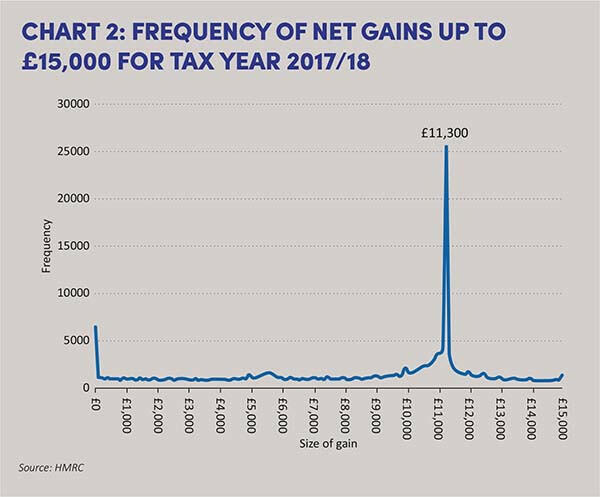

My final example of thresholds comes from capital gains tax (see Chart 2).

This chart from the OTS report (bit.ly/39KRTFz) shows that 25,000 individuals every year manage to sell assets with gains just below the annual exempt amount threshold. This spike looks like deliberate management of share/collective investment portfolios to ‘rebase’ every year, so as to use the annual exemption without turning the portfolio into cash.

Naturally there will also be some in this category who are spreading a sale over several years or sharing with a spouse. However, the chart does show how sensitive many of us are to thresholds – and we do our best to make use of them, rather than simply accepting them as a simplification. The question for governments is whether a lower threshold might still preserve some administrative simplicity whilst offering fewer (perhaps unintended) tax breaks.