Increasingly local

Share this article

David Philips explains why a local income tax is worthy of serious consideration

Key Points

What is the issue?

The council tax bills that have been hitting people’s doormats are heavier than ever before. But council tax increases are more than offset by reductions in funding from national government and rising costs and demands for a range of services, most notably adult’s and children’s social care.

What does it mean to me?

We must soon face a looming choice: either we accept further cutbacks in the services councils can provide; or additional funding must be found, whether in the form of grants from national government or by devolving more tax-raising powers to councils themselves.

What can I take away?

Given the demand for greater localism, a local income tax seems at least worthy of serious consideration though. But in this debate it will be important to keep in mind one simple fact: tax devolution per se is not the answer to funding shortfalls – more funding is.

The council tax bills that have been hitting people’s doormats are heavier than ever before. The average Band D tax rate in England is now £1,750 a year, up £266 (18%) over the past four years – with £80 (4.7%) of that increase in the last year alone.

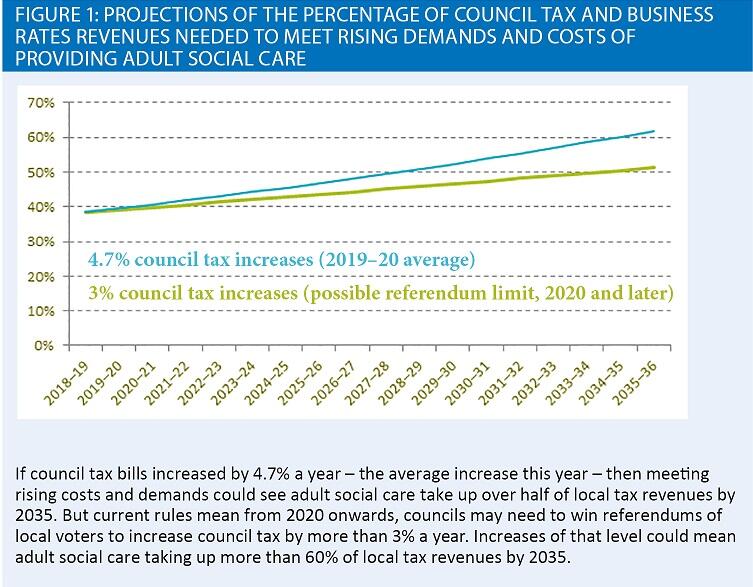

One might therefore expect that councils would be expanding and improving the services they offer. The opposite is in fact often true, as council tax increases are more than offset by reductions in funding from national government and rising costs and demands for a range of services, most notably adult’s and children’s social care. Indeed, projections suggest that even with 4.7% increases in council tax every year (almost doubling Band D rates to £3,485 a year within 15 years), spending on adult social care services could account for half of councils’ tax revenues within 15 years. This would severely squeeze the amount available for other services.

Looking ahead then, we must soon face a looming choice: either we accept further cutbacks in the services councils can provide; or additional funding must be found, whether in the form of grants from national government or by devolving more tax-raising powers to councils themselves.

Councils have been pushing for such powers in the last few years. But much of the focus has been on new taxes with the potential to raise useful sums in only a few places – like tourist accommodation taxes, or levies on workplace parking. London and some other big cities have argued for an option which would entrench particularly bad parts of the tax system that should in fact be abolished – Stamp Duty Land Tax.

In our latest paper, Taking control: which taxes could be devolved to English councils?, my colleagues and I argue instead that if tax devolution is the route we want to take to fill the looming hole in councils’ budgets, a local income tax would be the most sensible option. Why is this?

Taxes are not born equal – nor are they equally suitable for devolution

We use a set of criteria to assess whether different taxes are suitable for devolution to councils, drawing on both economic theory and more practical considerations.

For example, taxes for which it is difficult to identify the location of taxable activity tend not to be good candidates for devolution: the apportionment of tax bases between councils would be very tricky and costly.

Consider corporation tax. Changing business models mean we find it difficult to identify in which country multinational businesses’ profits are generated. Devolution would mean having to pinpoint in which town or city many more purely domestic businesses’ profits are generated, multiplying the difficulties.

How would the profits of a chain of supermarkets be apportioned between its stores, website operations, warehouses, and headquarters, for instance? We could use the approach used internationally, treating transactions between parts of the business located in different council areas as if they were between unrelated companies – but we know this is open to debate in many cases. Alternatively we could use a formula based on location of sales, capital or employment – but this may be more likely to distort real activity. Both approaches would also mean a significant increase in administration and compliance burdens.

A local VAT would be difficult and costly to operate for similar reasons. And both VAT and corporation tax have another feature that makes devolution problematic: mobile tax bases. Both theory and evidence suggest companies can shift around their activities to minimise their tax liabilities, and shoppers can change where they shop to limit how much VAT they pay. This means the location of economic activity could be distorted – taking place where tax rates are lowest, rather than where economic fundamentals are best. Knowing this, councils could have an incentive to engage in competitive tax rate-cutting, undermining revenues for all.

This reminds us that revenues are an important consideration for tax devolution. In particular, taxes where revenue yields are highly unequal and/or volatile are unlikely to be ideal candidates for devolution: it could be very difficult to avoid big divergences in funding for councils, and to protect councils from revenue shocks. Stamp Duty Land Tax’s highly unequal tax bases – revenues per person in Westminster and Kensington and Chelsea were over 75 times higher than in Blackpool, Hartlepool, Sandwell and South Tyneside in 2017–18 – and extreme volatility are two further reasons we doubt its suitability for devolution.

Finally, political accountability is important – those paying taxes set by councils should be able to vote in local elections. If they cannot, there may be excessive upward pressure on local tax rates as politicians and those who can vote enjoy what seems like a free lunch. The fact that many business owners do not live locally, and only a small fraction of properties change hand each year, suggest local corporation, value added or Stamp Duty taxes may suffer from accountability problems.

Income tax has a number of properties making it attractive for partial devolution...

On the other hand, a local income tax would be paid by most local voters (and very few non-voters). If councils benefited from growth in local income tax revenues, they would have incentives to boost the employment and income of residents – both by increasing the number and quality of jobs in the local area and by helping residents access better jobs in neighbouring areas.

Local income taxpayers could be identified based on where they live, and tax bases apportioned straightforwardly – at least in principle. And by restricting powers to a flat rate income tax on all tax bands, concerns about tax rates on the highest income being subject to excessive downwards pressure (due to tax competition) or upwards pressure (due to limited voting power) could be addressed. Indeed, this is the approach used in Scandinavia, where local income taxes are a major source of revenue – in Denmark and Sweden, bigger than the (progressive) national income tax. Each 1% on the tax rate would raise around £6 billion across England.

...but range of practical difficulties would need addressing...

Of course, devolution of income tax powers would not be costless. Employers and pension providers would have to update their software to calculate and deduct different amounts of income tax depending on where people lived. HMRC would need to make similar changes. And rules on how taxes should be calculated and divvied up when people move part way through a tax year need to be designed and implemented.

To do this effectively, employers, pension providers and HMRC would need up to date and accurate information on where taxpayers live. This isn’t always the case at the moment, in part because there is no legal duty for people whose tax is collected by PAYE to inform HMRC of their address. That should probably change.

People with second homes could also try to claim the one in the council area with the lowest tax rate was their main residence even if it were not. This is something which has caused some worry in Scotland as it has increased income tax on high earners, with many of the so-called WILLIEs (Working in London, Living in Edinburgh) maintaining a crash pad in London. Councils and HMRC would have to share information to help tackle this issue.

The partial devolution of income tax to Scotland and Wales has also required dealing with tricky issues related to tax relief for pension contributions to schemes operating on a relief-at-source basis, as well as Gift Aid for charitable giving. More robust fixes might be worth considering if income tax powers were devolved to local government too.

...and unequal tax bases would mean significant redistribution would be needed

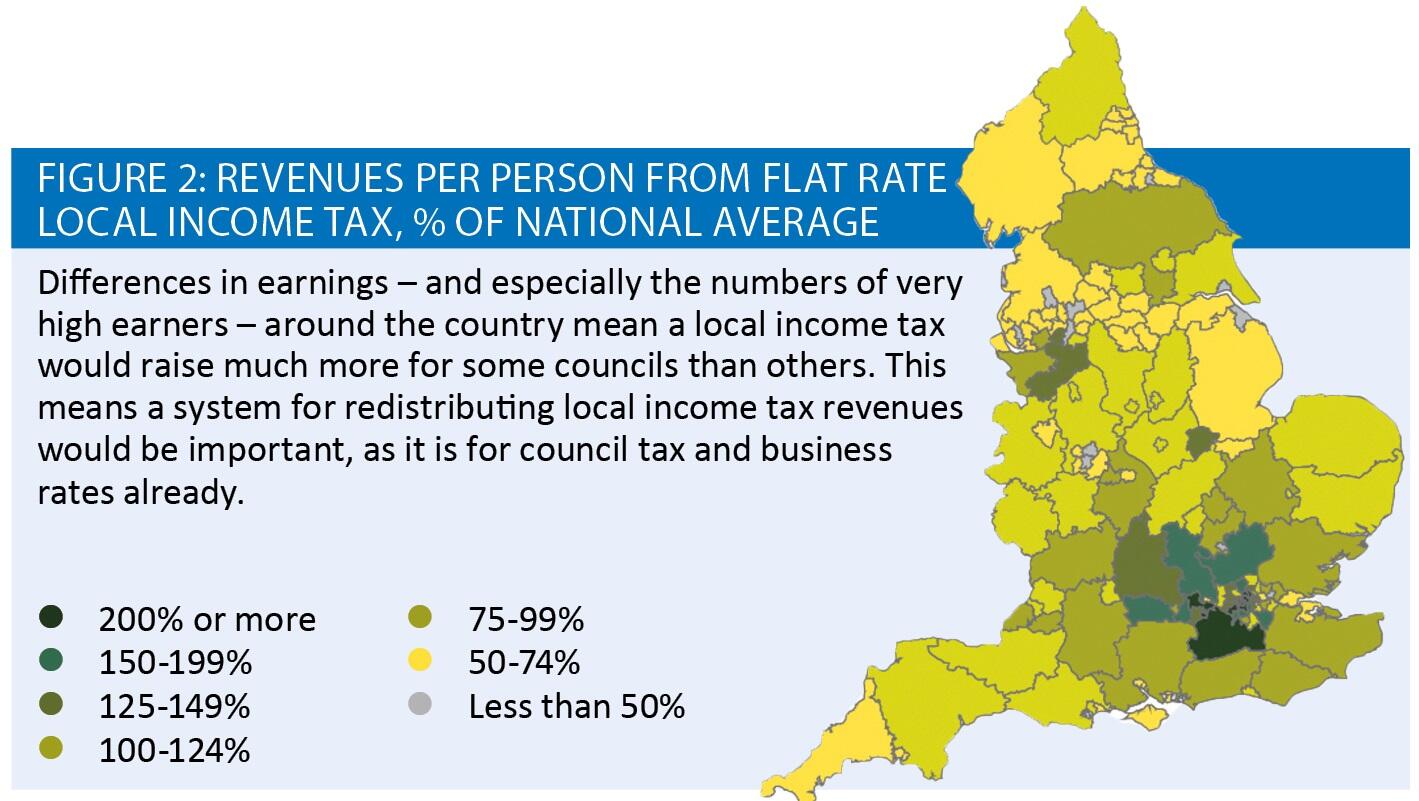

A system to redistribute revenues between richer and poorer council areas would also be needed. This is because local income tax revenues, while less unequally distributed than a tax like Stamp Duty, would still be much higher in some areas than others. For instance, our estimates suggest revenues per person in richer parts of West London and Surrey could be more than twice the national average, while in places like Blackpool, Blackburn, Hull and Sandwell, they are likely to be less than half the average.

Ultimately, it’s a question of the value placed on local incentives and discretion

These practical and distributional considerations mean we stop short of calling for the devolution of local income tax powers. That’s because a political judgement is needed.

How to weigh up the stronger financial incentives for growth and greater local discretion over tax and spending levels that local income tax powers could bring, versus the additional administration and compliance costs, and scope for larger funding divergences between fast- and slow-growing parts of the country.

Given the demand for greater localism, a local income tax seems at least worthy of serious consideration though. But in this debate it will be important to keep in mind one simple fact: tax devolution per se is not the answer to funding shortfalls – more funding is. If we want to maintain or improve the services councils can provide, taxes will need to rise, whether at a local or national level.

Editor’s note: The Scottish Commission on Local Tax Reform examined the issues of a local income tax in Scotland. The Scottish Government has decided not to proceed with a local income tax.