Legal fact or legal fiction?

Share this article

Harriet Brown considers deemed domicile status in the context of the new rules for non-UK domicilaries

Key Points

What is the issue?

Tax legislation often contains deeming provisions, which ask the reader to pretend a legal fiction is real.

What does it mean to me?

This is an introduction to some of the more important cases on deeming provisions and gives examples of how they apply in real-life situations.

What can I take away?

The general approach that should be adopted when dealing with deeming provisions.

Some context

In an article published in the October 2016 issue of Tax Adviser I discussed forthcoming changes to the rules governing the treatment of individuals not domiciled in any part of the UK. These rules were slated to be included in Finance Act 2017, but due to the calling of an early general election they were not so included.

Although it is anticipated that they are likely to be enacted subsequently in the last proposed, or substantially similar, form there is little to be gained from elaborating further on the provisions and their implications for taxpayers until we have more certainty. However, they raise a useful point about how deeming provisions generally should be interpreted and applied. In this article I discuss this in the context of those (still draft) provisions. To (briefly) recap, non-UK domiciled but resident individuals have, for many years, been in a privileged position with regards to UK taxation. These benefits, generally, have included:

- their non-UK situate property not being within their estate for inheritance tax purposes;

- excluded property status for non-UK situate property settled on trust while they were non-domiciled; and

- income and capital gains charges on the remittance basis.

These benefits have, however, been curtailed (generally by reference to the length of time of residence in the UK) by legislation, and the proposed provisions are to make further reductions to the amount of time that a person can be resident in the UK and still benefit from non-domiciled treatment. Currently (or, perhaps, previously, since the new provisions take effect from 6 April 2017):

- the Inheritance Tax Act 1984 (‘IHTA’), s 267, provides that a non-UK domicile will be deemed UK domiciled where he was domiciled in the UK within the three years immediately preceding the relevant time (the ‘Three Year Rule’) or if he was resident in the UK in not less than 17 of the last 20 years of assessment; and

- after a certain number of years has passed, the remittance basis may only be accessed upon nomination of income and gains to give rise to a certain amount of tax, with the amount rising from £30,000 where residence is for 7 of the previous 9 tax years to £90,000 where they have been UK resident in 17 of the last 20 tax years.

The new legislation proposes:

- retaining the Three Year Rule but adding a rule for those formerly domiciled in the UK (i.e. those born with a domicile of origin in the UK and meeting certain residence criteria) and reducing the time so that deemed domicile commences when you have been resident for 15 of the last 20 tax years;

- there is also a new rule for excluded property settled by a formerly domiciled individual, which will not be excluded property in any year in which the formerly domiciled person was a UK resident; and

- in relation to income tax and capital gains tax similar, though not identical, formerly domiciled and 15 out of 20 year rules will apply.

The upshot of this is that a number of new ‘deeming provisions’ are being introduced. While in tax we are generally familiar with deeming provisions, how to interpret them remains a difficult topic.

What are deeming provisions?

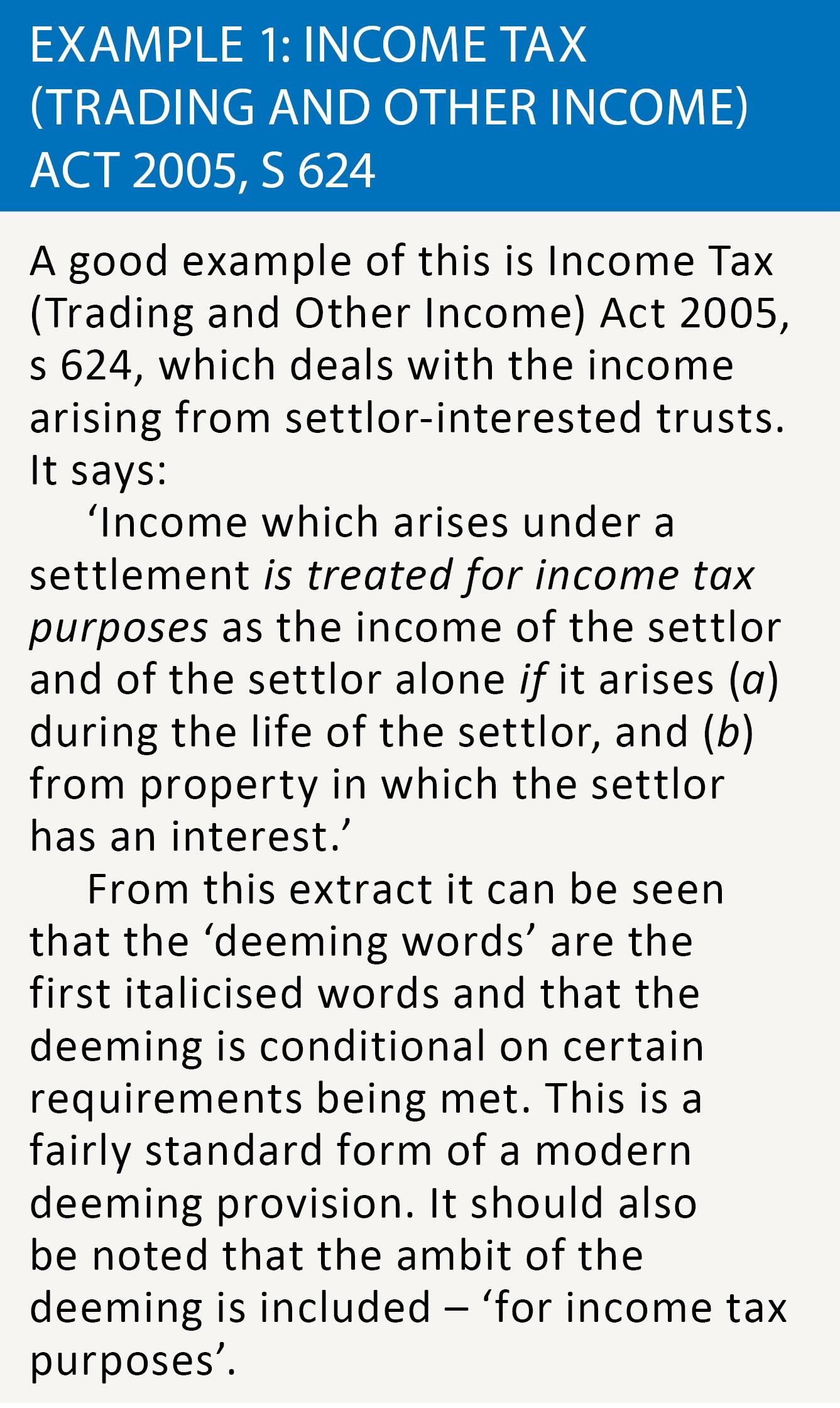

Deeming provisions are provisions that treat a situation as existing when it does not, in fact, exist. Such provisions are often referred to as creating ‘legal fictions’. In modern legislation rather than using the word ‘deemed’ provisions tend to say that something will be ‘treated as’. See example 1.

Certain issues arise around how to interpret deeming provisions – particularly how far to take the deeming, i.e. in what circumstances should the legal fiction created be considered to apply, and where one or more deeming provision interacts, how they interact and which one will take precedence if the legal fictions created are incompatible with each other.

How far will deeming go?

This has been for many years, and is likely to continue to be, a vexed question. Case law has developed certain broad principles that are applied in interpreting deeming provisions. These tend towards a purposive (as opposed to literal) construction. An early case, East End Dwellings v Finsbury Borough Council [1952] AC 109, sets out a good exposition of the general principle, saying ‘If you are bidden to treat an imaginary state of affairs as real, you must surely, unless prohibited from doing so, also imagine as real the consequences and incidents which, if the putative state of affairs had in fact existed, must inevitably have flowed from or accompanied it’. This of course begs the question as to how far one must go in considering the consequences of the legal fiction real.

Marshall v Kerr 67 TC 56 expanded on this, accepting that the consequences of legal fictions must be treated as real but stating a ‘rule’ as to when to stop treating consequences as real. In this case it was said ‘… because one must treat as real that which is only deemed to be so, one must treat as real the consequences and incidents inevitably flowing from or accompanying that deemed state of affairs, unless prohibited from doing so …’. Unfortunately, there was in Marshall v Kerr no clear guidance on what would constitute a prohibition from treating the legal fiction as real.

Of course the boundaries of the legal fiction are sometimes clear from the words of the statute. In the example given above, it can be seen that the legal fiction applies for ‘income tax purposes’, so we know that it would not be a fiction extending beyond income tax. Similarly in relation to the new deemed domicile provisions, in the last iteration of the proposed legislation a new Income Tax Act 2007, s 835BA was proposed which would have/will read ‘This section has effect for the purposes of the provisions of the Income Tax Acts or TCGA 1992 which apply this section’, so in those circumstances we know that the legal fiction only applies if we are told that it does by the section applying it.

However, such measures do not answer all questions as to the ambit of a particular legal fiction. This was recognised in Jenks v Dickinson [1997] STC 853 where it was said ‘It will frequently be difficult or unrealistic to expect the legislature to be able satisfactorily to proscribe the precise limit to the circumstances in which, or the extent to which, the artificial assumptions are to be made’. In Bricom v IRC 70 TC 272 the Court of Appeal said: ‘a statutory hypothesis, no doubt, must not be carried further than the legislative purpose requires, but the extent to which it must be carried depends upon ascertaining what that purpose is’.

So this leaves us without a ‘map’ for interpreting when the consequences of the legal fiction will peter out but, at least, with some instructions for ascertaining this in each case. Caution should be taken in assuming legally fictitious consequences without fully considering what the deeming was intended to achieve.

Barclays Wealth

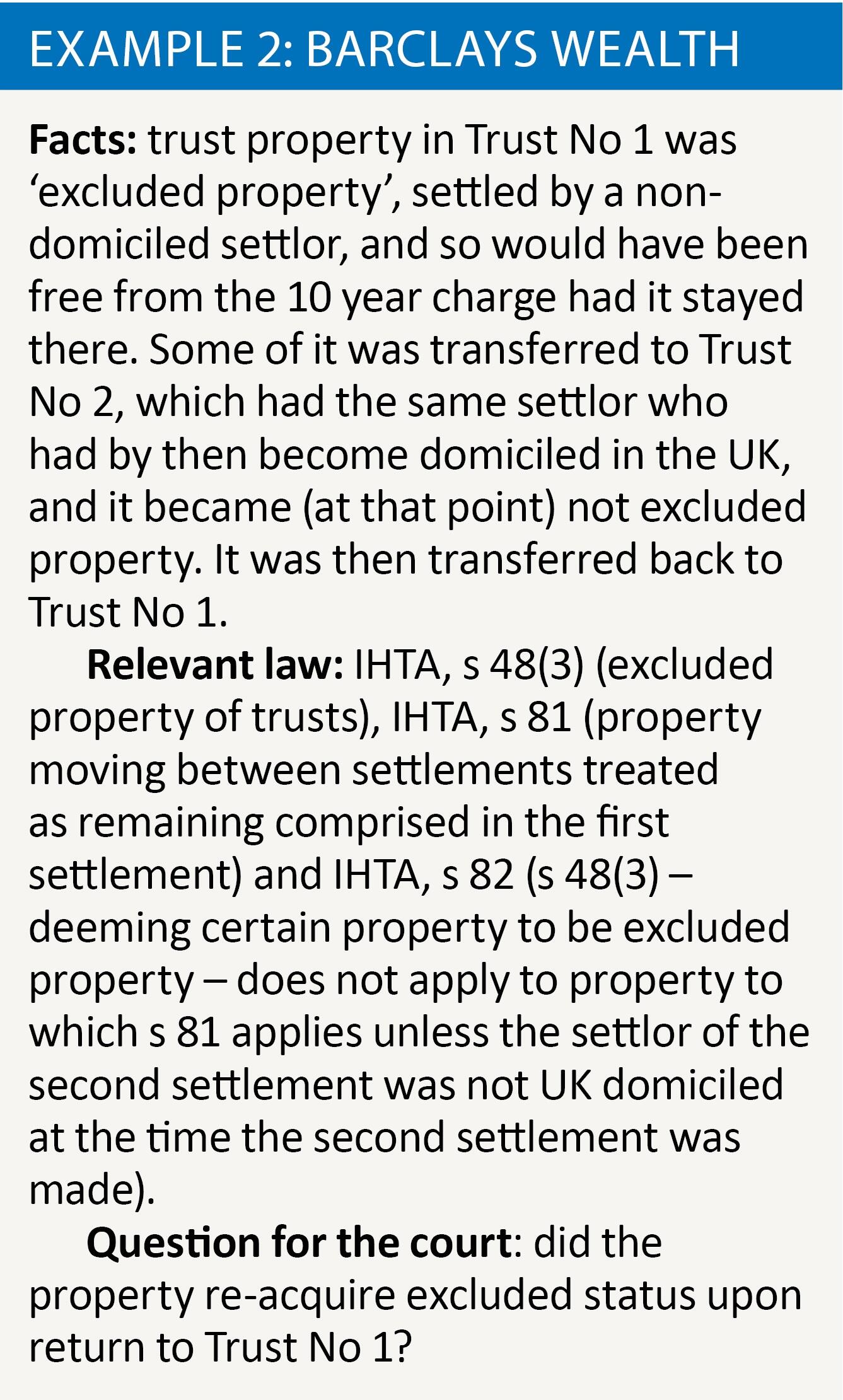

A recent and topical – the case is soon due to be heard by the Court of Appeal – case highlights this issue. Barclays Wealth v RCC [2015] WTLR 1675 considered certain deeming provisions in IHTA. See example 2.

It can be seen that Barclays Wealth deals with how far a deeming should be carried. IHTA, s 48(3) is not a deeming provision: it tells us when settled property will be excluded property. Excluded property is not relevant property and not, therefore, subject to the relevant property regime (10-year and exit charges).

IHTA, s 81 is a deeming provision. It tells us that for certain inheritance tax purposes we are to treat property that has moved from, in Barclays Wealth, Trust No 1 to Trust No 2 as still comprised in Trust No 1 IHTA, s 82 then attempts to ‘proscribe the precise limits’ of the legal fiction created by IHTA, s 81. It tells us that property to which s 81 applies shall not be taken to be excluded property by virtue of s 48(3)(a) unless the person who is the settlor in relation to, in Barclays Wealth, Trust No 2 was not domiciled in the United Kingdom when that settlement was made.

Thus it also creates a legal fiction of sorts itself (that the property in question is in Trust No 1 for some purposes but Trust No 2 for others) – that while we must treat property in Trust No 2 as still comprised in Trust No 1 with all that flows from this, we must consider the disposition of property to Trust No 2 as a separate disposition when ascertaining its status as excluded property. The question in Barclays Wealth, which seems a straightforward one turns, therefore, on the consequences on the deeming in IHTA, s 81 and the attempt by s 82 to prescribe the limits of the legal fiction created.

Mann J held that the property would remain non-excluded property after it was returned to Trust No 1. The taxpayer argued against this on the basis that the property returning to Trust No 1 acquires (or reacquires) excluded status because it becomes part of Trust No 1, and at the time that settlement was made the settlor was not domiciled in the UK, so s 48(3) applies. This argument relied on there being no third ‘settlement’ on the return of the property to Trust No 2.

In deciding how far to carry the s 81 deeming Mann J said:

‘The deeming provision in s 81 has to be considered carefully. It operates for the purposes of Chapter III, and only for the purposes of that Chapter … it would be going far too far to say that one inevitably has to treat a real world disposition as though it had not taken place at all. That is not necessary or inevitable. The taxation consequences of the deeming, so far as they are within Chapter III, might be inevitable, but the absence of a real world disposition is not.

… It is not necessary to assume that the disposition never happened. One just ignores its dispositive effect for the purposes of Chapter III. Accordingly one does not deem there to have been no disposition on that occasion. It is no more appropriate to deem there to be no disposition on the second … transfer. The funds were still treated, for the purposes of Chapter III, as being in [Trust No 2], but it is not necessary to go further and deem there to have been no disposition’

Thus Mann J gave the deeming provisions a narrow ambit on the basis of the wording of s 81. It remains to be seen whether or not the Court of Appeal will agree.

Conclusions

Where does this leave us? Interpreting and applying deeming provisions remains a far from straightforward task. That being said the former deemed domicile rule in IHTA has not yet been the cause of any great confusion as to its proper interpretation and, therefore, perhaps the new deemed domicile rules will follow this pattern.

Barclays Wealth, however, highlights the difficulties when trying to determine the limits to which the consequences of a legal fiction can be taken and careful thought should be given to taking appropriate legal advice in cases where the consequences of a legal fiction are determinative of the tax payable.