Living with the NMW

Share this article

Ian Goodwin and Jon Claypole provide a timely update on the current status of the National Minimum and National Living Wage

Key Points

What is the issue?

The National Minimum Wage (NMW) and National Living Wage has become a central business risk to address. Given this, all businesses now need to have an understanding of how they manage and comply with the NMW regulations.

What does it mean to me?

The NMW regulations are complex. Experience with handling numerous NMW investigations has shown that employers are not deliberately underpaying the NMW. Therefore, technical misunderstandings, or not having rigorous procedures in place, has led to underpayments arising.

What can I take away?

The NMW is not going away. Employers need to be managing their NMW repsonsibilities prudently or risk potentially significant financial and reputational damage. A starting point will be to make an individual responsible for its governance internally.

With more than 800 organisations named by the Department for Business, Energy & Industrial Strategy (‘BEIS’) in 2017 alone, the National Minimum Wage and National Living Wage (referred to collectively as ‘NMW’ throughout this article) has become a central business risk to address. Given this, all businesses now need to have an understanding of how they manage and comply with the NMW regulations.

NMW governance, like PAYE compliance, is an employer obligation. If an underpayment is discovered, it is the employer who will be required to correct and pay any penalties. This has been clearly communicated by the government: ‘All businesses, irrespective of size or business sector, are responsible for paying the correct minimum wage to their staff. The government is determined that everyone who is entitled to the National Minimum Wage (NMW) and National Living Wage (NLW) receives it’, Mel Stride, MP (12 September 2017 – Written Questions & Answers (7766)).

Therefore, all employers must act with due care and consideration when engaging and paying workers.

A short history of the NMW

The need for employers to be fully aware of NMW can be outlined by understanding how it has evolved since it was introduced:

- In 1997 The Low Pay Commission was set up, independent of the government, to make recommendations on NMW;

- From April 1999 the NMW regulations came into force, introducing a headline rate for those aged 22 or over of £3.60 per hour;

- The NMW rates were announced each October after consultation with the Low Pay Commission (up until October 2016);

- In April 2010, the NMW headline rate was changed to apply to workers aged 21 or over;

- The initial naming approach was introduced by the Department of Business, Innovation & Skills (BIS, now BEIS) in 2011, which led to over 700 employers being named between 2012-13, with underpayments of over £3.9m;

- In October 2013 the naming approach was updated, enabling BIS to name employers who had underpaid by more than £100. Previously underpayments needed to be in excess of £2,000;

- In April 2016, the government introduced the NLW for workers aged 25 and over;

- The NMW rates are now announced each April, rather than in October;

- The highest NMW rate is currently £7.50 per hour, an increase of approximately 108% since 1999. Within the same period a good costing £10 in 1999, would now cost £15.90, an increase of approximately 59% (using the Bank of England’s calculator);

- Since 2014, the government has more than trebled their annual funding of NMW enforcement, providing a total budget of £25.3m in 2017/18. As at 1 April 2017, there were approximately 400 staff in post in HMRC’s NMW teams nationally;

- In the Budget on 22 November 2017, it was announced that the highest NMW rate is increasing to £7.83 per hour from April 2018.

These developments illustrate that the risk of being named for underpaying the NMW is greatly enhanced.

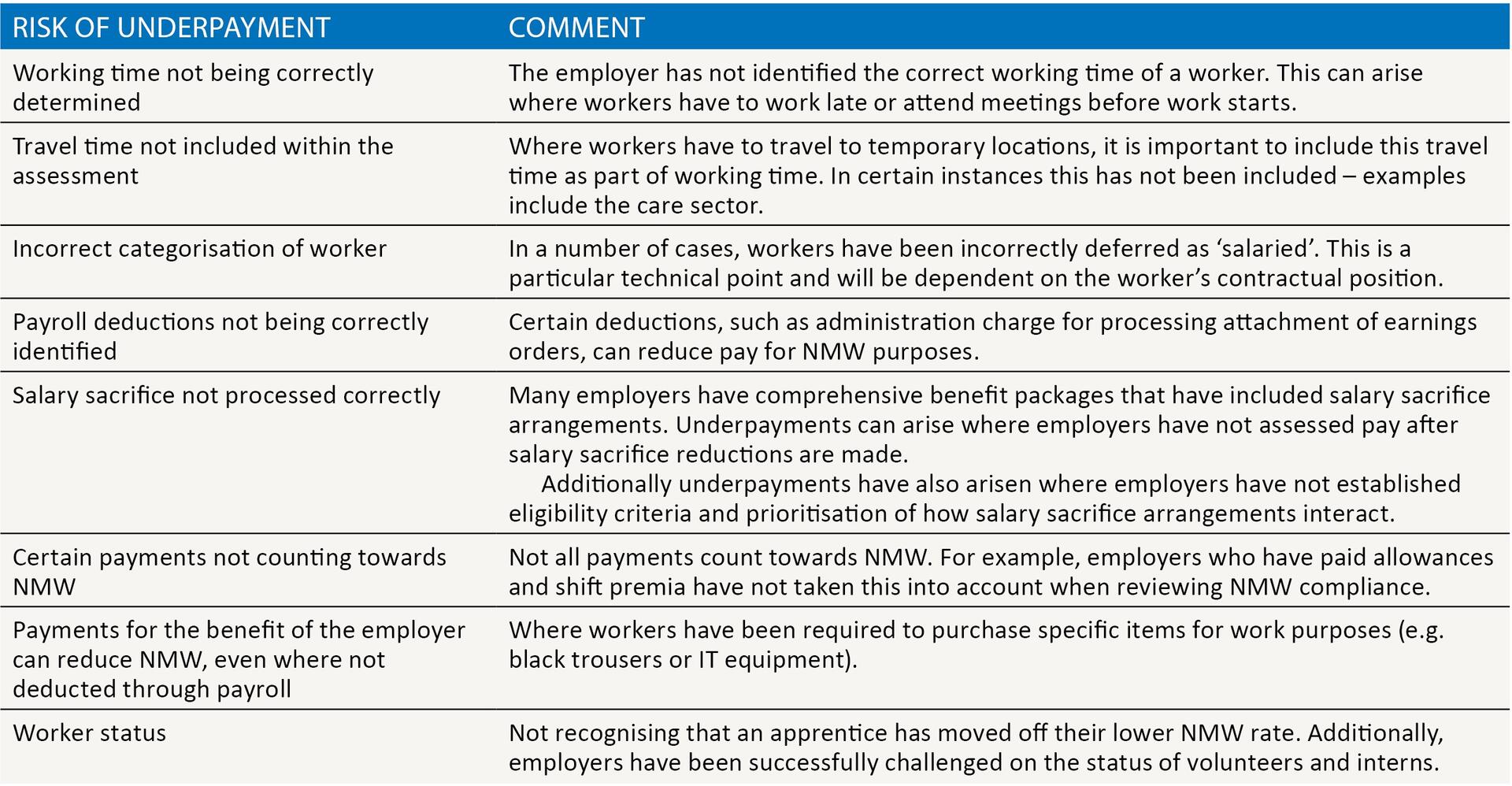

How are underpayments arising?

The NMW regulations are complex. Experience with handling numerous NMW investigations has shown that employers are not deliberately underpaying the NMW. Therefore, technical misunderstandings, or not having rigorous procedures in place, has led to underpayments arising.

Due to this, ‘how can we have underpaid the NMW if we at least pay in line with, or in excess of, the published NMW rates?’ is often asked by employers. The answer is that you can underpay surprisingly easily!

Table 1 is not exhaustive but provides a number of important examples to consider.

These examples demonstrate the importance of taking advice and ensuring steps are in place to control, govern and identify risks.

As there are lots of moving parts to NMW compliance, it is recommended that a collaborative approach is put in place to bring together disciplines including tax, payroll, HR, IT, communications, finance, legal and operations/people management. Appointing a senior individual to centralise the governance of NMW is often an important first step.

The enforcement landscape

1. Official enforcement

Formal NMW enforcement is undertaken by HMRC. However, it is the BEIS who are responsible for its overall governance.

The focus on NMW enforcement has accelerated and this is supported by the statistics. More than 260 employers were named and shamed in December 2017, compared to just 25 in June 2014. HMRC’s enforcement has been historically centred on hospitality and retail. However, no business is without risk and HMRC will, in our experience, investigate all complaints made across all sectors.

Non-compliance and being found to underpay workers will mean that the employer is required to:

- Make good the historic underpayments using the current NMW rates;

- Pay the additional PAYE/NIC and Apprenticeship Levy charge to HMRC;

- Potentially face a penalty of up to £20,000 per worker applied; and

- Potentially face criminal prosecution – to date, there have been 13 successful prosecutions for NMW offences since 2007.

2. ‘Unofficial’ enforcement

Increasingly, it is not just HMRC enforcement that is putting pressure on employers – it is the wider scrutiny created through improved data analysis, transparency of worker pay/wellbeing and the media’s focus on reputation that is enforcing change. It is ‘reputation’ that lies at the very heart of this type of enforcement.

Key developments to highlight the increased scrutiny include:

- The establishment of the Living Wage Foundation, a charity that publishes the ‘real’ living wage for London and the rest of the UK in November each year. This is a voluntary living wage and should not be confused with the NLW or NMW;

- The new requirement from 2018 to publish Gender Pay Gap data;

- The obligation to publish a Modern Slavery Act statement;

- The publication of the Taylor Review in 2017 which commented on many aspects of pay and engagements, but particularly employment status and the fairness of pay to those that may fit the role of ‘dependent contractor’; and

- The growing number of written questions and answers coming from MPs and Parliament.

Reputation is now central to any discussion on NMW. Reputation is critical for businesses and can make or break their success. Where underpayments are discovered, being named will damage reputation, impact on recruitment capabilities and also affect employee engagement, especially where there are wide pay differentials within an organisation. As outlined by a government publication in 2013, 80% of customers would not look to use a business that is found to be underpaying workers.

As scrutiny increases, government and HMRC focus further intensifies. In an age where attracting key talent is proving to be critical to the success of businesses, employers need to tread carefully not to be perceived as underpaying and undervaluing their workers. Where they are perceived in this manner, it could lead to customers and suppliers taking their business and services elsewhere.

Fundamentally, organisations need to realise that NMW/NLW compliance needs to become a core element of internal governance to help protect and enhance reputation and reduce the risk of non-compliance.

Being proactive

To avoid being named and paying penalties of up to £20,000 per worker, employers can choose to self-correct any underpayments. This will require knowledge of the NMW legislation and how HMRC approach investigations.

It is important that employers self-correct accurately. This is not a simple exercise. The employer will need to ensure there are no underpayments in the last six years. A key first step will be to establish the level of risk by reviewing a sample period (e.g. a six month period).

Should self-correction be undertaken and HMRC then discovers an underpayment, the employer will still be named and face potential penalties. One important point to note is that when self-correction does occur, the employer needs to make sure they make good the underpayment using the NMW rate in force in the pay period the underpayment has been identified, not the NMW rate for the pay period when the underpayment occurred. This is often an area where employers who self-correct fall down as they use the wrong NMW rates.

In certain cases, HMRC may also agree that self-correction can be undertaken, given their main objective is to ensure workers get paid correctly. This has recently been demonstrated more formally with the launch of the Social Care Compliance scheme for employers in the social care sector. More widely, developing a trusted relationship with HMRC will be important in establishing whether self-correction is available.

Furthermore, employers have an opportunity to use the increased HMRC NMW activity as a timely opportunity to review how pay and reward is structured and communicated. By communicating pay by using Total Reward Statements and online technology effectively, employers can reduce the risk of complaints arising and establish attractive and rewarding pay strategies that workers value. This can help increase retention and recruitment, as well as enhance productivity and, ultimately, reputation.

What next?

It is understood that the government is reviewing the NMW rate for apprentices and that there is due to be a second reading in Parliament later in 2018 to expand the payment of the NLW to those aged 21 or over.

Additionally, the interaction with employment status cannot be ignored. As the Taylor Review identified, there is pressure on businesses engaging self-employed workers, particularly in the ‘gig’ economy, to pay in line with the NMW.

As a final word, the NMW is not going away. Its importance is only likely to increase. Employers need to be mindful of managing their responsibilities or they will risk significant financial implications and reputational damage.