A last chance

Share this article

Mala Kapacee provides an overview of HMRC’s Worldwide Disclosure Facility

Key Points

What is the issue?

HMRC launched their Worldwide Disclosure Facility (WDF) on Monday 5 September 2016 as a ‘last chance’ opportunity for individuals to disclose UK tax liabilities relating to offshore assets.

What does it mean to me?

The WDF is a way of making straightforward disclosures to HMRC in a cost effective way for clients.

What can I take away?

The WDF is available to everyone with overseas assets and agents can submit disclosures on behalf of their clients through the HMRC Agent gateway.

HMRC introduced the Worldwide Disclosure Facility (WDF) on 5 September 2016 for individuals and companies to disclose undeclared UK taxes in relation to offshore assets. After the Panama papers story broke, the government was understandably wary of providing a facility that allows significant beneficial terms as permitted under the Liechtenstein Disclosure Facility. As a result, there is no immunity from criminal prosecution or reduced penalties.

Taxes that can be disclosed under the WDF include income tax, national insurance contributions and capital gains tax. Corporation tax and inheritance tax (IHT) are also included although IHT liabilities can only be disclosed for the past 20 years. VAT liabilities must be disclosed separately.

Although the WDF does not provide any beneficial terms per se, it should be borne in mind that unprompted voluntary disclosures to HMRC carry lower penalties than those prompted by ‘fear of discovery’ by HMRC. Fear of discovery could include notice of a formal enquiry by HMRC, an intervention letter or an informal request for information. More recently, HMRC have said that after 31 August 2017, they may treat a voluntary disclosure as prompted by either the ‘Requirement to Notify’ legislation or the introduction of the CRS. The logic being that after 31 August 2017, one way or another advisers with UK clients should have made them aware of the CRS and the various routes available for making a disclosure, via HMRC’s prescribed wording.

Where there was a lack of reasonable care and a voluntary disclosure has been made, the standard tax geared penalty of 30% can be reduced to nil provided that in telling HMRC about it, the person gave HMRC reasonable help in quantifying the inaccuracy and allowing HMRC access to records. If in the same scenario, the disclosure were prompted, the minimum penalty is increased to 15%.

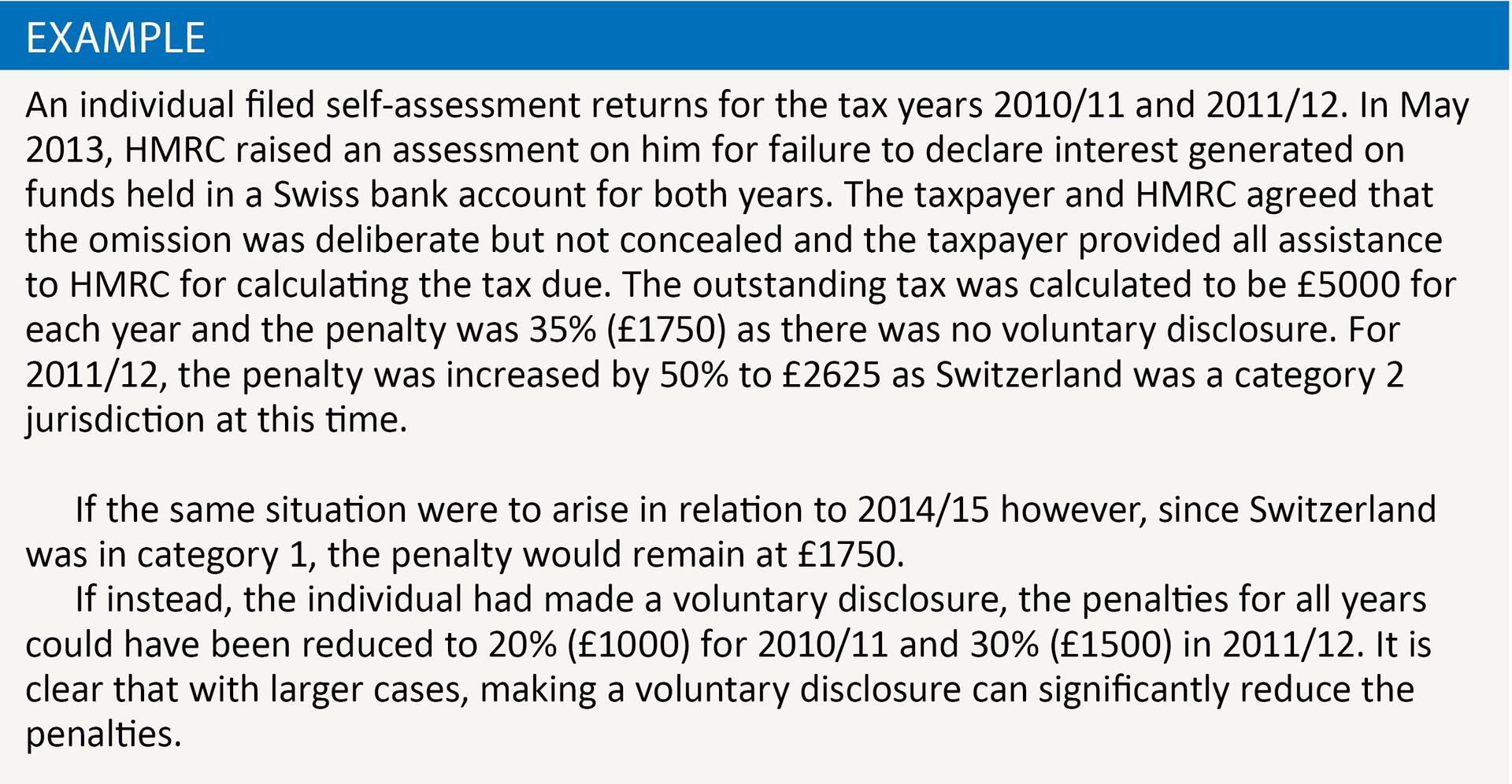

With effect from April 2011 the jurisdiction in which an asset was held affects the penalty. The jurisdictions are divided into three categories, with the most transparent jurisdictions being in category 1 and the most opaque in category 3. The UK is included in category 1. The penalties quoted above are for the most transparent jurisdictions including the UK. The tax geared penalties in relation to assets held in other jurisdictions are 150% or 200% of the normal penalty depending on whether the jurisdictions were in category 2 or 3 respectively.

From 6 April 2016, the applicable penalties have been reviewed to incorporate CRS jurisdictions in a category “0” with the penalties relating to categories 1, 2 and 3 increasing to 125%, 150% and 200% of the standard tax geared penalty. See the example.

As the WDF takes the form of an online disclosure, it removes the need to submit a detailed report. Nonetheless, care should be taken to ensure that the disclosure is complete and correct as, should HMRC find anything that was not brought to their attention, the person making the disclosure may then be open to a criminal investigation.

HMRC have advised that whilst they ‘expect the majority of disclosures to be accepted without an in depth enquiry’, they may need to ask further questions to substantiate the information provided. One drawback of the WDF is that there is very limited space to provide an explanation of the basis of the calculations or the behaviour that underlies the penalty loading. There is also the danger that unrepresented individuals that make voluntary disclosures themselves may be unaware of the correct penalty loading to use. The online disclosure form suggests that the minimum expected penalty for careless behaviour should be 10%, however, the penalty guidance from HMRC, advises that the minimum penalty could be 0%. The disclosure form also suggests that where less than the expected minimum penalty of 10% is applied, there may be some delay to acceptance of the disclosure.

HMRC are currently consulting on significantly higher penalties (up to 200% in total in the worst case scenario) in relation to the ‘requirement to correct’. Stricter sanctions and the ‘failure to correct’ legislation are also currently under consultation.

The WDF is available until 30 September 2018. This is in line with the deadline for all countries signed up to the CRS to carry out their annual reporting requirements. HMRC anticipate that the level of information they will receive as a result of the CRS means that they will be able to identify those with assets hidden offshore and therefore there is no need to entice people into making a disclosure or provide any beneficial terms for doing so. They have also indicated that from September 2017, individuals will no longer be able to obtain the maximum penalty reduction available for making a voluntary disclosure as HMRC consider that awareness of the CRS is effectively ‘fear of discovery’, which makes the disclosure prompted.

In addition, from 30 September 2016, advisers are required to notify clients (to whom they may have provided tax advice in relation to overseas assets) of the CRS and the fact that HMRC will soon be in receipt of significant information from overseas financial institutions. The wording of the notification is provided in Schedule 3 to The International Tax Compliance (Client Notification) Regulations 2016 and any adviser who is found not to have complied will be liable to a fine of up to £3,000.

The WDF is accessed through an online portal, the Digital Disclosure Service (DDS). The service is straightforward to use and in addition to the WDF, also provides access to various available campaigns and also voluntary disclosures in relation to UK assets, that do not fall under the other categories. The form is very straightforward and requires personal details (name, address, NI number) and each year’s tax liabilities. The person making the disclosure calculates the tax, interest and penalties due as with the normal disclosure process.

For more complex structures, HMRC have said that the non-statutory clearance process can also be used for those who have already registered to make a disclosure via the DDS. When making the disclosure, the individual is expected to consider their residence and domicile status and any trust issues if relevant. They are also required to self-assess their behaviour (whether reasonable care was taken in the preparation of the tax returns or whether the behaviour was careless or deliberate). Whilst these ideas seem second nature to tax advisers, clients may not be aware of the relevant legislation or how to implement it. It is imperative therefore that advisers make their clients aware of the facility and also highlight the areas that are more technical and may need further explanation or professional advice.

As part of the UK government’s commitment to crack down on tax evasion and non-tax compliance, Finance Act 2016 has legislated for a new criminal offence for offshore tax, which will take effect from April 2017. The criminal offence applies where an individual or entity fails to advise HMRC of a tax liability in relation to offshore assets. It is a strict liability offence, which means that HMRC do not need to demonstrate intent to evade tax. It is understood that the strict liability criminal offence will only apply to income tax and capital gains tax for now and that this will be reviewed in the future. Conviction of the offence could result in a fine or six month prison sentence.

In view of HMRC’s recent focus on tax evasion and political pressure for a ‘zero tolerance approach’ towards tax evasion, particularly in relation to offshore assets, it is imperative that taxpayers take professional advice in relation to the disclosure.