How to use P11Ds: reporting obligations for benefits

Share this article

An overview of the income tax, National Insurance and reporting obligations arising for benefits provided to employees, and what should be reported on an employee’s Form P11D.

Often considered to be a simple process, employee benefits reporting can be complex. This is increasingly so with the advent of the statutory payrolling benefits regime, the introduction of the optional remuneration arrangement rules and changes to what benefits can be treated as exempt (such that no employer reporting obligation arises). Complexity can arise from both legislation and HMRC’s approach to the application of exemptions (particularly in respect of the trivial benefits exemption).

The first part of this article looks to give an overview of the various benefits reporting regimes, and when each can or should be utilised. The second part, to be published in the May issue of Tax Adviser, will set out some of the items that we would expect to commonly be exempt, such that tax, National Insurance or reporting obligations do not arise for employers, as well as covering PAYE Settlement Agreements and payrolling benefits under HMRC's statutory regime.

Tax

As a general rule, any expenses and non-cash benefits provided to employees (including a member of their family or household) should be reported on an employee’s Form P11D for tax purposes unless they are:

- exempt;

- included in a PAYE Settlement Agreement;

- payrolled under HMRC’s statutory regime; or

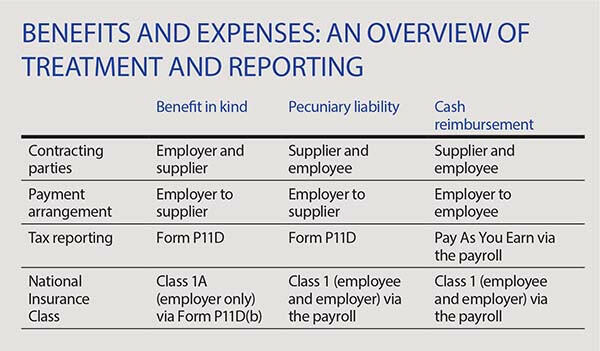

- taxable cash reimbursements (in which case the amounts must be processed via the payroll, see Box: Benefits and expenses: an overview of treatment and reporting.

Subject to the above, a Form P11D is required for each employee to whom benefits and/or expenses are provided. The Form P11D is broken down into 14 sections (sections A to N) for returning different types of benefits and expenses; e.g. private medical and dental treatment or insurance should be reported in P11D box I. Once the Form P11D has been submitted, HMRC will charge the employee income tax on these benefits at their marginal rate, typically via an adjustment to their tax code in the following tax year.

National Insurance

Most benefits attract a Class 1A (employer only) National Insurance (NI) liability. Any benefits subject to Class 1A must be included on Form P11D(b), which is used to report the Class 1A liability to HMRC. Only one Form P11D(b) is required per PAYE reference to summarise the Class 1A NI payable by the employer.

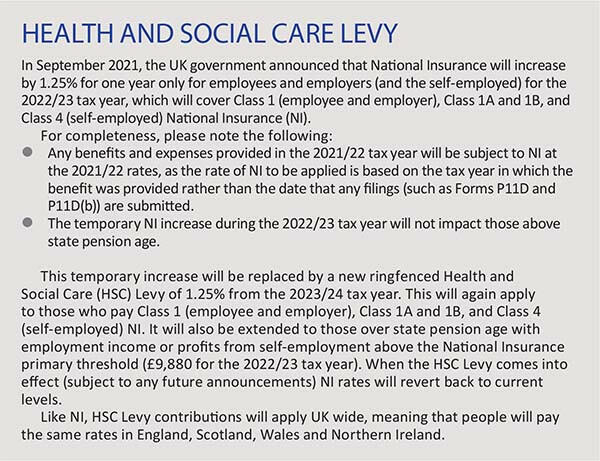

For the 2021/22 tax year, the value of any benefits reported on Form P11D(b) for Class 1A purposes will be subject to Class 1A at 13.8%. This will not be impacted by the forthcoming Health and Social Care Levy (see Box: Health and Social Care Levy).

It should be noted that the income tax and NI treatment does not always align and some items reportable on Form P11D should be subject to Class 1 (employee and employer) NI via the payroll. Whether an item should be subject to Class 1A or Class 1 NI is indicated on the Form P11D itself: items attracting Class 1A are in brown boxes with ‘1A’ on the right hand side, whilst items not subject to Class 1A are indicated by blue boxes. Some common items subject to Class 1 NI include:

- where an employer settles an employee’s personal liability (referred to as a pecuniary liability); e.g. the employee has the contract with the supplier but the employer makes payment directly to the supplier. The specified items should be reported in P11D box N, with any other items to be reported in P11D box B;

- non-cash gift vouchers (P11D box C); and

- mileage allowance payments in excess of the exempt amounts (P11D box E). Note that the exempt amount differs for tax and NI purposes.

Care should be taken to ensure that anything reported as an ‘other’ item (P11D box M) is included in the correct box for NI purposes, as this can include items subject to either Class 1A or Class 1 NI.

The above should strictly have been processed via the payroll in the pay period in which the benefit was provided or the expense was reimbursed for Class 1 (employee and employer) NI purposes.

Image

Value of benefit

The value of the benefit to be charged to tax is referred to as the ‘cash equivalent’. As a general rule, the cash equivalent is:

- the expense incurred by the person who provided the benefit; less

- any amount made good by the director or employee to the person providing it.

If VAT was incurred by the person providing the benefit, the cash equivalent is the VAT inclusive cost (even if the VAT can be reclaimed).

Exceptions to the general rule

Special rules apply in relation to calculating the cash equivalent of certain benefits (see Tax guide 480 in ‘Useful links’ below), including:

- living accommodation (P11D box D);

- employment related loans (P11D box H);

- company cars or vans, and fuel (P11D boxes F and G respectively);

- use and/or transfer of employer owned assets (P11D boxes L and A respectively);

- in-house benefits (for which the marginal cost to the employer is considered) (P11D box K for in-house services); and

- optional remuneration arrangements (see below).

HMRC provides working sheets (see ‘Useful links’ below) to aid with calculating the cash equivalent of some of the more complex benefits, including some of the above.

Optional remuneration arrangements

Changes restricting the income tax and NI advantages in relation to benefits provided as part of an optional remuneration arrangement (OpRA) were introduced with effect from 6 April 2017. These apply to benefits provided under a salary sacrifice arrangement (Type A) or any other arrangement whereby cash can be exchanged for a benefit (Type B).

Subject to some specific exclusions, the value of the benefit to be reported is the higher of:

- the cash equivalent calculated under the ordinary rules (as outlined above); and

- the value of the salary sacrifice or cash given up (referred to as the ‘amount foregone’).

Excluded benefits from the OpRA rules include (but are not limited to) payments by employers into registered pension schemes, employer provided pensions advice, childcare vouchers, workplace nurseries, cycle to work schemes and company cars with CO2 emissions of 75g/km or less (ULEVs).

Where a benefit would otherwise be exempt from tax but for the OpRA rules, HMRC considers that the ‘cost’ of the benefit is nil so that the value of the benefit is the cash foregone by the employee (i.e. where a salary sacrifice arrangement is in place, the value of the sacrifice).

To address concerns about the impact of the OpRA rules on employees who were potentially locked into salary sacrifice arrangements, the legislation included grandfathering provisions such that salary sacrifice arrangements entered into before 6 April 2017 in respect of company cars, accommodation and school fees would not be included in the OpRA regime until the earlier of the arrangement coming to an end, being varied or renewed and 6 April 2021.

Given that all grandfathering fell away with effect from 6 April 2021, particular care should be taken when considering the value of any car, accommodation and school fees which were previously grandfathered. The OpRA rules will need to be considered for all relevant benefits for the 2021/22 tax year.

Useful links

- How to complete Forms P11D and P11D(b): bit.ly/3sEOUFc

- PAYE draft forms: P11D and P11D Working Sheets (2021 to 2022): bit.ly/3vByAXR

- Class 1A NICs on benefits in kind (CWG5): bit.ly/3hAWvyh

- Expenses and benefits for directors and employees: Tax guide 480: bit.ly/3MwsLkz

Key benefits reporting deadlines for the 2021/22 tax year

5 April 2022: Last day to register for payrolling benefits in kind in 2022/23

31 May 2022: If not already included on the payslip, provide a statement to employees providing specified information for payrolled benefits

4 July 2022: Make good any unrecovered PAYE on notional payments to avoid a section 222 charge

5 July 2022: Agree a new PSA or amend an existing PSA with HMRC for the 2021/22 and subsequent tax years

6 July 2022: General deadline for making good any non-payrolled benefits in kind provided by the employer to avoid P11D benefit reporting

6 July 2022: Forms P11D and Form P11D(b) filing deadline

22 July 2022: Due date of payment Class 1A NI liability on employee non-cash benefits as set out in the Form P11D(b). Due date is 19 July 2022 if not paid electronically

No statutory deadline: (Usually 31 July or 31 August 2022 per individual agreement with HMRC) Submit calculations to notify HMRC of the PSA liability due

22 October 2022: Due date for payment of PSA liabilities (income tax and Class 1B NI)