An impressive start

Share this article

Neil Warren gives practical tips about making sure the first VAT return submitted by a business is accurate

Key Points

What is the issue?

The first VAT return submitted by a business often includes a number of technical challenges, such as how much input tax can be claimed on pre-registration expenses and what VAT schemes should be adopted. An understanding of these issues is important in order to submit an accurate return to HMRC.

What does it mean to me?

It can sometimes be a grey area whether an expense comes into the category of goods or services, where different time periods apply for pre-registration expenses. It is also important to be sure that an ‘intending trader’ has a genuine intention to make taxable supplies before input tax is claimed.

What can I take away?

The evolution of Making Tax Digital will hopefully mean that voluntary updates and supplementary data can eventually be submitted online to support the figures in the nine boxes of the return, hopefully speeding up the processing of repayment returns and avoiding an HMRC enquiry.

As a great fan of cricket, it is fair to say that most international players dream of a successful debut when they first play for their country. A good start is important in any activity, including the submission of the first VAT return to HMRC by a newly registered business. In many cases, these returns will be for a repayment, which could attract interest from one of HMRC’s compliance teams.

Intending trader registrations

I know that some advisers are a bit apprehensive getting a VAT number for a client when the first day of trading is a long way off (a voluntary registration). It can be a bit of a worry claiming input tax on expenses connected with the intended business but then entering zeros in both the output tax and outputs boxes. I often get asked whether there is a time limit before supplies must start – the answer being ‘no’ – although the intention to start trading at some point in the future must always be clear.

To share a tale, I used to act for a family in Devon and the partners purchased the freehold of a run-down old pub that was in a total state of disrepair: ‘We can even see the stars through the holes in the roof when we’re in bed,’ the wife proudly told me. They spent 15 months repairing and improving the property before the doors opened for business, which meant five quarters of repayment VAT returns were submitted (all repaid by HMRC) before there was even a sniff of output tax.

The challenge is to be able to provide to HMRC (if requested) a bundle of documents that clearly show an intention to trade and make taxable supplies – business plans, cash flow forecasts, orders with potential customers, supplier details, adverts to recruit staff, rental agreements with landlords etc.

Pre-registration input tax

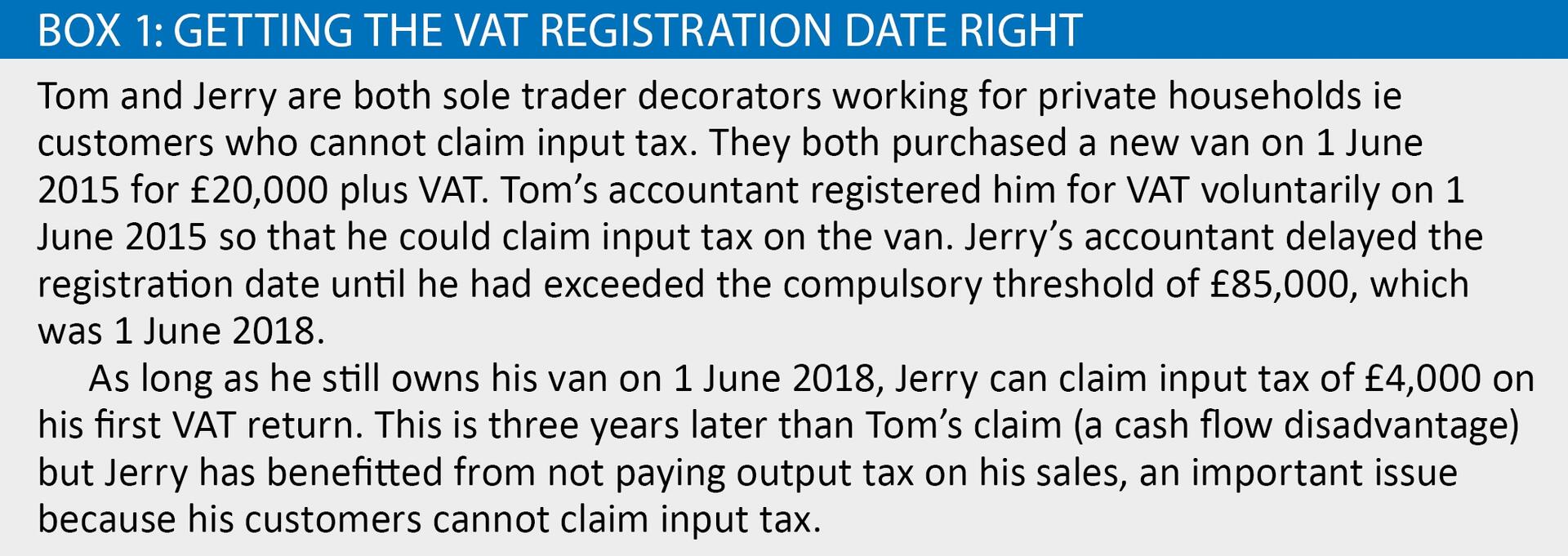

The timing of the VAT registration date is very important. I have seen situations when a business has asked for a VAT number too early (on a voluntary basis) in order to claim input tax on its stock and assets. But the same input tax would still be claimable in most cases if the business delayed its registration date and used the opportunity to claim input tax on pre-registration expenses. See box 1.

The basic rules for claiming pre-registration input tax depend on whether goods or services are involved:

- Goods – which have been purchased within the four-year period before the date of registration, which have been used in the business during that time, and are still owned by the business on its first day of registration. The definition of ‘goods’ includes both stock and fixed assets.

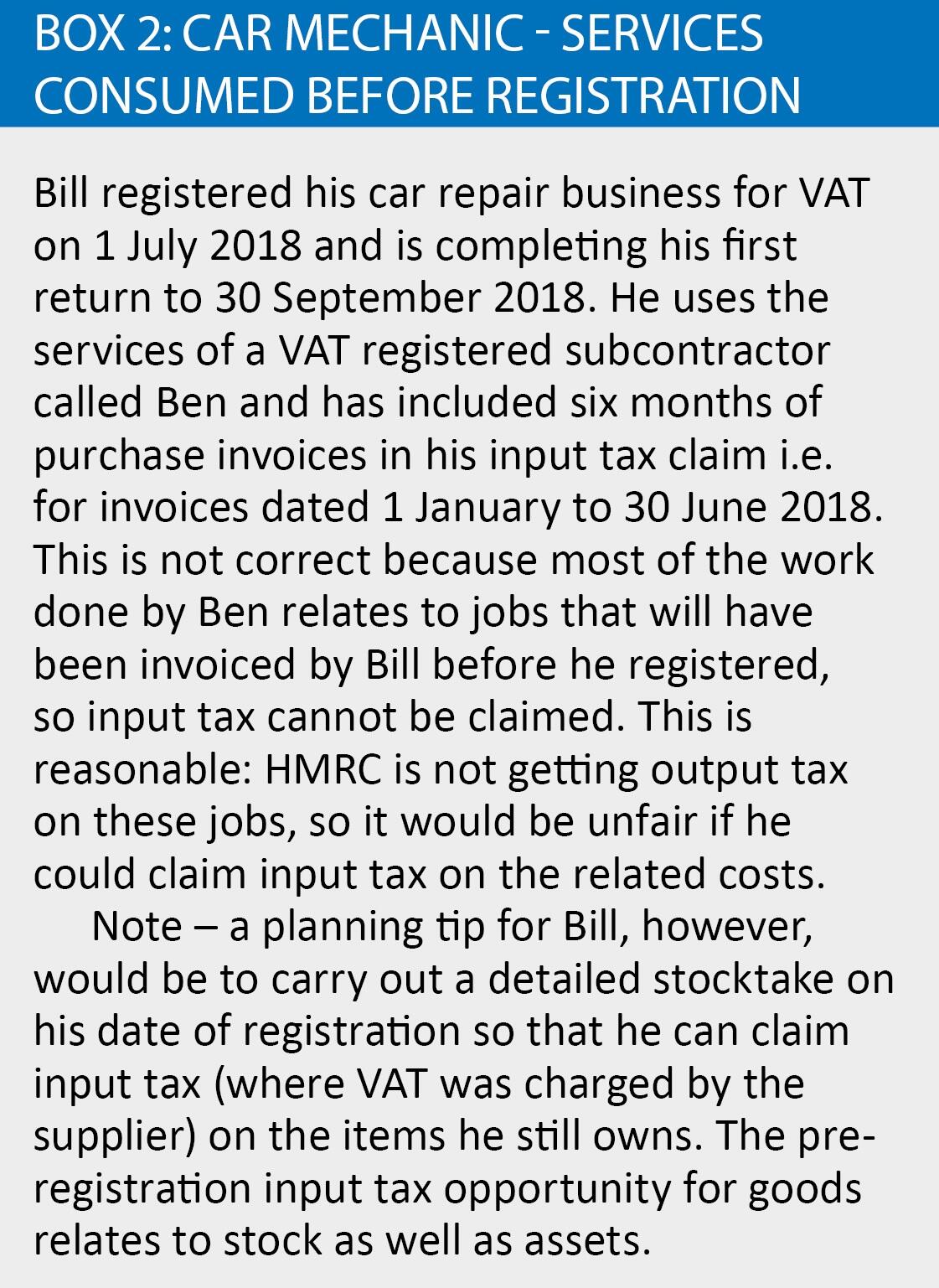

- Services – the time window is capped at six months before registration, and the service cannot relate to a sale that has been invoiced or consumed before registration.

There was a period a couple of years ago when HMRC discretely amended their guidance and stated that an input tax claim on capital goods, such as Jerry’s van, had to adjust for wear and tear i.e. an input tax claim would be based on the market value of the goods at the time of VAT registration and not the original cost price. The good news is that HMRC U-turned on this approach, and we are now back to cost price – definitely good news for Jerry. (see Revenue and Customs Brief 16 (2016) – 4 November 2016).

Goods vs services

The six-month time window for claiming pre-registration input tax on services is much less than for goods, so getting the ‘goods or services’ decision wrong on the first VAT return could attract HMRC interest. Care is also needed on the issue of a service being consumed before registration. See box 2.

A common source of dispute relates to building work and the split between goods and services. Think of a hairdressing salon which became VAT registered in October 2018 but spent a lot of money improving the salon 12 months earlier. The owner might claim that because the expenditure is capitalised to her balance sheet that it relates to capital goods rather than services. But this is not correct. There is no problem with input tax recovery using the four-year window on items such as hairdryers and chairs but definitely an issue with spending on e.g. decorating, electrical and plumbing works, which is capped at six months.

VAT schemes

Some business owners wrongly think that the cash accounting scheme only applies to sales and not purchases. They are happy to delay accounting for output tax until a debtor pays his dues but don’t realise that the payment date also counts for input tax claims. There might be benefits in a newly registered business delaying its entry to the scheme if there is a lot of input tax to claim on creditors in the early days, and not much output tax to declare on debtors.

The flat rate scheme (FRS) is a little bit like a footballer aged over 35 – it has performed well in the past but is now past its best days. This is because of the introduction of the ‘limited cost trader’ category in April 2017, which wiped out many of the tax gains made by scheme users, although it still offers important time-saving benefits. The 16.5% rate for limited cost traders gives minimal credit for input tax, meaning that many users have either left the scheme or deregistered in the case of voluntary registrations. But as a reminder, any business can join if it expects its taxable sales to be less than £150,000 excluding VAT in the next 12 months, and there is a 1% discount on the chosen category for the first 12 months of VAT registration.

Partial exemption?

There are definite benefits in clients asking their adviser to review the first VAT return before the submit button is pressed. It is important to extend this check beyond the basic figures and also review the client’s trading activities. I know that many advisers have overlooked situations where a client has generated exempt income and should therefore restrict input tax claims under partial exemption or, equally importantly, to check if input tax can still be claimed because of the partial exemption de minimis limits (beyond the scope of this article – see VAT Notice 706, section 11). I enjoy recalling the tale of an accountant who told me that one of his clients bought a house to renovate and sell and had managed to persuade HMRC to let him have a VAT number so that he could claim input tax on the building repairs, even though the house sale was obviously exempt from VAT and the client was making no taxable sales!

Making Tax Digital (MTD)

As we all know, MTD for VAT will take effect for most businesses that trade above the £85,000 threshold in April next year but there is one aspect of the process that will eventually give clients the chance to hopefully be ahead of the game if they submit a repayment return which might be queried by HMRC. Section 4 of VAT Notice 700/22 is headed ‘voluntary updates’ and section 5 is titled ‘supplementary data’. Both sections are limited about detail and refer to the future but supplementary date is defined as ‘information that supports the 9 Box VAT return’. As I understand it, the eventual outcome (which is very positive) will be that a business making, say, a large VAT repayment claim on a return will be able to digitally provide supplementary data to HMRC to support the figures e.g. the digital record of purchase invoices that makes up the input tax total but not copies of purchase or sales invoices. But as the old saying goes…don’t quote me on that one!