Mastering tax

Share this article

Andy Lymer explains why universities play an important role in the development of tax professionals

Key Points

What is the issue?

Are universities likely to continue to play an important role in developing the next generation of tax professionals?

What does it mean to me?

With multiple routes into the tax profession, I need to know what I can expect of a university graduate – it may not be what I brought when I joined from a university, if I went to one. Is what they are offering now what we need? Could a master’s degree be something of value to me and my staff?

What can I take away?

Is there a role I can play in shaping the next generation of tax professionals studying at a university? Can I offer advice and support to my local university, or one I have a particular link to perhaps as an alumni? They will probably welcome my contact.

Historically, tax has been one of the traditional graduate professions. However, as the world is changing, is there still a role for universities to help develop the next generation of tax professionals? Will direct entry schemes provide the bulk of the cohort in the future? Will higher degrees and the probably forthcoming degree apprenticeships in accounting or law, or even tax itself, be key suppliers of future CIOT and ATT members?

I am perhaps not the right person to argue against the proposition that universities should continue to be a key provider of future tax professionals – I am hardly unbiased! So, assume what follows is the case for universities remaining a key supply channel, albeit changed in key areas.

Universities have been central in developing people who form the basis of most of the UK’s professions, and tax is no different. If we use CIOT and ATT membership pipelines as a proxy of the current trend of graduate mix within the tax profession, in the past six months at least 63% and 70% respectively of new student applicants have been graduates. Meanwhile, 4% of CIOT applications have higher degrees (master’s or PhDs). However, that clearly suggests around one-third of new entrants are looking to build careers in tax without having gone through university.

Universities, therefore, are far from providing the only entry route into this profession. There have always been other entry routes into a profession that rewards talent regardless of educational background. However, a university education, whether related to tax or on a different and unrelated subject, has been the main route in.

Universities provide a chance for personal and technical development in the chosen field of study. They allow students to leave home, often for the first time, into a fairly controlled halfway house to the ‘real world’, to develop their intellectual skills to become freer thinkers, and to explore the theoretical as well as the practical elements of their chosen subject. Good university programmes should provide a foundation that does not merely deliver ‘off the shelf’ technical capability, but also provides breadth of understanding and a grounding in principles and theory that can be applied throughout a subsequent career.

That is the theory anyway. In practice universities do this to varying extents; people experience different mixes of the technical and theoretical elements of their subject based not only on the institution they study at, but also the individual lecturers they are exposed to. What specific mix prospective students can expect has been difficult to judge from the packaging since the convergence of the polytechnics, with their bias towards technical skill development, and universities, which accentuated theory and principles. These days, neither technical skill nor theory-based courses intrinsically offer ‘better’ employment prospects because all higher education establishments, of whatever type, meticulously plan their programmes and linked activities to benefit their ‘customers’.

The new teaching excellence framework (TEF) assessment, coming to a university near you soon, may well bring institutions closer together yet further, because it will require more information on teaching activities to made available to the market, detailing what happens within any particular ‘ivory tower’.

Universities have had to face up to a changing world as students, being the direct purchasers of services and products the institutions are selling, become customers in the fullest sense of the word. They are now responsible for settling the fees for their courses, give or take their eligibility for government loans, or another lender like the ‘bank of mum and dad’. Since March 2015, according to the Competition and Markets Authority, universities have fallen under consumer rights legislation, giving the buyer of a degree the same rights as if they were sold any other product or service. This makes developing and evolving courses during that period’s study more difficult for universities.

Within this dynamic environment, what is offered as tax education by UK universities at present? How are tax education offerings affected? Perhaps, a little oddly, there are only two undergraduate degrees containing a substantive amount of the subject to warrant using the ‘tax’ in their course titles. Both degrees are at the University of Bournemouth: BA (hons) accounting and taxation; and LLB in law and taxation. Perhaps it is unrealistic to expect 17-year-olds to opt for a tax-focused degree in significant numbers to make it a more mainstream offering. Degree apprenticeships might change this, with universities eyeing up such an opportunity – more of which later.

Our profession benefits from attracting people who have studied degree courses that span a range of professional disciplines, such as business, law, economics, or even an unrelated degree, before recognising the particular attractions of a career in tax. Many accounting, law and economics degrees will have at least one tax course required of students, with some offering a second.

At my institution, for example, students are lucky enough to be given an introduction to income taxes (UK personal and corporate tax) and consumption taxes (VAT) in a compulsory course on our accounting degrees, and an optional final year in comparative and international tax (with wealth taxes thrown in for good measure). Law students can take a revenue law course and those taking economics-related degrees will have various macro and public economics courses that offer different perspectives on the need for, and role and use of, taxation. We have also taught tax to social policy and politics students. This is typical of many ‘research-led’ universities and others that would not class themselves that way. In many cases, syllabuses of professional accounting bodies are followed closely for bachelor degrees that provide significant exposure to tax for students on those programmes.

It could be argued that such courses provide only limited exposure to tax in the ‘real world’, however, so fail to adequately sell tax as a career of choice. Offers of experience and short-term internships help to address this by becoming common additions within degree courses.

Many undergraduate degrees offer a chance to extend business placements. At Bournemouth University there is a 40-week placement option. These have not always been a formal feature of accounting, economics or law undergraduate degrees at ‘research-led’ universities, with the exception of Aston and Bath. They do, however, appear at Coventry, Derby, De Montfort, Hertfordshire, Leeds Beckett, Manchester Metropolitan, and Westminster to name a few. However, this is changing quickly with more universities embracing the value of extended periods of work combined as formal parts of their programme offerings.

New university-level programmes called degree apprenticeships are being promoted by the Department for Business, Innovation & Skills. These require universities and employers to work together to form undergraduate, and perhaps higher-level, programmes that will create a middle way between conventional three- or four-year degrees and direct entry into work. These schemes are part of the government’s apprenticeships programme overhaul and an extension to the new higher apprenticeships (level 4 and 5 – up to foundation degree level) that cover many business areas, including accountancy and law. The schemes received a significant financial increase after announcement in the autumn statement of the apprenticeship levy/payroll tax that will come in to effect from April 2017, promising ‘three million apprentices by 2020’. Although degree apprenticeships (level 6 and 7 – undergraduate and master’s degree levels) will form only part of this ambitious aim, they are likely to be rolled out in subjects now without them, including accountancy, law and, more specifically, tax. This may significantly affect the ‘sandwich course’ market.

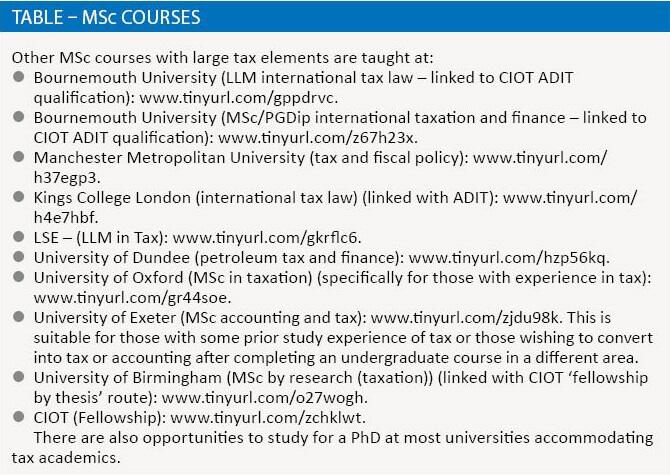

Beyond undergraduate degrees, there is a limited number of taught master’s-level programmes specialising in tax in the UK. This contrasts with continental Europe, the US and Australia where such courses are commonly available.

The full detail of what is taught in undergraduate tax degree offerings has not been examined for more than 15 years and has never been examined at master’s level study. The last study was made by this author and John Craner of the University of Warwick.

As part of the same series of articles, Angharad Miller (Bournemouth University) and Christine Woods published what I believe was the last significant study of UK employer needs of graduates in tax. Perhaps it is time to revisit both these areas, given all the changes that have occurred since?

Universities are now more open than ever to engage with employers to think about how, together, they can improve the offering to the next generation of students. The role to which degree apprenticeships may play in this field is yet to be explored. Research into how greater use of internships and longer placements in tax may be of use to all parties is under-developed, despite compelling evidence for their use in other professions.

It may be that a university education is of value to an aspiring tax professional or to one mid-career who is professionally qualified but wishes to study their subject more deeply. However, the evidence for this ought to be reviewed. Although some exciting new opportunities are becoming available, for example with new master’s-level courses coming to the market, further research would help clarify what the right link should be between universities and the tax profession across all levels of study. In the UK we remain some way behind the range and scale of offerings that those in the rest of Europe, in North America and in Australia benefit where better links are in place. This does suggest the UK is missing opportunities others are benefiting from.

UK universities are experiencing significant change and this requires the tax profession – and those advising the next generation of employees – to continually rethink the transition paths. Universities are re-examining their roles in this process and need help to balance the pressures they are under from other directions to develop their offerings. They are now more open to employer advice and suggestions than in the past as they look to reshape their programmes to keep what is good from historical approaches to educating students and develop what is needed for the future.

Further information

Read more about PhDs in tax.