Keeping it arm’s length

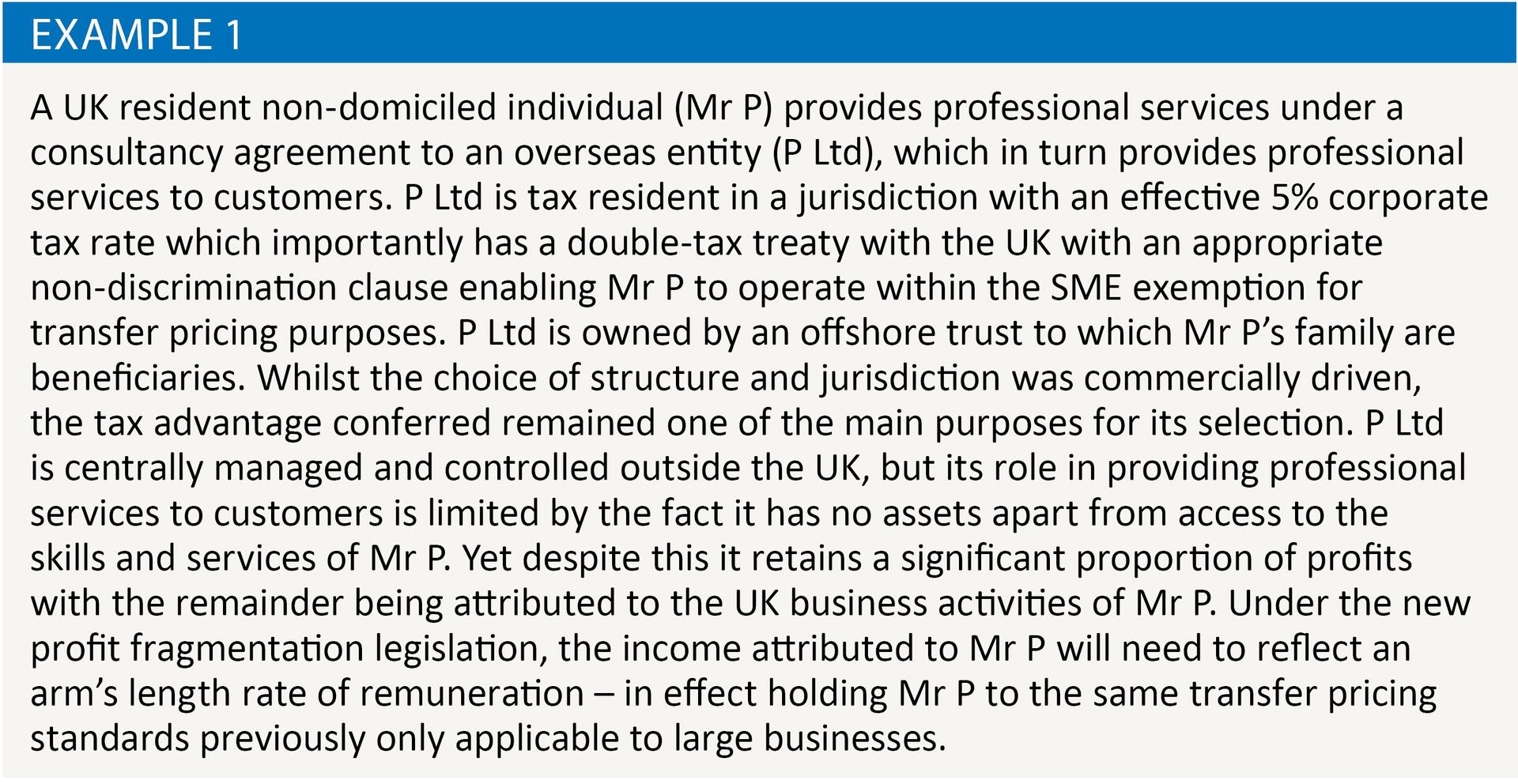

Share this article

Michael Beart and Francis Fitzpatrick QC consider the impact of the new profit fragmentation legislation

Key Points

What is the issue?

From April 2019 individuals, partnerships and companies undertaking a trade in the UK that intentionally divert profits to an offshore entity with a significantly lower rate of taxation will be within the scope of the UK’s new profit fragmentation legislation.

What does it mean to me?

The new tax provisions will effectively impose transfer pricing rules on certain businesses that operate within the current small and medium enterprise exemption.

What can I take away?

SMEs will need to develop OECD compliant transfer pricing policies.

Profit Fragmentation: transfer pricing for SMEs?

New legislation to tackle profit fragmentation was first proposed at Autumn Budget 2017. The government announced that it would consult on proposals to prevent UK traders and professionals from avoiding tax by arranging for their UK business profits to accrue to entities resident in territories where no tax or only a low rate of tax is paid. The stated aim was to target arrangements where profits derived from UK activity is ‘fragmented’ across jurisdictions, in particular where they are currently exempt from the UK’s transfer pricing rules as a result of qualifying for the SME exemption. Given that the exemption was originally introduced to ensure compatibility with EU legislation, the commencement date of April 2019 for the new legislation is somewhat poignant.

A consultation document ‘Tax Avoidance involving Profit Fragmentation’ was subsequently published on 10 April 2018 outlining a blueprint for the new rules and providing examples of the type of activity intended to be covered. On 6 July 2018 responses to the consultation were published, many of which argued that the proposals were unnecessary and simply added another overlapping layer of anti-avoidance. However, the proposals have been progressed as HMRC made it clear that they wanted the new rules and that they would shorten disputes under existing provisions.

Finance Act 2019 Schedule 4

The parties

Profit fragmentation arrangements involve the following parties:

- A person resident in the UK (the ‘resident party’);

- An overseas person or entity who is not resident in the UK (the ‘overseas party’) where this means a person abroad within Income Tax Act 2007 s 718 (a person resident outside the UK or an individual who is domiciled outside the UK) or a company, partnership, trust or other entity or arrangements established or having effect under the law of a country or territory outside the UK (whether or not it has legal personality as a body corporate);

- An individual (the ‘related individual’) who is either the resident party, a member of a partnership of which the resident party is a partner or a participator in a company which is the resident party.

Profit fragmentation arrangements

Arrangements are profit fragmentation arrangements if the following conditions are met:

- A provision has been made or imposed between the resident party and the overseas entity by means of the arrangements (the ‘material provision condition’);

- As a result of the material provision, value is transferred from the resident party to the overseas party which derives directly or indirectly from the profits of a business chargeable to income tax or corporation tax (the ‘value transfer condition’)

- The value transferred is greater than it would have been if it had resulted from a provision made or imposed as between independent parties acting at arm’s length (the ‘arm’s length condition’);

- Any of the enjoyment conditions are met in relation to the related individual (the ‘enjoyment conditions’).

The material provision condition is of course reminiscent of the ‘provision’ that must exist for the purposes of the transfer pricing provisions and one would expect it to bear a similarly broad meaning and to encompass conditions made or imposed as between the two parties. As was shown in the Dixons case [2009] UK FTT 31, there can be a provision made where there are a series of interdependent contracts between the two parties even where one of the parties in the chain is an independent party.

The value transfer condition is expanded upon in Paragraph 3 Schedule 4, which makes the condition extremely broad as one would expect. This provides, in summary, that account is to be taken of any method by which value is transferred from the resident party to the overseas party and explicitly includes both the transfer of property or rights and the enhancement or diminishment in value of any property or right. Value can be traced through any number of individuals, companies, partnerships, trust or other entities or arrangements. There is also provision for property held by a company, partnership, trust or other entity or arrangements, to be attributed to the shareholders, partners or members, beneficiaries or other participants at each stage on a just and reasonable basis. This seems designed to defeat arguments of form over substance and to introduce a substance approach with a look through structures to see where the real interests lie.

The arm’s length condition requires a determination of what value would have been transferred in a hypothetical transaction made between independent parties acting at arm’s length, which is an easy test to state, but is often very difficult to apply in practice as constructing a hypothetical transaction and determining hypothetical arm’s length values is often very challenging.

The enjoyment conditions are strikingly similar to the TOAA enjoyment conditions at Income Tax Act 2007 s 723. The enjoyment conditions are met in relation to a related individual if it is reasonable to conclude that some or all of the value transferred as a result of the material provision relates to something done by or any property or purported right of the individual and either:

- under the arrangements (the enjoyment arrangements): the value transferred is so dealt with as to enure for the benefit of the individual; the value transferred increases the value of assets held by the individual or held for his benefit; the individual receives or is entitled to receive any benefit out of the value transferred; the individual may become entitled to benefit if one or more powers are exercised (and so this would cover discretionary trust structures); or the individual is able in any manner, whether acting alone or with others, to control the application of the value transferred; or

- it is reasonable to conclude that the individual (whether acting alone or with any other person) procured the transfer of value from the resident party in such a way as to avoid the above-mentioned conditions being met. This means that in the unlikely event a person could somehow procure a transfer without falling within the enjoyment arrangements, they will be caught in any event.

References to an individual are also to any person connected with that individual within the meaning of Income Tax Act 2007 s 993 (with some modifications). Further, where an individual can exercise control over a person or entity or where the person or entity can reasonably be expected to act, or typically acts, in accordance with the wishes of the individual or a person connected with the individual, the individual and person will be connected. This seems intended to cover, for example, trustees who, whilst not obliged to do so, routinely act on the directions of a settlor for instance.

Exemptions

Even where all four of the above conditions are met, arrangements are not profit fragmentation arrangements if one of two exemptions is met:

- The material provision does not result in a tax mismatch for a tax period of the resident party (the ‘no tax mismatch exemption’); or

- It is not reasonable to conclude the main purpose or one of the main purposes for which the arrangements were entered into was to obtain a tax advantage (the ‘no tax advantage purpose exemption’).

With respect to the no tax mismatch exemption, there is a tax mismatch as a result of a material provision if the resident party obtains a deduction or reduction in income, where it is reasonable to conclude that the resulting reduction in tax exceeds the resulting increase in taxes payable by the overseas party for the same period, save where the resulting increase in taxes payable by the overseas party is at least 80% of the reduction enjoyed by the resident party. There are specific exemptions where the mismatch arises from, for example, payments under a registered pension scheme, payments to charity or to offshore funds or authorised investment funds which meet certain tests. Paragraph 6 Schedule 4 provides a formula for determining the reduction in the resident party’s liability to tax.

With respect to the no tax advantage purposes exemption, it is important to bear in mind that the rest will be failed if the main purpose or one of the main purposes is to obtain a tax advantage and as the Lloyds TSB Equipment Leasing (No 1) Ltd v HMRC [2014] STC 2270 case shows (see paragraph [65]) the fact there is a commercial motive for a transaction does not mean that it cannot also have as one of its main purposes the seeking of a tax advantage.

The adjustment

Schedule 4 Paragraph 7 provides in bald terms that adjustments must be made so as to counteract the tax advantages that would otherwise arise from profit fragmentation arrangements and must relate to the expenses, income, profits or losses of the resident party and must be based on what would have occurred if there had been an arm’s length provision and must be just and reasonable. It follows that one is likely to be looking at a transfer pricing type methodology with considerable discretion being conferred on HMRC.

Avoidance of double tax

Specific provision is made in Schedule 4 Paragraph 8 for avoiding any double payment of tax by reference to the same income or profits with the onus being on the taxpayer to make a claim for a consequential adjustment with HMRC being obliged to make such adjustments as are just and reasonable.

Existing anti-avoidance legislation

Whilst arrangements may be excluded from the transfer pricing rules, what is notable is that the examples suggested in the consultation process would fall within a number of the existing anti-avoidance provisions, as well as substance-based challenges due to the lack of any commercial rationale. The specific rules which spring to mind are the transfer of assets abroad rules in Income Tax Act 2007, yet in reality these are just the tip of the iceberg. HMRC have a raft of other anti-avoidance provisions in their arsenal that could be used to counteract profit fragmentation arrangements – for example the recently introduced disguised remuneration legislation. There is also industry specific anti-avoidance legislation such as the disguised investment management fee legislation for asset managers that operate in very much the same way.

In the consultation HMRC openly acknowledged that they have existing legislation to counteract such avoidance, but admitted that they find it too difficult to apply. Emphasis was placed on the need to force the taxpayer to disclose such arrangements and give HMRC the discretion to charge tax upfront if required, similar to that in the diverted profits tax legislation, although both of those elements have now been removed.

Given that, there seems little reason to think that any of the type of arrangements at which this legislation is aimed would be likely to survive scrutiny under existing rules. The profit fragmentation rules would seem to offer a short-cut for HMRC and an extra compliance burden, with the risk of collateral damage to innocent arrangements, for taxpayers. As will be apparent, it also raises the prospect that arrangements which pass muster under the transfer of assets abroad rules (because, for example, the motive test is met) will have to be reviewed under the new rules as well. Whilst both share a motive test exemption, the two tests are not identical so each need to be considered.

Practical implications

Non-domiciled individuals operating as sole traders or through partnerships stand to be significantly impacted by the new legislation. Generating non-UK source income is of greatest benefit to non-domiciled individuals filing on a remittance basis or those deemed-domicile who have put offshore structures into protected trusts – a planning route the government specifically made available upon implementation of the new deemed-domicile rules. It follows that such individuals are most likely to have established non-UK structures which are likely to be captured under the new legislation.

Importantly, individuals operating as a sole trader or via a partnership will be regarded as the resident party for the purposes of the tax mismatch condition. This means that income tax rates at up to 45% will be the benchmark against which the tax mismatch will assessed, considerably more than corporate tax rates currently at 19%. For such individuals incorporation to a company structure could be worth considering.

We understand that HMRC have been meeting with the BVCA to clarify the operation of these new rules for asset management businesses already within the disguised management fee and carried interest rules. Indications have been that where those existing rules have been properly applied, then the profit fragmentation rules will not change the position. Hopefully many of these issues will be addressed in promised guidance to be issued by HMRC.

Final thoughts

The key take-away for readers should be that many more taxpayers will need to develop an OECD compliant transfer pricing policy. This is a significant additional compliance burden as most of the current UK transfer pricing teams are set up to handle large businesses and their model will struggle to handle the needs of a raft of SMEs that will now require a transfer pricing methodology in order to comply with these new rules.

This is compounded by the fact that the existing demand for transfer pricing practitioners in the UK has never been higher. Political pressure, public opinion and the OECD’s Base Erosions and Profit Shifting project have all increased scrutiny of the transfer pricing policies adopted by large multinationals – meaning demand for transfer pricing skills will remain high and the market will take time to adjust – potentially leaving taxpayers at risk of non-compliance.

The information in this article is accurate at the time of going to press.