Life after Lobler

Share this article

Hui Ling McCarthy examines the impact of Lobler v HMRC and the proposed options for reform

Key Points

What is the issue?

HMRC are consulting on changes to the life insurance policy regime to prevent disproportionate tax charges from arising.

What does it mean for me?

Anyone with clients affected by the decision in Lobler should contact HMRC.

What can I take away?

Anyone with an interest in this area should review HMRC’s consultation document.

Consider this scenario: a recently retired couple sell their family home for £1m with a view to downsizing. They ask their IFA for advice on a safe place for their cash while they look for a smaller property. He tells them to invest in life insurance policies which offer slightly better growth than a bank account. The policies grow by £10,000. They duly find their new home for £800,000 and withdraw that amount. Their IFA completes the withdrawal form and returns it to the insurance company. The insurance year ends shortly after.

Now consider this: a group of pensioners have been persuaded by an unscrupulous IFA to invest their modest life savings of between £50,000 and £100,000 in various questionable financial products. They have been wrongly advised that the products are appropriate and low risk. The IFA completes all the paperwork and, in effect, makes all the investment decisions, investing in (and partly cashing out) numerous products over several years. The investments are a disaster: none is profitable individually and the pensioners lose everything.

If you ask the commercially-minded man on the Clapham omnibus how the two scenarios are taxed, after wondering whether it was a trick question he would invariably answer that the couple in the first one should surely pay tax on a proportion of their £10,000 gain; the pensioners in the second owe nothing since they made no profit at any stage.

No rational individual (without intimate knowledge of ITTOIA 2005 Pt 4 ch 9) would conclude that the couple in fact face a tax bill of about £400,000 and each pensioner owes HMRC tens of thousands of pounds. Yet these scenarios did happen. A quirk in the tax code deems the full value of the rights surrendered on a part surrender (not just any economic profit or gains) to be income, after deducting 5% of the total premium invested for each policy year.

The predicament facing these investors is especially egregious since other well-advised taxpayers took advantage of the same anomaly to generate millions of pounds of artificial tax losses under the avoidance scheme, which was the subject of HMRC v Mayes [2011] STC 1296.

It is well known that Mr Mayes’s success was one of the driving forces behind the introduction of the GAAR in 2013. At the time, CIOT floated the idea of a ‘reverse GAAR’ to ameliorate the effects of the tax code when it misfired and created disproportionate tax charges, but it was not taken further.

However, CIOT has since been instrumental in liaising with other organisations in the insurance industry and the tax profession, as well as with HMRC, to bring about law reform in this area.

Significant progress was assured when, in the March 2016 Budget, the government announced its commitment to change the tax rules for part surrenders and part assignments of life insurance policies to prevent excessive tax charges like these arising in future. On 20 April 2016, HMRC published a consultation document, Part Surrenders and Part-assignments of Life Insurance Policies, inviting views on three options for change, more of which later.

The product

Life insurance investment products (primarily investment vehicles) provide a policyholder with the ability to surrender all or part of the policy at any time. A UK-resident taxpayer is liable to income tax on any ‘gains’ as defined by the legislation arising on ‘chargeable events’, such as surrender, assignment or maturity. The tax regime works effectively on chargeable events which bring the policy to an end (for example, full surrender or maturity), in effect taxing the economic gain. The problem arises when value is derived from a policy without bringing it to an end (for example, part surrenders or part assignments).

The problem

On a part surrender or part assignment the full value of the rights surrendered or the full value of consideration received is the amount treated as the policyholder’s income, after a deduction of 5% of the total premium invested for each policy year. The 5% represents an annual cumulative allowance: policyholders can make part surrenders or part assignments of up to 5% of the premium paid each year the policy is held without incurring a tax charge. Although there are no gains at the point of withdrawal in these circumstances, the cash withdrawn is included as a receipt in the final gain calculation when the policy ends. So the 5% feature represents a tax deferral.

Any excess above the cumulative 5% threshold is, however, taxed in the year of part surrender. Accordingly, policyholders who partly withdraw substantial sums early on can unintentionally trigger swingeing income tax charges that far exceed the economic growth of the policy. A basic example used in Anderson v HMRC [2013] UKFTT 126 (TC) illustrates the point:

A taxpayer invests £1,000 in a single premium life policy. At the end of year one, the policy value is £1,100 (10% return has been earned by the insurer) and the policyholder withdraws £1,000. The return included in that withdrawal cannot exceed £100. However, the taxable chargeable event gain will be £1,000–£50 (5% of premium) which is £950.

If the policy had been surrendered in full by the end of the year, the gain would have been only £100 – the return on investment. If, in contrast, the policy is surrendered in full in a subsequent year, there is no reduction or repayment of the previous year’s tax charge. Rather, the regime provides for ‘deficiency relief’ that can be set against other taxable income of the later year (subject to restrictions).

In Mayes, significant chargeable event gains were triggered offshore so escaping the charge to UK tax; the policies were then brought back onshore and fully surrendered, triggering millions of pounds of deficiency relief that the taxpayer set against his other income that year. In contrast, the taxpayers in the two scenarios already described had no significant other income in the year of full surrender. They were left with massive tax charges in year one, together with equally substantial sums of deficiency relief in year two, which were useless.

Who has been affected?

The tax regime governing the taxation of part surrenders has drawn severe criticism from the First-tier Tribunal (FTT) in several cases. The investment habits of elderly or retired taxpayers have left them particularly vulnerable. These individuals may have invested life savings or proceeds on downsizing their house under the impression that these products are suitable for low-risk, short-term investment. Often they will have acted prudently and taken professional advice; in no cases I have come across have the policyholders’ decisions been motivated by tax avoidance. Yet, because of the way the regime operates, they faced a devastating loss of life savings and even bankruptcy.

Lobler

In Lobler v HMRC [2015] UKUT 152 (TCC), a tax charge of around £350,000 arose, yet the taxpayer made only a small economic gain. The FTT had held that the clear terms of the legislation prevented it allowing Mr Lobler’s appeal, despite the judge’s obvious sympathy.

The CIOT was granted permission to make submissions to the UT in the wider public interest of finding a solution for taxpayers in equivalent positions to Mr Lobler. As the UT (Proudman J) recorded at [5]: ‘The CIOT is in the process of gathering information from other interested parties and professional bodies in order to make a formal submission to HMRC and the Treasury with a view to obtaining a change in the law.’

The CIOT contended that the tax charges were disproportionate and that the legislation should be interpreted so that Mr Lobler could carry back the deficiency relief and set it against chargeable event gains in previous years. Although Proudman J considered that ‘the scales tip, only just’ in favour of HMRC’s contention that the tax charge was proportionate, the judge decided that he had made a ‘sufficiently serious’ mistake in completing the withdrawal form and erroneously selecting a part surrender across all policies.

Accordingly, the UT allowed Mr Lobler’s appeal and held that his tax position should be determined as if he had instead made full surrenders of policies to the extent possible. HMRC did not appeal.

Settling open cases in the wake of Lobler

Although it would be fair to criticise the government for not amending the insurance policy legislation sooner, those at HMRC tasked with handling the consequences of the UT’s decision in Lobler have made significant progress:

- HMRC has offered to settle cases stayed behind Lobler on the basis of the UT’s decision so that, in effect, taxpayers pay tax on the economic gain.

- HMRC has also engaged with the life insurance industry, industry and policyholder representative bodies and the tax profession about workable options for change.

The product of those informal discussions is the three options posed in the condoc. What follows is an outline of each option plus abbreviated versions of the examples given in the condoc.

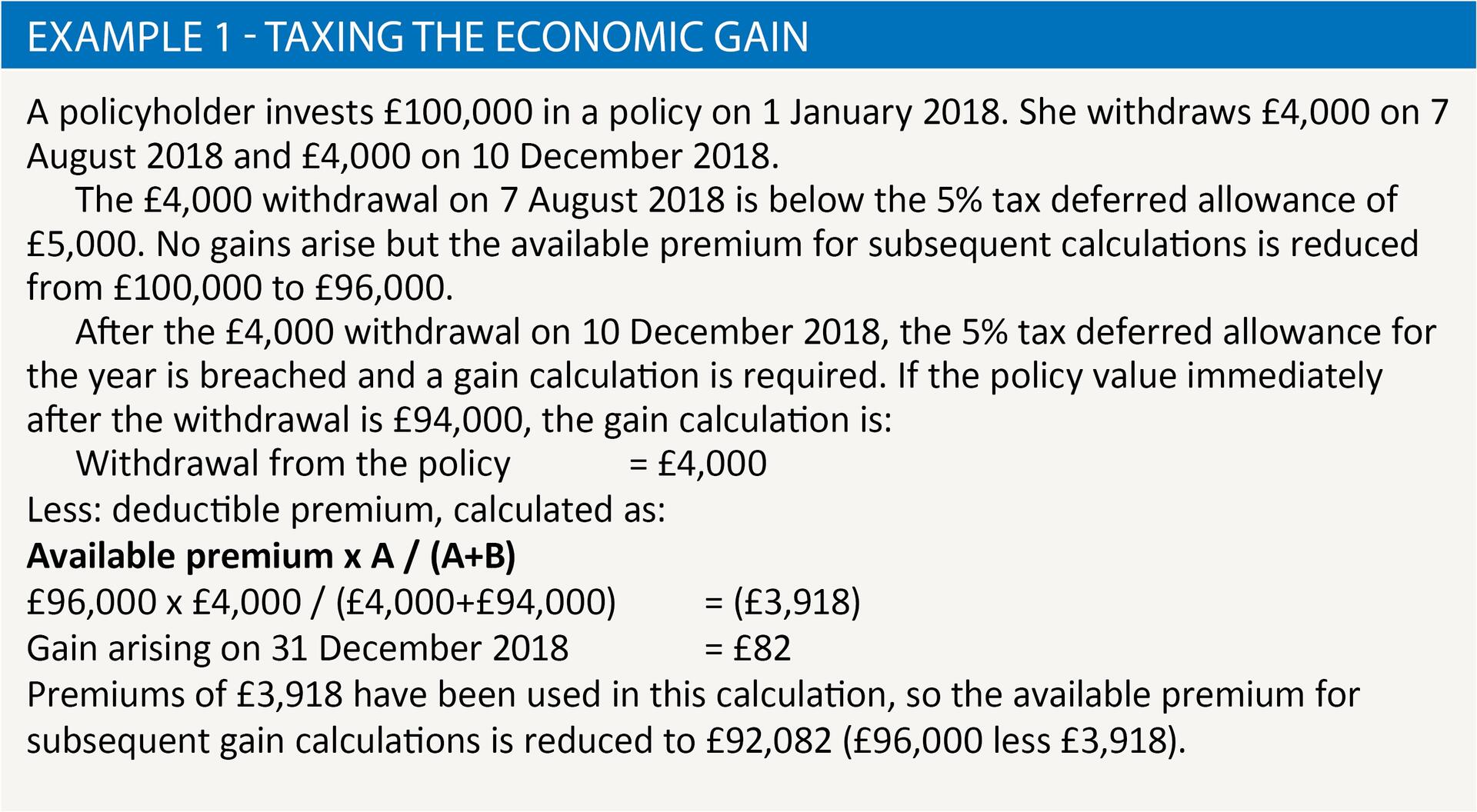

Option 1 – Taxing the economic gain

This option retains the 5% tax deferred allowance but brings into charge a proportionate fraction of any underlying economic gain whenever an amount in excess of 5% is withdrawn. Gains would arise only if withdrawals in excess of the cumulative 5% allowance are made and would always be an appropriate fraction of the policy’s economic gain. See Example 1.

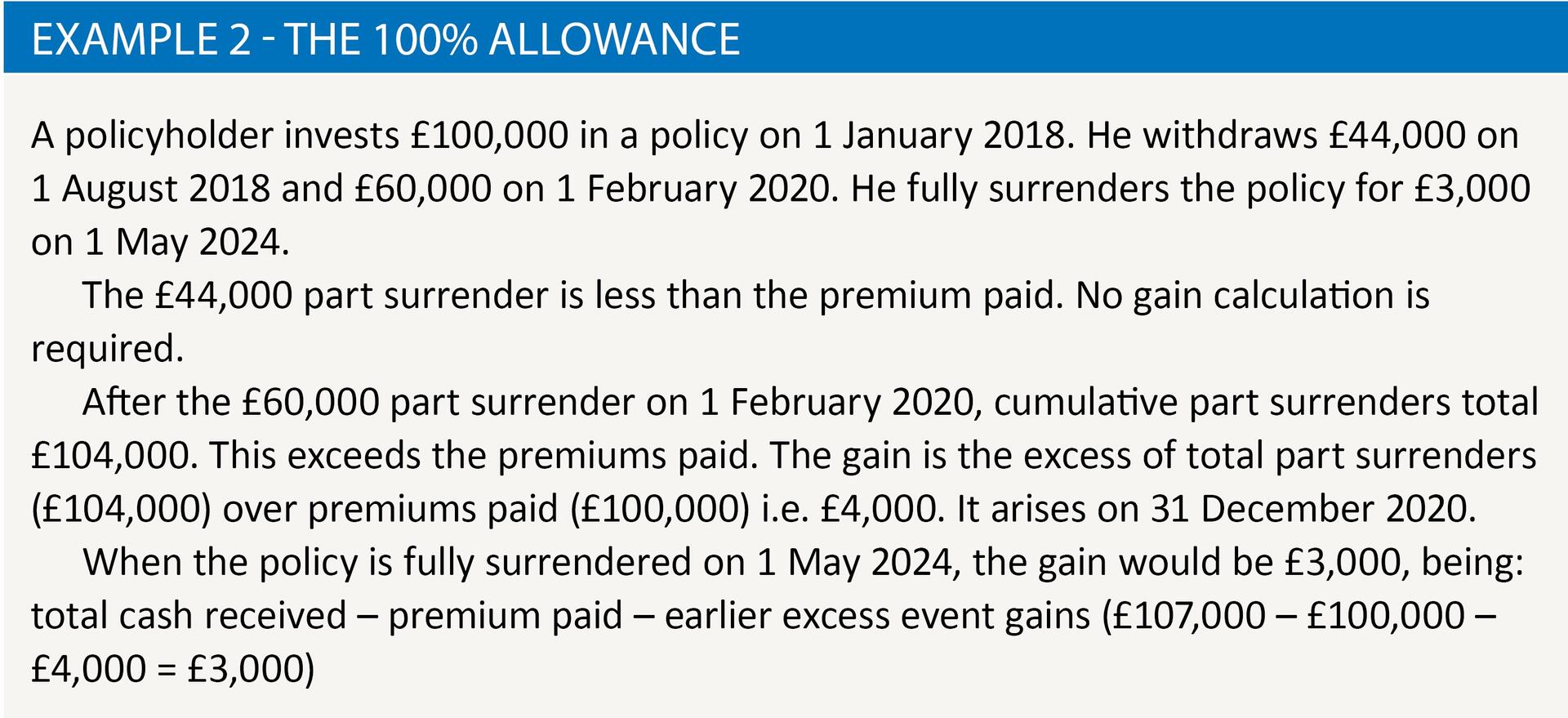

Option 2 – The 100% allowance

Here, no gain arises until all the premiums paid have been withdrawn. It would change the current cumulative annual 5% tax deferred allowance to a lifetime 100% tax deferred allowance and ensure that only economic gains are taxed. Once all premiums have been withdrawn, any subsequent gains would be taxed in full. See Example 2.

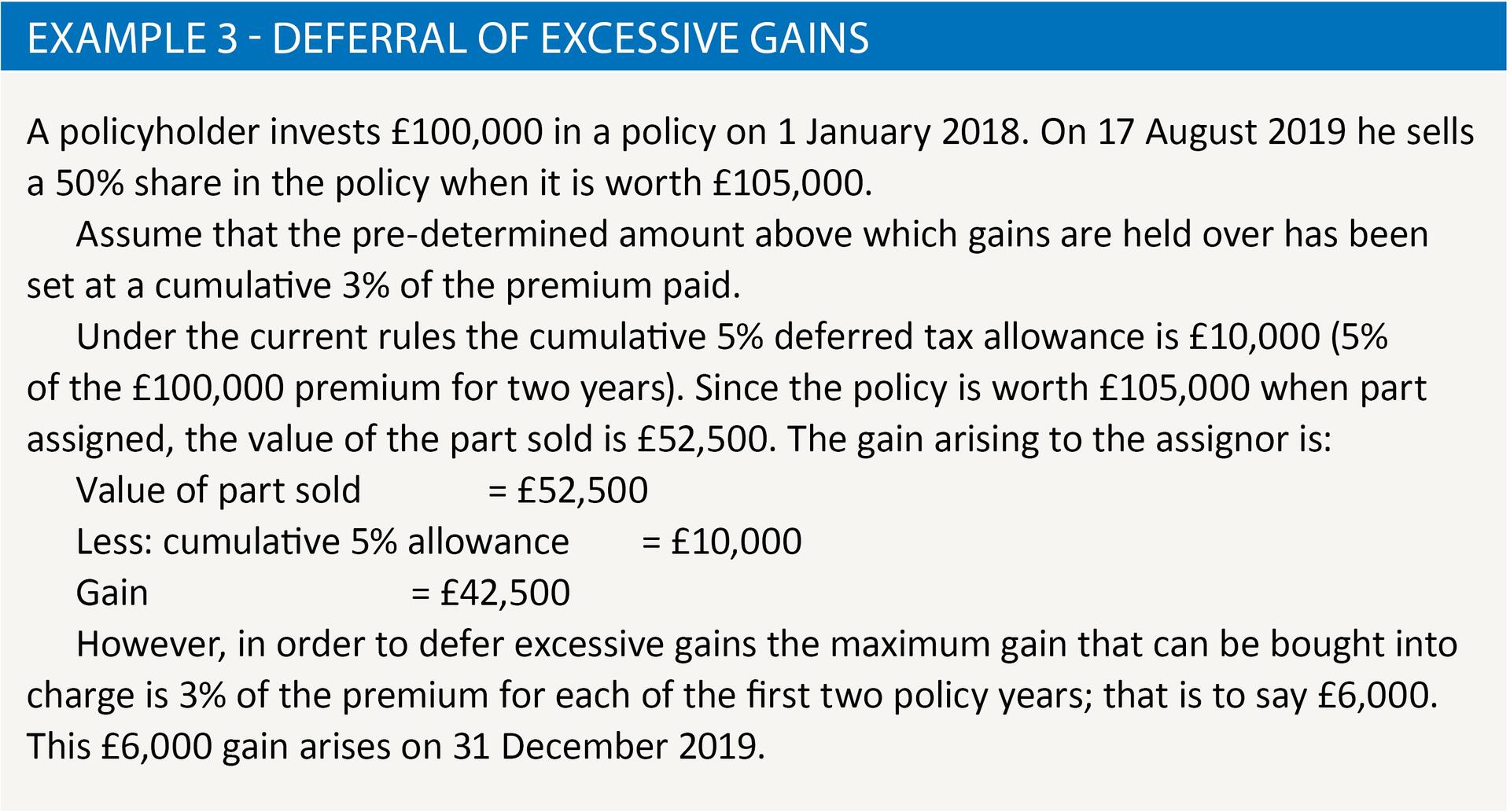

Option 3 – Deferral of excessive gains

If the gain exceeds a pre-determined amount of the premium (say, a cumulative 3% for each year since the policy started), the excess would not be charged to tax immediately. Instead it would be deferred until the next part surrender or part assignment. The gain arising from this would be increased by the amount of the deferred gain from the earlier event. If this total gain exceeded the pre-determined amount, the excess part of it would be deferred again (and so on). The gain on maturity or full surrender would be calculated by deducting premiums and gains (whether deferred or not) from total policy withdrawals. Deficiency relief might be available at this point if cash withdrawals are less than the total of premiums paid and earlier gains. The result would be that the total gains arising on the policy throughout its lifetime equal the economic gain from the policy. See Example 3.

From the perspective of the policyholders, each option will have charged to tax the overall economic gain made by the policy. But, in broad terms, the differences can be summarised as:

- Option 1 spreads tax charges over the number of years the policy is held by reference to the economic gain from the policy in each year of part surrender.

- Option 2 defers all tax charges to later years.

- Option 3 spreads tax charges over the number of years the policy is held by reference to the amount withdrawn in each year of part surrender, subject to a cap.

The government has identified certain desirable outcomes from any options for change, including:

- The prevention of disproportionate gains arising from any part surrender or part assignment – for new and existing policies.

- The maintenance of a tax deferred allowance (now 5%).

- Changes that are simple to administer and understand, with as few systems changes as possible for insurers.

- New tax avoidance opportunities are not created.

The condoc seeks to identify a preferred option, together with:

- a better understanding of the potential effects on policyholder behaviour and the life insurance market;

- whether any of the options (if adopted) might place additional burdens on policyholders;

- the likely costs to the insurance industry (for example, changing IT systems and advising policyholders);

- any consequential changes that needed to be made to reporting requirements; and

- any tax avoidance risks.

Conclusion

The option of most benefit to any given policyholder will depend on his personal circumstances and the performance of the policy.

For instance, any policyholder who becomes non-resident before using up the 100% lifetime allowance in Option 2 would be significantly better off if this option were adopted. Option 1, in contrast, might not find favour with the insurance industry if it requires insurers to make expensive systems changes. However, purely as a matter of tax policy, it might be the most coherent.

Although Option 3 seems more complex than Option 2, it has the benefit of spreading gains more evenly throughout the lifetime of a policy. However, in contrast to Option 2, Option 3 might give rise to chargeable event gains where there are no corresponding economic gains. These would, however, be capped at 3% as the proposal currently stands.

The consultation closes on 13 July 2016. Readers are encouraged to consider the condoc and submit responses to HMRC directly, or to the CIOT which will be preparing its own formal response to the consultation.

Further information

Read Keith Gordon’s article covering this case from the June 2015 issue of Tax Adviser.

Read the decision in Lobler on the Bailii website.

Read the condoc on GOV.UK.

If you wish to contribute to the CIOT’s response to the consultation, email Kate Willis at [email protected]