The moral compass

Share this article

Chris Davidson examines the role of the tax adviser in a changing world in his address to the Confédération Fiscale Européenne 8th European Conference on Tax Advisers’ Professional Affairs

Key Points

What is the issue?

What is the role of the tax adviser? Is it just advising clients and protecting them from tax authorities?

What does it mean to me?

A responsible tax adviser should be willing to play my part in helping to balance the legitimate rights of governments, clients and taxpayers in general.

What can I take away?

Tax advisers should be full players in the tax debate, with responsibilities to our profession and to society generally, as well as to our clients.

The role of tax advisers has been under scrutiny in the UK, along with public, press and political interest in the tax affairs of multinational businesses (the BEPS agenda being the response) and rich individuals (reflecting developments in tax avoidance litigation). There have been some lurid revelations and some misinformation – and also criticism of taxpayers, tax advisers and tax authorities. Given that taxpayers are often willing to comply with their tax obligations as long as they have confidence that their neighbours are also compliant, this publicity risks causing serious damage to tax administration.

Misunderstandings and mistrust lead to unhelpful accusations. Last time I spoke to the CFE, we talked about the OECD tax intermediaries study. That started with the Seoul Declaration, which felt to some like a declaration of war and could scarcely be viewed as anything other than governments hurling abuse at tax advisers across a ravine. Tax intermediaries were involved, governments said, in ‘non-compliance and the promotion of unacceptable tax minimisation arrangements’.

The tax intermediaries study ended in a sensible place – the Cape Town Declaration – which concluded that governments should look at their own behaviour and focus on the relationship between taxpayer and tax inspector to change the incentives on taxpayers so they are more likely to behave in the way governments want. The enhanced relationship, later renamed co-operative compliance, was born. Under this, tax authorities needed to behave in a way that led taxpayers to conclude it was in their own self-interest to behave responsibly – I’ll come back to what responsibly means. To achieve this, tax authorities needed to base their approach on five attributes: understanding based on commercial awareness; impartiality; proportionality; openness; responsiveness. In the UK, this was implemented through a large business strategy and what is now HMRC’s Large Business Directorate, with CRMs relationship-managing business, a risk-based approach with far fewer enquiries, attempts to resolve enquiries quickly, an invitation to work in real time, and the concept of low-risk status where the tax authority trusts the business to self-risk-assess as well as self-assess, bringing issues to HMRC when dialogue is needed.

Some thought this new co-operative compliance would be bad for tax advisers. Not so – clients still need advice; we still have to provide best advice to them. As the tax intermediaries study made clear, tax systems would not work better if tax advisers did not exist; they are not the problem but part of the solution. But what was to be the role of the tax adviser in this new world? On at least one occasion, a CFE meeting debated how far tax advisers should stand behind the taxpayer, providing private advice, or stand between the taxpayer and the tax authority, protecting the taxpayer and acting as a filter. Clearly that is part of the role of the tax adviser.

The other model is an adviser as a full player in the tax debate, standing proudly in a triangle with taxpayers (our clients) and tax authorities. Playing a full part in creating a fair and efficient tax system. Sure, we have responsibilities to clients. But there are limits on those responsibilities, as we have other responsibilities too – to our profession and to society more generally.

Those responsibilities are defined in the UK by the professional bodies in Professional Conduct in Relation to Taxation, which sets out the fundamental principles that tax professionals must comply with. Only that way will tax advisers be trusted by society at large. These fundamental principles are integrity, objectivity, professional competence and due care, confidentiality, professional behaviour. (Not the same as the OECD prescription for tax authorities’ behaviour but very much in the same vein.)

So … professional responsibilities. In the UK, there has been a debate about responsible tax advice. KPMG has been supporting this debate. KPMG’s approach to tax can be summarised as ‘responsible tax; sustainable outcomes that contribute to the overall benefit of society’.

Tax is a fundamental part of our world. Without it, modern economies could not function and we would not be able to achieve the collective goods of health and welfare, security and education that we all value. It is also a subject where we face the boundary between, on the one hand, the rights and duties of individuals that we owe to each other and, on the other hand, the obligations of the state. Our purpose as tax advisers at KPMG in the UK is to help ensure these boundaries are drawn in the right place. Helping clients live up to their duty to comply with tax rules; representing their interests in a way that encourages the state to develop good tax law and administer the rules in ways that are conducive to this common good.

As the scrutiny tax has been under in the UK has shown, society needs to be able to trust that tax experts will operate in a responsible way – individually and collectively – whether in companies, advisory firms or tax authorities. That means tax experts in companies, tax experts who advise taxpayers (their clients) and tax experts who devise and deliver the tax system working in government. If we as tax experts – in whichever role we happen to occupy currently – do not work together in what is perceived to be the equitable interest of society as a whole, trust is lost, we will all face criticism, and the result is likely to be a sub-optimal tax system. There will be increased costs for taxpayers, and these will be passed on indirectly to society at large.

So tax advisers have a critical role to play in helping ensure that the tax system operates in a proper way – helping governments achieve their policy objectives fairly and efficiently; and at the same time protecting the interests of taxpayers, helping them meet their compliance obligations. All of this in an increasingly complex world. It’s a big ask!

As tax professionals, we have to recognise the consequences of not playing our full part in creating a fair and efficient tax system. This necessarily includes encouraging clients, tax authorities and legislators to recognise and respond to the implications of perceived abuses of the tax system. We can’t sit back and say that it’s someone else’s problem. We should recognise the desirability of the tax system supporting economic growth – and the right of governments to raise tax for the good of society – and the rights of individual taxpayers to manage their tax liabilities – and the need for fairness between taxpayers. There are clearly potential tensions between these principles that we all need to negotiate.

It’s for governments and lawmakers to determine tax policy. It should be for us to provide open and transparent assistance – on how policy proposals can be achieved, whether they are likely to deliver their aims in an effective manner, and what unintended consequences could arise.

It is for our clients to decide what tax planning is appropriate for them. We should provide technical advice. We should also provide our view on the acceptability of any tax planning and the risks we foresee – through potential consequent changes to the tax system as well as more direct risks for the client. Because the choices our clients make carry ethical implications, including the impact on stakeholders and society as a whole. Clients should take these into consideration – their business models can be damaged if they fail to manage risk to their reputations. Having said all this, there will inevitably be differing views on what constitute acceptable choices and, as I’ve said, it is for clients to make those choices.

But it is also for us to decide what we will and will not assist with.

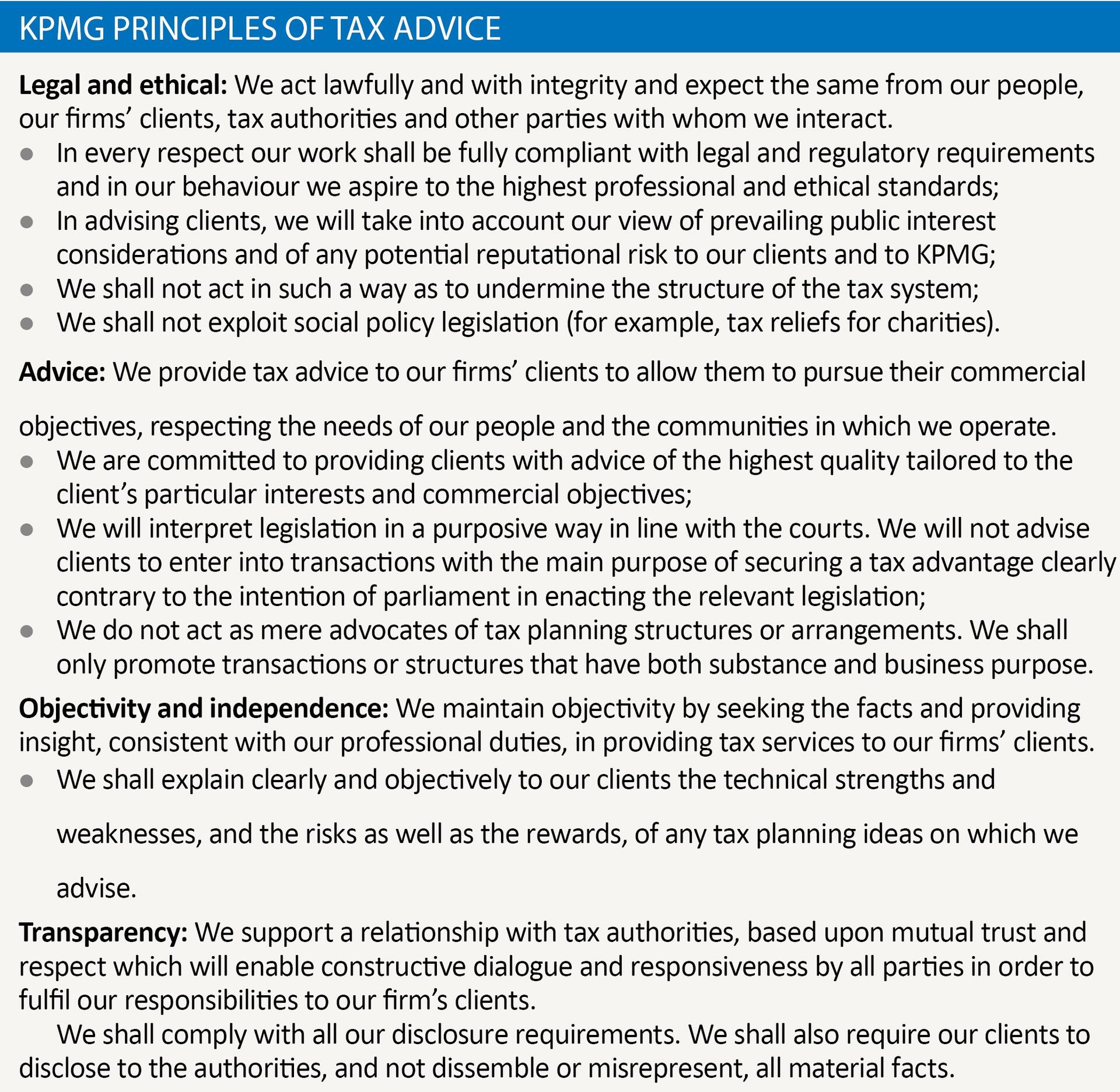

The advice KPMG UK gives clients is governed by our Principles of Tax Advice (see panel, overleaf). We will not promote or recommend planning that breaches these principles. If asked, we will provide technical advice on this sort of planning but we will make clear that we would not assist a client to implement it.

When it comes to dealings with tax authorities, we as tax advisers should be open and transparent. We should work constructively with tax authorities to enable them to do their job of administering tax effectively. At the same time, we should be firm in representing our clients’ interests, challenging tax authorities when their conduct risks undermining the fairness or effectiveness of the tax system.

So much for the theory – where is PCRT on the question of tax adviser involvement in tax avoidance? The guidance makes clear that:

- Advisers ‘must never be knowingly involved in tax evasion’ – but ‘tax planning is legal’ and ‘ultimately only the courts can determine whether a particular piece of tax planning is legally effective or not’.

- Advisers ‘should consider carefully whether the planning in question is robust, whether it could be successfully challenged by HMRC, as well as the reputational risk for the member and the client in being involved in such a transaction’.

- An adviser ‘does not have to advise on or recommend tax planning which he does not consider to be appropriate or otherwise does not align with his own business principles and ethics. However … the member may need to ensure that the advice he does not wish to give is outside the scope of his engagement’.

- Advisers ‘should ensure that the client is made aware of the risks and rewards of any planning, including that there may be adverse reputational consequences’. In particular, they ‘should warn the client of the potential risks of proceeding with a tax planning arrangement without taking full advice … or despite the advice’.

- Advisers ‘may advise on steps to manage elements of the risk … For example, the merits with client consent of a full disclosure of the arrangements to HMRC in advance of implementation even if not required by law’.

- Advisers ‘should also make an assessment of and advise the client on whether there is a sustainable filing position for tax return purposes’. The adviser ‘should not include within the tax return a claim for a tax advantage which he considers has no sustainable basis based on the information provided to him’. ‘If … information … is too complex or outside the member’s level of expertise to allow any reasonable assessment to be made, he should seek specialist support or recommend that the client obtains advice elsewhere.’

Because, as the PCRT makes clear, ‘ethical behaviour in the tax profession is critical. The work carried out by a member needs to be trusted by society at large as well as by clients and other stakeholders.’ This last point is absolutely critical.

- Why is this all so difficult? It’s hard because we have different perspectives and different expectations of the tax system. And there are different time points. And we can’t even agree on the terminology. In particular:

- What is tax avoidance has been debated for ever – and because it doesn’t adequately capture everything, we have invented new labels: aggressive tax planning, tax dodging, imbalances in the tax system, unfair outcomes and numerous other pejorative terms as well as tax planning, tax mitigation etc.

- Time points are important – and illustrate why avoidance behaviour is very different from evasion. Taxpayers have an obligation to submit a tax return and must make sure it is correct to the best of their knowledge. Putting the wrong number down on the tax return is possibly evasion but cannot be avoidance. Much earlier in time, they have the opportunity to plan their transactions to get the right number for entry on the tax return to be what they want it to be – this planning is possibly avoidance but cannot be evasion (yet). Looking at things this way shows why a lack of transparency with tax authorities is hard to reconcile with tax planning.

- Whether or not you regard planning as avoidance depends on your view of tax policy. Treasury ministers have a firm view: if someone achieves a tax advantage they disapprove of, they would see the planning as avoidance – and they might see it as avoidance even if it was the consequence of bad policy choices rather than ‘evil’ planning. At the other extreme, those with a strong interest in the rule of law might well say that the only legitimate way to establish the policy intention – the intention of parliament, not of current ministers – is to read the legislation as that is where parliament’s will is expressed: it either imposes tax or it doesn’t but there is no such thing as avoidance, either way.

- And outside commentators would have a different perspective rooted in perceptions of fairness: ‘Why don’t you pay as much tax as I think you ought to pay, given that your pockets are deeper than mine?’ This ignores the intentions of parliament and superimposes a morality that is deeply felt but a wholly unsatisfactory basis for computing tax liabilities, as shown when a company’s response to criticism was to offer a ‘voluntary’ payment of corporation tax.

Where does this leave taxpayers’ rights to privacy, to effective representation, to pay no more tax than legally owed, and to plan within the limits of the law? More transparency and hence more data available to tax authorities and more use of IT to mine that data will change the details – change what efficient tax administration looks like. But the principles don’t change. Our role should be a full one, within a triangular relationship with clients and governments, helping to make the tax system work fairly and efficiently. That is responsible tax.