An intangible problem

Share this article

Jitendra Patel considers the complexities of the intangible fixed assets regime and tries to untangle the tax consequences of transactions involving IFAs and partnerships

Key Points

What is the issue?

This article focuses on the anomalous outcomes arising from transactions involving intangible fixed assets (IFAs) and partnerships (including limited partnerships and limited liability partnerships).

What does it mean for me?

The tax analysis is by no means certain and there will undoubtedly be different views as to how the relevant statute should be interpreted.

What can I take away?

The anomalies created by the rules mean that numerous commercial situations involving the transfer of IFAs both by and to a partnership may trigger significant and unexpected tax consequences. Readers should exercise caution in considering the tax implications of such transactions.

It has been almost 20 years since the introduction of the intangible fixed assets (IFA) regime (Corporation Tax Act (CTA) 2009 Part 8), which fundamentally changed the corporation tax treatment of goodwill and intangible assets. A large number of updates have been made since then, but some of the rules continue to mystify through their unexpected tax consequences. This article focuses on the anomalous outcomes arising from transactions involving IFAs and partnerships (including limited partnerships and limited liability partnerships).

What is the issue?

The government’s objective when it introduced the IFA regime in April 2002 was to provide a fair and consistent approach to the taxation of intangible assets, which was more closely aligned with the accounting treatment. The regime broadly allows accounting debits and credits which arise under generally accepted accounting practice in respect of a company’s intangible fixed assets, including goodwill, to be followed for corporation tax purposes, although changes made in more recent years have restricted this to some extent.

As well as providing corporation tax relief for the costs of acquiring and enhancing IFAs, the regime incorporated a number of provisions, similar to those within the capital gains regime, to enable commercial reorganisations to be undertaken on a tax neutral basis. Unfortunately, the operation of these rules to partnerships involving companies seemed less well thought out.

The IFA rules are in point for partnerships with corporate members and/or for any transactions between partnerships and companies (including between a partnership and a corporate member).

For a number of years, in the absence of clear legislation and HMRC guidance, many had assumed that the IFA provisions operated on a ‘look-through’ basis – in a similar manner to the corresponding capital gains rules, which are supplemented by HMRC Statement of Practice D12. This transparent treatment seemed consistent with the way that corporation tax rules generally apply to partnerships (in line with CTA 2009 s 1259 and s 1273) and accordingly within the spirit of the rules, with no mischief intended.

However, HMRC perceived that some businesses had sought to exploit gaps in the legislation to obtain a tax advantage by using arrangements that utilised partnerships to circumvent the related party rules and bring ‘pre-FA 2002 assets’ into the IFA regime without a change in effective ownership. This led to a ‘clarification’ of the rules through Finance Act 2016. The new provisions focused on countering such arrangements but, frustratingly, had little concern for unduly adverse tax consequences that might arise in genuine commercial transactions as a result.

How do the rules apply in practice?

The difficulties arising from the application of the IFA rules to business structures involving partnerships can be demonstrated with the following example. Note that such hybrid corporate partnership structures are reasonably common.

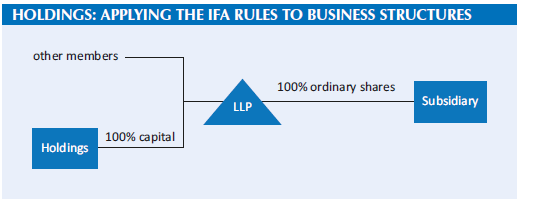

Holdings is the sole corporate member of LLP and holds a 100% capital interest in its assets. It is decided that the business and assets of LLP will be transferred to a company wholly owned by the LLP, Subsidiary, as a capital raising exercise may be undertaken in the future and it is considered that a more conventional corporate group structure will be preferred by investors. LLP’s most valuable asset is goodwill, which has been internally generated but has a current market value of £10 million. The business commenced after 1 April 2002, meaning that the goodwill is not a ‘pre-FA 2002 asset’ and, as such, is not excluded from the IFA regime.

Comparison with capital gains rules

For comparison purposes, if a non-IFA subject to taxation under capital gains rules was also to be transferred, the tax position would be relatively straightforward, insofar as the LLP would be looked through (per TCGA 1992 s 59A) and the transfer would be treated as though it were a direct disposal by Holdings to Subsidiary. Consequently, the disposal would give rise to no gain or loss under the intra-group transfer rule (TCGA 1992 s 171)).

Operation of IFA rules

In this example, however, the operation of the IFA rules to the transfer of goodwill has to be considered. Goodwill is deemed to include internally generated goodwill (per CTA 2009 s 715(3)) and specific provision is made at CTA 2009 s 738 to ensure that a taxable credit must be brought into account for corporation tax purposes if there is a disposal of an off-balance sheet IFA. The credit will be equivalent to the realisation proceeds, generally being the amount recognised for accounting purposes, subject to special rules which may impose that a different amount must be brought into account.

Related party transfers

The basic rule at CTA 2009 s 845 for related party transfers treats the transfer of an IFA between a company and a related party as being at market value. Related parties are defined at CTA 2009 s 835 but the cases do not adequately cover transfers to or from a partnership. Instead, specific provision is made by way of amendments to s 845, as introduced by Finance Act 2016. These amendments import the ‘participation condition’ from Taxation (International and Other Provisions) Act 2010 s 148 and provide that a partnership is a related party of another person if the ‘participation condition’ is met.

As LLP holds all of the shares in Subsidiary, the participation condition should be met, meaning that a taxable credit equivalent to the market value of the goodwill would be imputed by s 845 unless any exclusions apply.

Tax neutral transfers

We can then consider CTA 2009 s 848, which gives priority over s 845 to ‘tax-neutral transfers’, including transfers within a group falling within CTA 2009 s 775. Where the conditions of s 775 are met, an asset transferred between two group companies is deemed to be transferred on a tax neutral basis. It is unclear whether or how a transfer either by or to a partnership or LLP can ever fall within s 775 but there are two possibilities to consider.

The first is whether the transfer can be treated as made directly by Holdings, rather than by LLP. Unlike the capital gains rules, which confirm (at TCGA 1992 s 59 and s 59A) that capital gains are to be calculated at the partner level, no equivalent provisions are explicitly included within the IFA rules.

One could argue that look-through treatment is nevertheless applied to partnerships and LLPs in general by CTA 2009 s 1258 and s 1273. However, the decisions in the cases of Armajaro Holdings Ltd v HMRC [2013] UKFTT 571 and Bloomberg Inc and another v HMRC [2018] UKFTT 205 confirm that a general look-through is not deemed to be provided for all purposes, including accounting purposes. The IFA rules follow the accounting treatment, under which Holdings would be treated as holding an interest in a partnership as a fixed asset investment, whilst the LLP would be treated as the owner of the goodwill.

The second possibility is whether the LLP itself can be deemed to be a company and therefore a member of the IFA group. LLPs are expressly excluded from the definition of a ‘company’, ‘group’ and ‘subsidiary’ by CTA 2009 s 764. Nevertheless, the application of the IFA rules to partnerships and LLPs relies on references to a company to be read as references to a firm for the purposes of CTA 2009 s 1259.

Under s 1259, we are required to pretend that the partnership’s trade or business is carried on instead by a company and we may wonder whether this means that a partnership may be treated as a deemed company for wider purposes. This, however, is unlikely to be the case, with s 1259 being merely a computational device and having no effect on the actual identity and characteristics of the partnership or LLP in question.

Tax arising

In the absence of any overriding provision, s 845 will deem a taxable credit of £10 million, being the market value of the goodwill, to be brought into account when the goodwill is transferred. The credit would form part of the LLP’s taxable profits and be allocated to its members in accordance with the LLP’s profit sharing arrangements. Those members that are subject to corporation tax (in this example, Holdings) would suffer a dry tax charge in proportion to their profit share as a result of the transaction, with a tax liability of up to £1.9 million (based on the current corporation tax rate) arising.

Relief for expenditure incurred?

The confusing nature of the rules can be further demonstrated by considering the position if, in the example, Holdings paid actual consideration of, say, £5 million to acquire its interest in LLP.

As Holdings’ expenditure would relate to ‘the interest of a partner in a firm’, as per CTA 2009 s 807(1)(c), it would be an excluded asset for IFA purposes; whereas, under capital gains rules (TCGA 1992 s 59A), Holdings would be deemed to have acquired an interest in the underlying chargeable assets of the LLP.

If, for simplicity, we assume that the entire £5 million paid is attributable to the goodwill, Holdings would have a capital gains base cost of this amount in respect of the goodwill per TCGA 1992 s 38(1)(a). However, if a taxable credit arises under IFA rules on the transfer of the goodwill from the LLP to Subsidiary and forms part of the partnership profits allocated to Holdings, no relief for the actual expenditure incurred could be set against those profits.

Pitfalls

The tax analysis is by no means certain and there will undoubtedly be different views as to how the relevant statute should be interpreted. It is understandable that one may seek a particular reading in order to benefit from the tax neutral transfer provisions as that might appear most like the right outcome. Although it is difficult to believe that the seemingly unfair and inconsistent tax consequences arising are a matter of deliberate policy, in my view, such interpretations feel strained and run counter to the manner in which the IFA rules must generally be applied to partnerships in order to work.

The anomalies created by the rules are not limited to the scenario described in the example used and numerous commercial situations involving the transfer of IFAs both by and to a partnership may trigger significant and unexpected tax consequences as a result. Readers should exercise caution in considering the tax implications of such transactions.

Final thoughts

The government’s review of the IFA regime in 2018 raised hope that these issues might be rectified. It was noted in its consultation response summary (published on 7 November 2018) that stakeholders had suggested technical changes to remove anomalies including ‘introducing new rules governing the treatment of IFAs held by partnerships with corporate members’. Whilst acknowledging the suggestion, the response simply stated: ‘While these are outside the scope of the current review, they will be used to inform future policy work.’

The suspicion is that this was a way of kicking the problem into the long grass. However, the issue remains. In my opinion, the government should reconsider the matter as businesses should not be constrained from undertaking commercial reorganisations by poorly designed tax policy.

The CIOT OMB and Corporate Tax Committees are interested in hearing from members who have practical experience of significant problems caused by the application of the IFA rules to commercial transactions involving partnerships.

Please email [email protected] with the message of ‘Partnerships and intangible assets, Tax Adviser (November 2021)’ in the subject line.