A little boost

Share this article

Lynne Poyser provides practical guidance on claiming the £1000 allowances for trading and property

Key Points

What is the issue?

The £1,000 allowances for property and trading income came into force with effect from 2017/18 onwards. The allowances are of most benefit to micro-entrepreneurs, such as those with secondary incomes, for example letting property through sites like Airbnb, and trading vie e-markeplaces.

What does it mean to me?

The allowances work in a similar way to rent-a-room relief, in that the taxpayer has choices based on the level of gross trading or property income in the tax year. However, it is important to be aware of the anti-avoidance provisions.

What can I take away?

Although limited in application, these allowances are useful, particularly since the trading allowance covers miscellaneous income from the provision of assets or services.

The £1,000 allowances for property and trading income came into force with effect from 2017/18 onwards. The trading income allowance also covers miscellaneous income from the provision of assets or services.

The allowances work in a similar way to rent-a-room relief, in that the taxpayer has choices based on the level of gross trading or property income in the tax year:

- income of £1,000 or less – either the income is exempt from income tax or the taxpayer can choose to disapply the allowance and calculate the profit or loss under normal business income principles

- income of more than £1,000 – either the profit or loss is calculated under normal business income principles or the taxpayer can elect to deduct the £1,000 allowance from his gross income and be taxed on the excess

The allowances are of most benefit to micro-entrepreneurs, such as those with secondary incomes from:

- letting property through sites such as Airbnb, although it is worth considering whether rent-a-room relief applies as the relief is more generous

- trading via e-marketplaces; however, remember that those selling their old possessions are unlikely to be trading

The allowances are set at £1,000 and can only be amended by secondary legislation, meaning it is unlikely the level of the allowances will be up-rated annually. As such, the value of these allowances is likely to be eroded over time by inflation.

Conditions

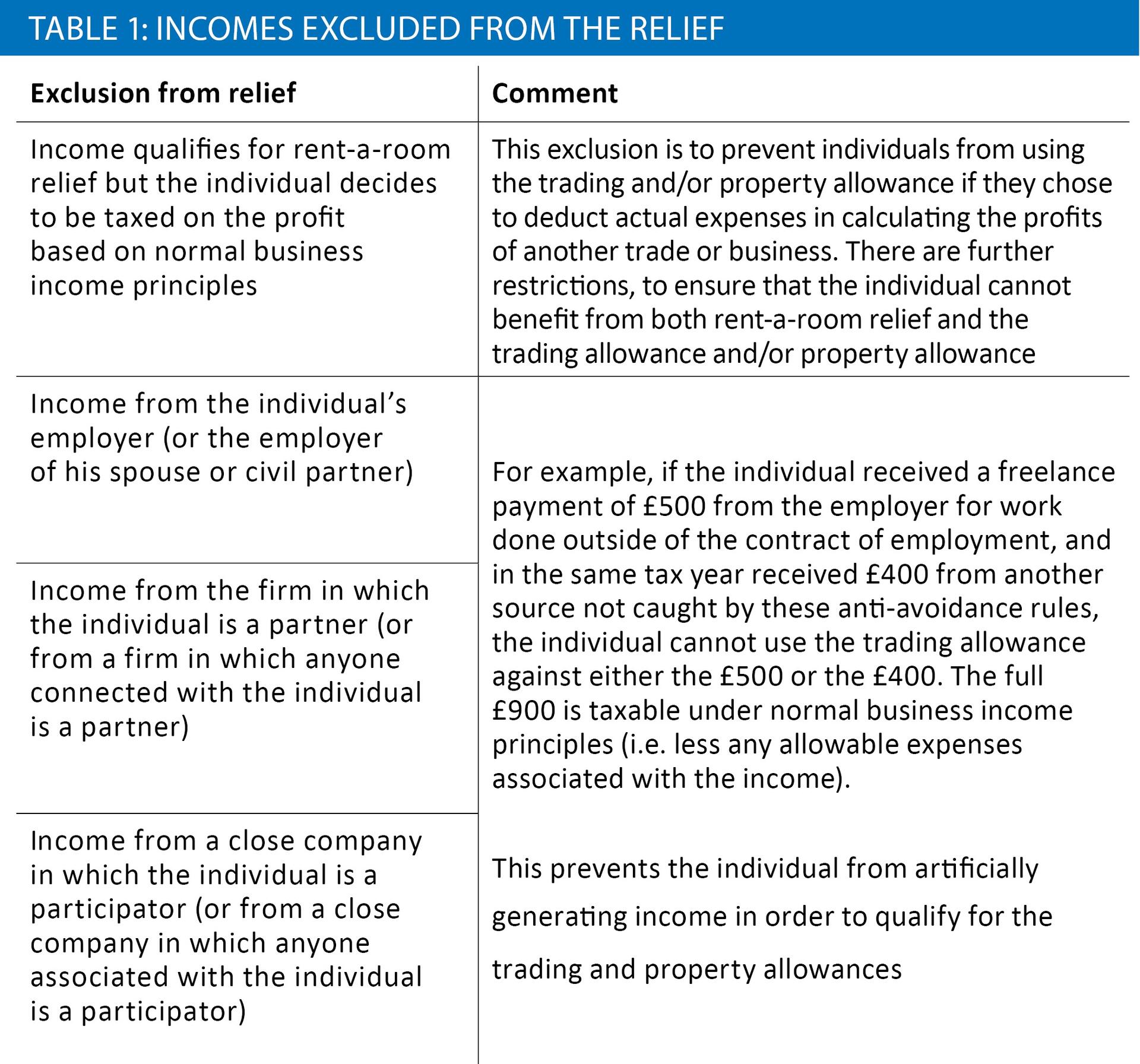

General exclusions from relief

Before considering the trading and property allowances in more detail, it is important to be aware of the anti-avoidance provisions that are common to both.

If the relevant income purposes of the trading and property allowance includes any of the income sources listed in table 1, the allowances are not available.

The presence of income from these sources effectively taints the individual’s relevant income for the purposes of the allowances.

However, just because one allowance has been tainted does not mean the other allowance has also been tainted.

The exclusions from relief need to be viewed separately in relation to both allowances.

Therefore, in the example in table 1 where the individual is disqualified from benefitting from the trading allowance, he may still be able to benefit from the property allowance in the tax year, provided the conditions below are met and the relevant property income does not contain any income caught by the exclusions from relief.

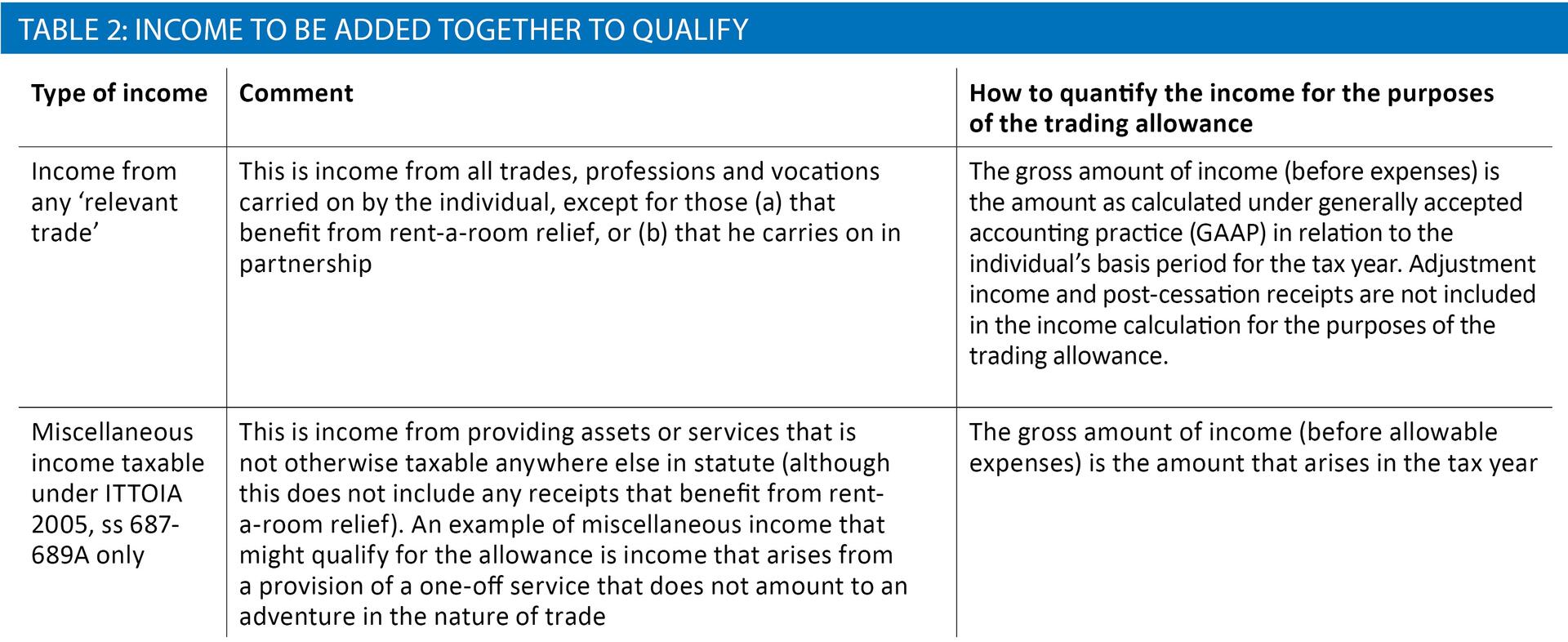

Relevant income for the trading allowance

Income must be added together to determine the relevant income for the trading allowance. See table 2.

The GAAP basis is used to determine the income from relevant trades because this is the default basis unless the individual elects for the simplified cash basis to apply.

The trader is unlikely to have made such an election if he is in a position to benefit from the trading allowance (i.e. low levels of gross income or low levels of allowable expenditure), meaning the GAAP basis applies.

However, if the individual had previously made an election to apply the simplified cash basis that is in force in the tax year, then the simplified cash basis would be used to determine the total income instead.

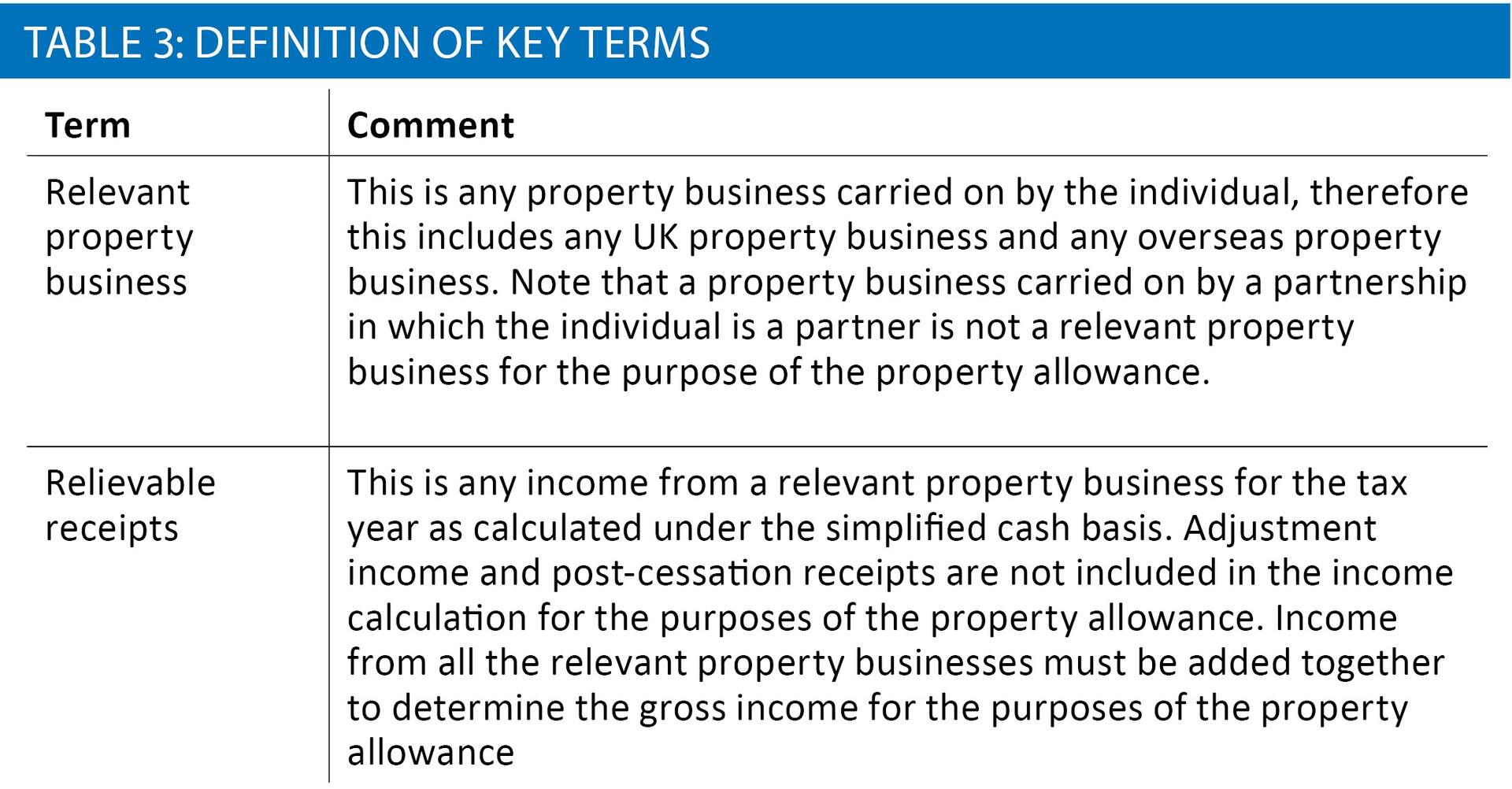

Relevant property income for the property allowance

The property allowance cannot apply to any individual who carries on a property business that includes residential property where there are costs incurred in relation to a dwelling-related loan(s). The legislation excludes anyone who receives relief for any part of these finance costs by way of a tax reduction under ITTOIA 2005, s 274A. Any individual who has a property business that incurs these costs is excluded.

The property allowance applies to the total ‘relievable receipts’ from any ‘relevant property business’ carried on by the individual. The definition of these terms is key. See table 3.

If the property business is owned jointly (so long as it is not run as a partnership), it is the individual’s share of the property income that must be taken into account when determining the amount of the ‘relievable receipts’.

The relievable receipts are calculated under the simplified cash basis, rather than GAAP basis, because the simplified cash basis is the default basis upon which property income is calculated. From 2017/18 onwards, the GAAP basis applies only if certain conditions are met, such as the receipts being over £150,000 in the tax year, or an election to use the GAAP basis has been made.

The following income does not qualify for the property allowance and is considered to be a separate property business:

- rental income that would have been taxable, but that benefits from rent-a-room relief

- distributions from a property authorised investment fund (AIF)

- distributions from a real estate investment trust (REIT)

Mechanism of relief

When determining whether the full or partial exemption applies, it is the gross income that must be considered (i.e. the income before deduction of expenses).

The £1,000 allowance for trading income and property income are mutually exclusive. Therefore, it is possible for the individual to have £1,000 of gross trading receipts (which must include miscellaneous receipts) and £1,000 of gross property receipts, and the entire £2,000 would be exempt from income tax under these rules.

The mechanism for relief under the trading allowance and the property allowance is broadly the same and is discussed below. Any differences between the two allowances are noted.

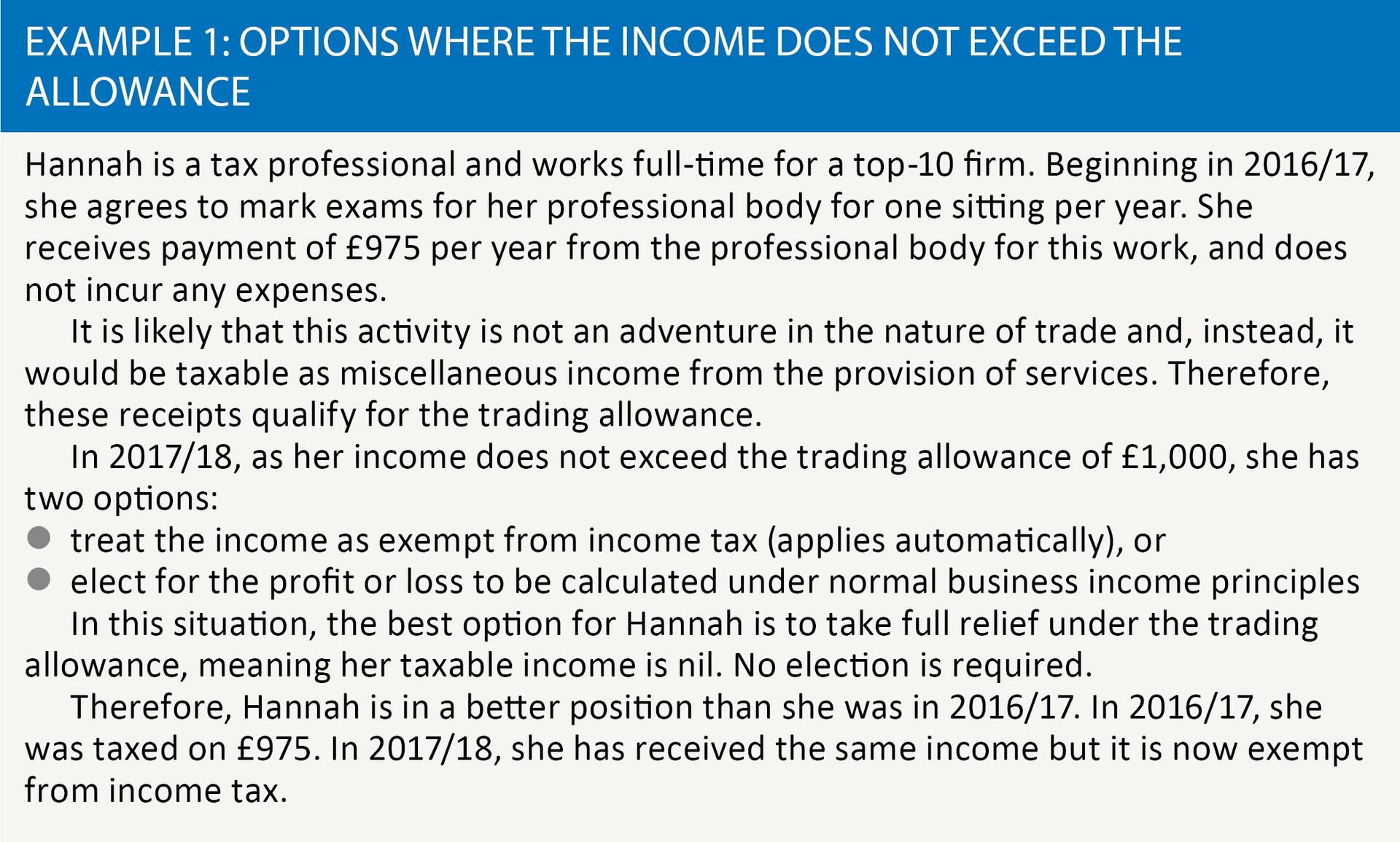

Full relief: gross receipts of up to £1,000

Where the gross receipts are less than or equal to £1,000, the individual has two options:

- treat the income as exempt from income tax (applies automatically), or

- elect for the allowance to be disapplied so that the profit or loss is calculated under normal business income principles (probably only worthwhile where the taxpayer has incurred a loss)

When deciding whether or not the total gross income from relevant trades is less than or equal to the £1,000 trading allowance, if using the GAAP basis would give gross income of over £1,000 but using the simplified cash basis would give gross income of less than or equal to £1,000, it is the simplified cash basis that is used instead. The legislation deems the individual to have made an election for the simplified cash basis, even though one may not have been made. In order to benefit, the individual must be otherwise eligible for the simplified cash basis both in that tax year and the preceding tax year. This relaxation on the calculation of income applies only for determining whether or not full relief is available. It does not apply where the individual has made an election for the trading allowance to be disapplied or where partial relief is in point; in these situations, the GAAP basis must be used unless an actual simplified cash basis election has been made.

The election for the allowance to be disapplied must be submitted by the first anniversary of 31 January following the end of the tax year (i.e. 31 January 2020 for the 2017/18 tax year).

Therefore, the taxpayer has the opportunity each tax year to decide which is the best option.

See example 1.

If the election is made and a loss arises, this is treated in accordance with the rules applying to the underlying nature of the income.

Partial relief; gross receipts of more than £1,000

Where the gross receipts exceed £1,000, the individual has two options:

- calculate the profit or loss under normal business income principles, or

- elect for the profit or loss to be calculated using the alternative calculation

Under the alternative calculation, the taxable receipts are restricted to the excess over £1,000, less any overlap profits. The deduction for overlap profits only applies to the trading allowance and might arise if the relevant trade ceased in the year or there had been a change of accounting date.

The election for the alternative calculation is worthwhile if the taxpayer has made a profit and the expenses are less than the £1,000 allowance.

As far as the trading allowance is concerned, where the individual has income from relevant trades and miscellaneous income, it is up to him how the trading allowance is allocated under the alternative calculation.

The only condition is that if the trading allowance is used against miscellaneous income, it cannot create a loss.

Therefore, it is possible for the individual to set the trading allowance against either source of income exclusively, or to allocate part to income from relevant trades and part to miscellaneous income.

Similarly, where the individual has more than one relevant property business (e.g. a UK property business and an overseas property business), it is up to him how the property allowance is allocated under the alternative calculation, although it is not possible to create a loss.

The election must be submitted by the first anniversary of 31 January following the end of the tax year (i.e. 31 January 2020 for the 2017/18 tax year).

As for full relief above, the taxpayer has the opportunity each tax year to decide which is the best option.

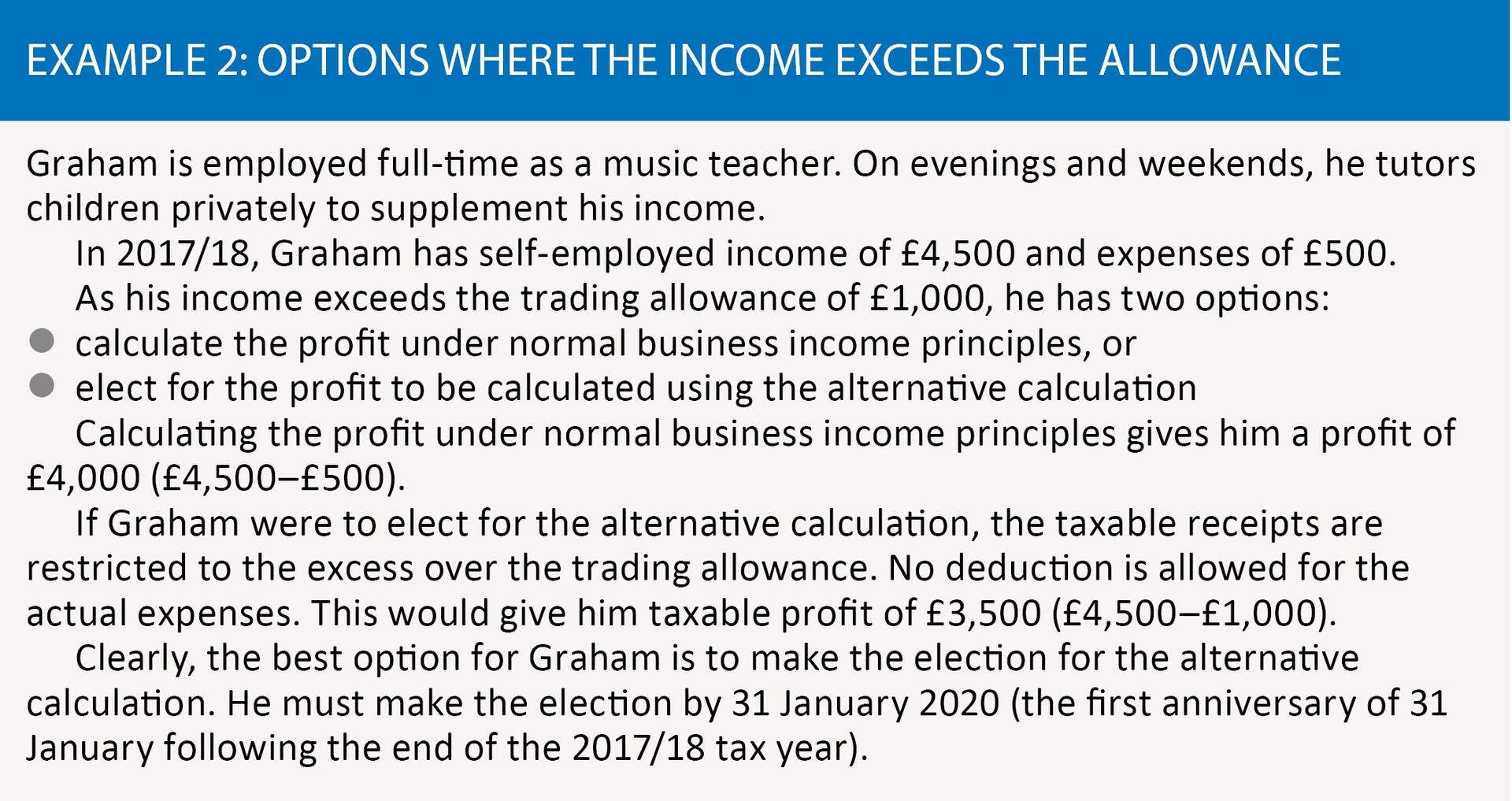

See example 2.

If a loss arises (i.e. no election is made), this is treated in accordance with the rules applying to the underlying nature of the income.

Conclusion

Although limited in application, these allowances are useful, particularly since the trading allowance covers miscellaneous income from the provision of assets or services. They are also available to most individuals; unlike some ‘allowances’, there are no exclusions or restrictions based on the level of the taxpayers’ other taxable income.

The Government launched a call for evidence on rent-a-room relief in December 2017. This has been widely interpreted as putting those who let a room(s) in their homes on a short-term basis, using sharing websites such as Airbnb, on notice that the generous rent-a-room relief may be coming to an end. Should this be the case, the individual may still qualify for the property allowance, although the individual would only benefit from £1,000 relief rather than £7,500 relief.