Hybrid mismatch

Share this article

Ed Wright provides analysis on the UK implementation of Action 2 of the OECD BEPS project

Key Points

What is the issue?

The UK will introduce new anti-hybrid rules effective from January next year, which will represent a fundamental change to the taxation of multinationals operating in the UK.

What does it mean to me?

Multinationals and their advisers will need to undertake a systematic diagnosis exercise for existing arrangements to work out whether and how they are impacted, and what action to take.

What can I take away?

The UK is an early mover in responding to BEPS Action 2, but a number of other territories will surely follow suit in the near future meaning that there will continue to be changes in the treatment of transactions and arrangements that involve cross-border aspects.

The UK will introduce new ‘hybrid mismatch’ rules from 1 January 2017 in response to Action 2 of the OECD Base Erosion and Profit Shifting (BEPS) project. The rules will be broader in application than the current ‘tax arbitrage’ provisions and many multinational groups will be affected. The impact on the UK tax profile will often depend on the nature of arrangements and transactions outside the UK, and a significant diagnosis exercise will be needed.

The new rules: overall approach

The proposed new law is found in F(No.2)B 2016 Sch 10, published in March, and in places differs significantly from December’s initial draft.

The overarching principle is that adjustments will be made to corporation tax liabilities to counteract situations where there would otherwise be a:

- deduction/non-inclusion mismatch; or

- double-deduction mismatch.

A deduction/non-inclusion mismatch arises when a person obtains a tax deduction for a payment without there being a corresponding amount of fully taxable income arising to another person. This may include unreasonably long mismatches in timing between deduction and taxable receipt. A double-deduction mismatch occurs when tax deductions for the same payment are available to two taxpayers, or to the same taxpayer for two different taxes.

When the new rules apply

Sch 10 chs 3–10 describe the circumstances under which such a hybrid mismatch might arise, and the proposed counteraction in each case. Broadly these circumstances involve the presence of one of the following:

- Hybrid instruments: mismatches may be attributable to the terms or features of a financial instrument (for example, if the instrument is treated as debt in one territory and equity in another);

- Hybrid transfer arrangements: mismatches may result from the differing ways that parties to arrangements such as stock loans and repos treat them for tax purposes;

- Hybrid entities: mismatches may be attributable to the hybrid nature of entities (those that are treated as taxable persons under one territory’s tax law, but as tax-transparent entities under another’s);

- Companies with permanent establishments (PEs) outside their state of residence: mismatches may arise from PEs, either because payments to companies with a PE are not fully taxed in either the head office or PE territory, or because the PE territory permits tax deductions for actual or notional payments to the head-office territory that are not correspondingly taxed there; or

- Dual resident companies: mismatches, specifically double deductions for the same expense, may occur if a company is resident in two territories or has a PE outside its territory of residence.

The specific counteraction varies in each case. In general, the rules provide for:

- the UK to impose additional taxable income when a UK corporate taxpayer receives a payment that would otherwise give rise to a mismatch; or

- the UK to deny tax deductions, or limit their use, when a UK corporate taxpayer makes such a payment.

Chapter 11 sets out the concept of ‘imported mismatch’. In short, the UK will restrict or deny corporation tax deductions if a UK corporate taxpayer makes a payment that does not itself give rise to a mismatch, but where there is, within a wider arrangement, a mismatch of the type described above.

In general, the rules are written for arrangements implemented among related parties, but they can also apply to those between unrelated persons when it is reasonable to suppose that these have been designed to give rise to a tax mismatch.

Finally, ch 13 contains an anti-avoidance provision which permits just and reasonable counteraction should a person, as a result of avoidance arrangements, otherwise obtain a tax advantage inconsistent with the principles and policy objectives of the rules or equivalent provisions in other territories. Regard may be given to the OECD’s Action 2 Final Report in assessing this.

Contrast with current law

The new rules anticipate repeal of the tax arbitrage rules in Pt 6 of the Taxation (International and Other Provisions) Act 2010. There is an overlap with that existing legislation, but there are material differences. These include:

- there is no ‘purpose’ based exclusion from the rules. This contrasts with the tax arbitrage rules, under which the so-called ‘Condition C’ test allows relief from them if arrangements do not have a main purpose of achieving a UK tax advantage for the company. The practical effect of this will be that, for taxpayers relying on Condition C, including cases when HMRC has given a Condition C clearance, it is likely that the new rules will have an adverse tax impact in the UK; and

- the tax arbitrage rules are concerned primarily with hybrid entities and hybrid instruments, whereas the new rules are extended to cover mismatches arising from PEs and dual residents too.

Examples of application

The OECD Action 2 Final Report, on which the proposed new rules are largely based, includes 80 examples of potential application, showing the wide ambit of the provisions.

Two illustrations of how the UK rules could apply are set out in the examples but in reality most multinational groups operating in the UK will need to conduct a review to identify any exposures arising from their specific arrangements.

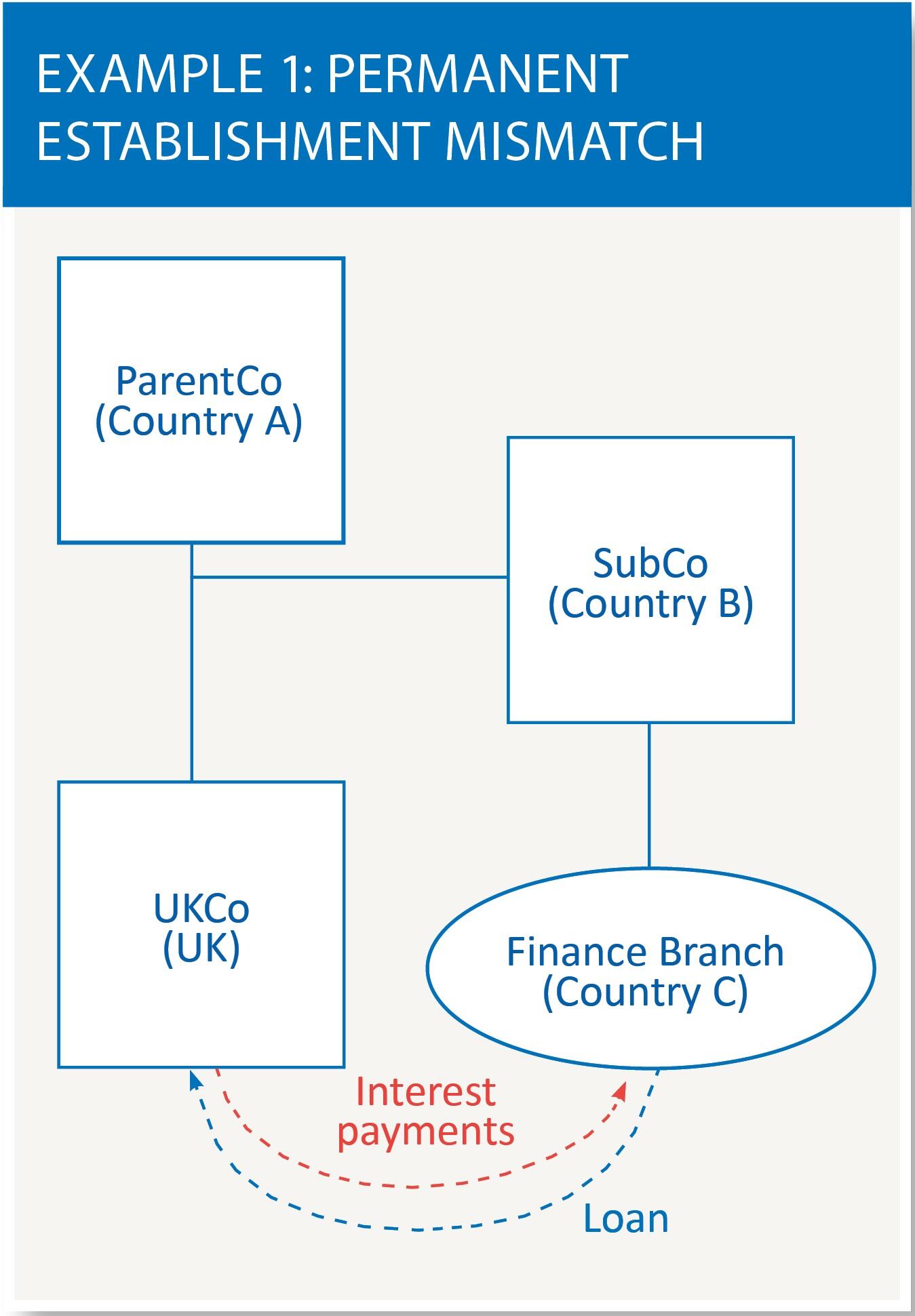

In example 1, a UK resident company (UKCo) makes interest payments to another group company (SubCo) resident outside the UK. SubCo has a finance branch office, which constitutes a PE in Country C. Country B grants an exemption from tax for profits attributable to a foreign PE. Country C’s tax system does not tax income in the finance branch unless it arises from an active operating business, which is not the case here. In effect, the interest income is untaxed.

In this scenario there is a deduction/non-inclusion mismatch arising from the fact that SubCo operates through a PE in Country C. It is likely, therefore, that the new hybrid mismatch rules will deny tax deductions to UKCo.

It is worth noting:

- If the controlled foreign company rules in Country A imposed a tax charge on the interest income, this could reduce or eliminate the mismatch and thus reduce or eliminate the counteraction against UKCo; and

- If Country C did apply corporate income tax at its normal rate to the whole of the interest income, this could again eliminate the mismatch (even if Country C had a very low rate of tax), unless the income was offset by actual or notional payments by the finance branch to SubCo.

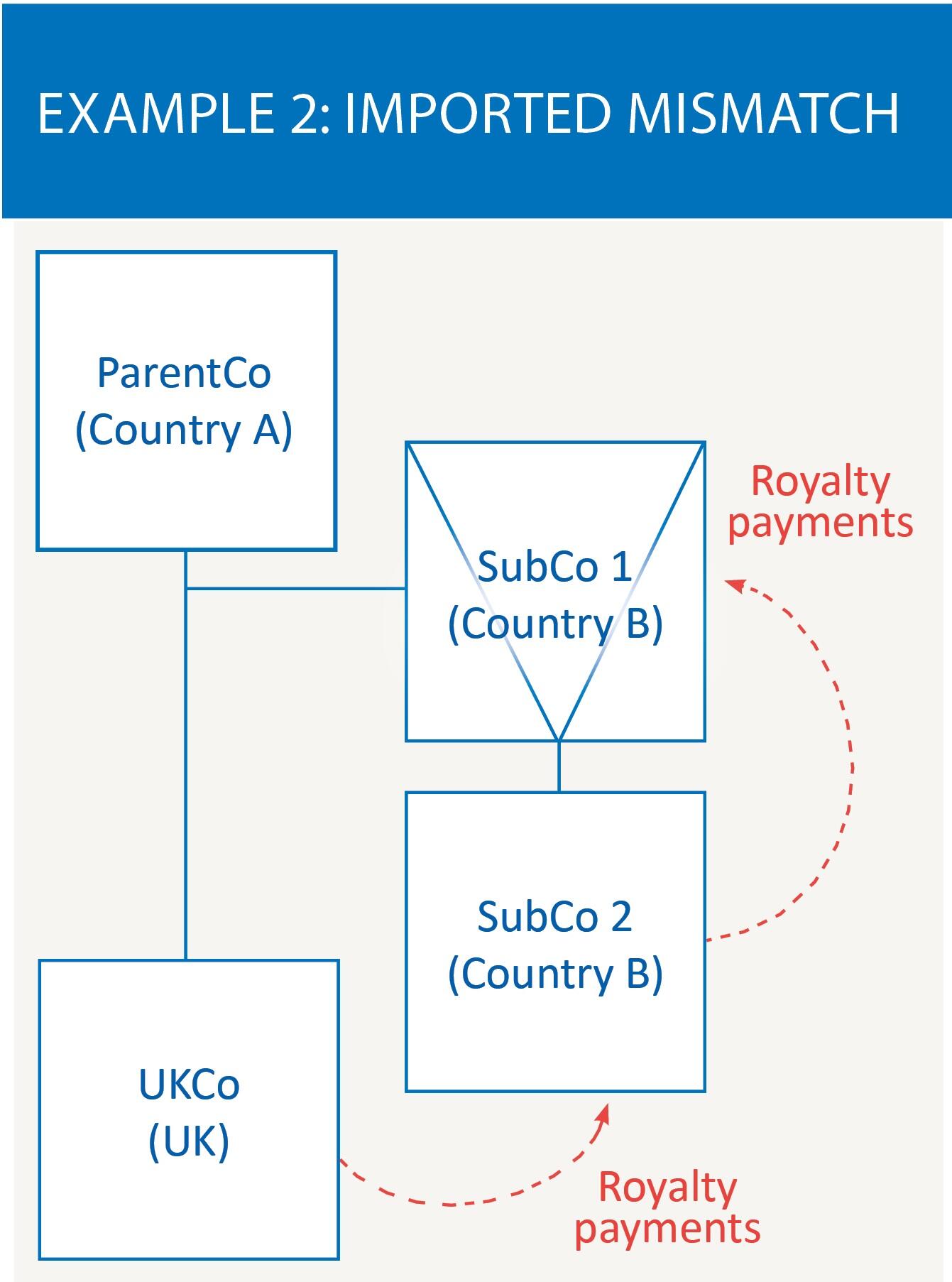

In example 2, a UK resident company (UKCo) makes royalty payments to another group company (SubCo 2) resident in Country B. These are fully taxable in Country B but, as part of a wider arrangement, SubCo 2 in turn makes royalty payments to SubCo 1 which reduce its profits. SubCo 1 is organised under Country B’s laws but seen as tax-transparent there. Country A, on the other hand, considers SubCo 1 as a separate taxable entity (it is thus a hybrid entity). Accordingly, neither Country A nor Country B imposes tax on the royalty income in SubCo 1.

Although the payments from UKCo are fully taxable for the recipient, the wider arrangement includes a hybrid entity mismatch. Under the imported mismatch rule, it is likely that the UK will deny tax deductions for UKCo’s payments to the extent they fund SubCo 2’s onward payments.

Impact and response

Multinationals operating in the UK will need to review their transactional structures – especially any designed to obtain beneficial tax outcomes – with reference to the new rules. Where there is an adverse impact, they will need to determine whether to reorganise to eliminate hybrid elements. It is, however, not an easy time to assess the best course of action for the long term – not least because of other anticipated UK law changes in 2017 on the deductibility of interest and the use of tax losses.

The UK is an early mover in terms of responding to BEPS Action 2. In theory, there may be a finite pot of taxable income that is ‘up for grabs’ on hybrid mismatches between territories. It will be fascinating to see whether and when other countries seek to adopt similar rules, thus protecting their own tax bases and in doing so reduce the extent to which the UK can collect tax through its hybrid mismatch rules. At the time of writing, Australia has announced an intention to introduce anti-hybrid rules in 2018.

There will surely be a behavioural impact as multinational groups make less use of hybrid mismatch arrangements. This could be seen as a victory for the BEPS process, although the financial return will depend on the appetite and ability of multinationals to achieve similar tax outcomes from non-hybrid arrangements. Nothing in BEPS Action 2 counters territories competing simply by offering lower or zero headline corporate tax rates, so attention may move in that direction.