Multiple completion contracts for company share buy-backs

Share this article

Purchase of own shares transactions are an important tool in succession planning. Although complex, multiple completion contracts can play a vital role in their financing, as we explore in the fictional case of Wimbledon Environmental Services Ltd.

Key Points

Key Points

What is the issue?

Financing a purchase of own shares transaction is not always easy. Company law demands that the purchase price for the shares bought back by the company is paid immediately.

What does it mean for me?

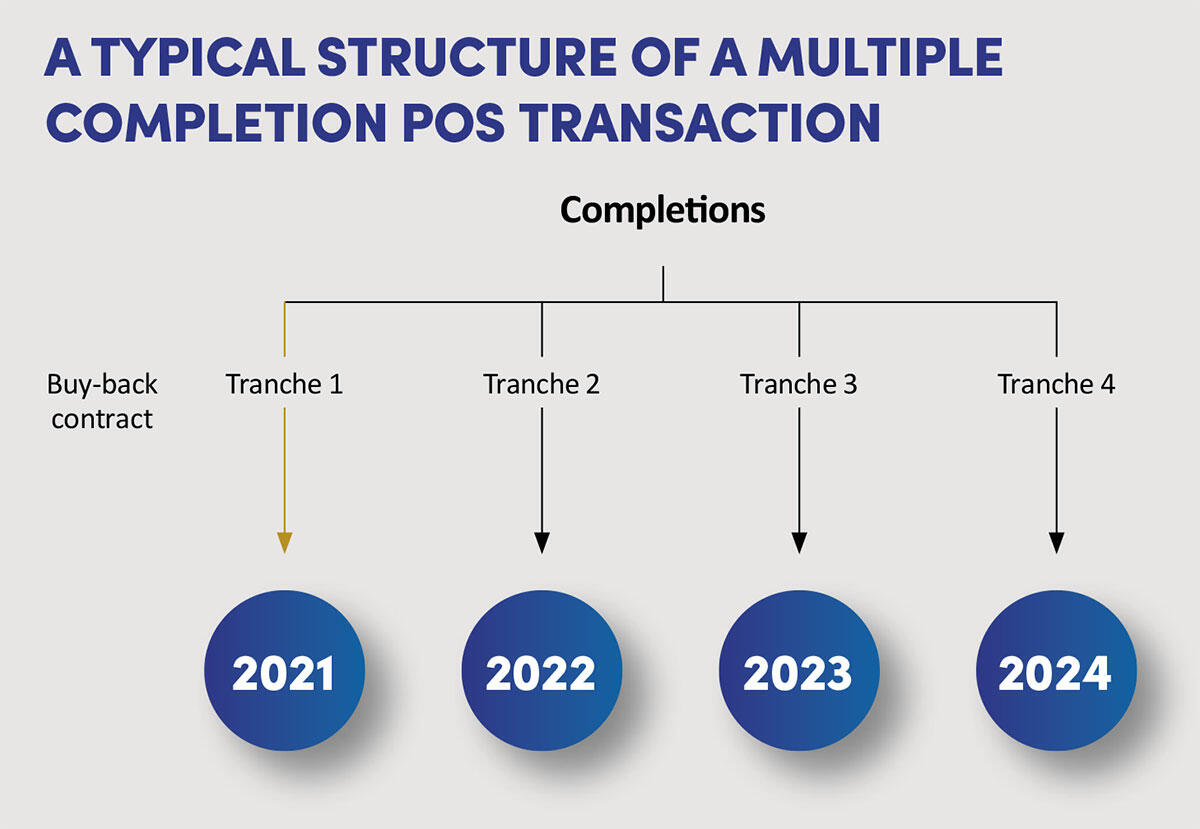

A multiple completion purchase agreement enables the exiting shareholder to enter into a contract to invariably sell all their shares back to the company, but with the legal completion of the share purchases taking place in tranches.

What can I take away?

There may be scope for adjusting the phasing of the own share purchase completions to ensure that the seller satisfies the ‘connection’ test immediately after the first tranche of shares are purchased.

Company share buy-backs are frequently used as an important tool in succession planning. Typically, the owner managers will sell all their shares back to the company under a purchase of own shares (POS) transaction, leaving the next generation and/or the senior management team in place as the new owners.

Financing a POS is not always easy. Company law demands that the purchase price for the shares bought back by the company is paid immediately (Companies Act 2006 s 691(2)). It is not therefore possible for a company to buy back its own shares for a deferred consideration. However, because of the (often) substantial sums involved for the POS consideration, the ‘multiple completion’ arrangement often comes to the rescue.

Multiple completion POS agreements

A multiple completion POS agreement enables the exiting shareholder to enter into a contract to invariably sell all their shares back to the company, but with the legal completion of the POS subsequently taking place in tranches. At each separate ‘completion’ date, the company would pay the relevant consideration, cancel the relevant tranche of shares being purchased and submit the SH03 form to the Registrar of Companies. The POS 0.5% stamp duty charge would only be payable on the tranche being brought.

It is accepted that the purchasing company only requires enough distributable profits to complete the relevant tranche of shares being purchased (i.e. it does not need to have all the distributable profits for all the relevant POS completions). The vast majority of corporate lawyers seem to accept that it is lawful to purchase shares under a multiple completion deal but there are some dissenters.

A multiple completion arrangement enables the company to finance the purchase price over a number of years out of its (surplus) trading cash flows. Provided the contract is properly structured and implemented, this mimics a ‘deferred consideration’ deal, whilst remaining compliant with company law.

By way of contrast, as the seller will normally prefer ‘capital gains’ treatment on the sale of their shares, the financing issue cannot normally be solved by arranging for the seller to loan back all or part of the purchase consideration. This will usually make the seller ‘connected’ under the Corporation Tax Act 2010 ss 1042(1) and 1062(2)(b). This is because they will invariably have more than 30% of the combined share and loan capital of the company immediately after the POS. (Unless otherwise stated, all legislative references in this article are to Corporation Tax Act 2010.)

Image

HMRC’s existing approach to the connection test

HMRC has generally been comfortable with multiple completion contracts and granted POS clearances under s 1044 (and Income Tax Act 2007 s 701). Nevertheless, HMRC has stressed that it has always taken the view that the word ‘possesses’ in s 1062(2) refers to legal rather than beneficial ownership. This is emphasised in HMRC’s Capital Gains Manual at CG58655. This effectively trumps the provision in s 1048(3), which indicates that the references in ss 1033 to 1047 refer to beneficial ownership.

HMRC told the CIOT that it appears to have overlooked the ‘possession’ of issued share capital limb of s 1062(2) when granting a number of recent POS clearance applications under s 1044. This is likely to have resulted in POS clearances being granted where the seller was still connected with the company by virtue of retaining legal ownership of more than 30% of the issued share capital immediately after the POS contract was executed. Wide-ranging experience suggests this was the case.

However, a particular difficulty that we often experienced was HMRC's view that it was not possible (under company law) to nullify the voting rights attached to the remaining shares. HMRC still held this opinion where there was a specific prohibition on voting in the POS contract. Consequently, where the selling shareholder, together with their associates (which notably excludes adult children for this purpose), still held more than 30% of the voting rights immediately after the POS contract was executed, HMRC would indicate that the seller was connected with the company under ss 1042 and 1062(c). Nevertheless, HMRC would be prepared to grant clearance provided that the remaining tranches of shares (awaiting purchase) were converted to non-voting shares. The seller was therefore able to enjoy the (usually) beneficial capital gains (i.e. no distribution) treatment. (All the other conditions in ss 1033 to 1048 would also need to be satisfied.)

HMRC’s current approach

In recent years, tax advisers generally approached multiple completion POS transactions with some confidence that they were effectively ‘blessed’ by HMRC.

However, I have received many calls from CIOT members and accountants indicating that HMRC is now refusing clearances in cases where the seller retains more than 30% of the company’s issued ordinary share capital after the multiple completion contract is made. HMRC has recently confirmed to us that this does not represent a new interpretation of the word ‘possesses’ – simply that HMRC has not always correctly applied the strict law relating to the ‘connection test’.

As already stated, HMRC has emphasised to us that ‘possesses’ refers to legal ownership (i.e. holding the shares remaining to be purchased), rather than beneficial ownership. Put simply, where the seller has legal ownership of more than 30% of the issued ordinary shares after the first POS has been completed, the transaction will not satisfy the strict requirements of s 1062(2). In some cases, it may be possible to tweak the transaction to comply with this test, as shown in the example below.

HMRC has confirmed that it is now looking to rectify this recent oversight and will make sure that the wording of s 1062(2)(a) is properly taken into account when applying the connection test. For the avoidance of doubt, HMRC will not disturb clearances that have already been issued but will apply the above approach to any fresh POS clearance applications.

Notwithstanding HMRC’s application of the ‘30% plus issued share capital’ connection test, it is generally recommended that all steps are taken to deprive the seller of beneficial ownership (such as converting the relevant shares to non-voting shares) on day 1. This will provide certainty about the capital gains tax disposal date and, where appropriate, ensure that a valid business asset disposal relief claim can be made.

Image

Capital gains tax disposal date

The analysis of the capital gains tax disposal date for multiple-completion POS agreements has previously been the subject of some debate. The accepted view now is that the normal rule in Taxation of Chargeable Gains Act 1992 s 28 cannot apply. This is because s 28 requires an acquisition of shares; and Finance Act 2003 s 195 specifically deems that when a company executes a POS there is no acquisition of shares (even where the shares are placed in ‘Treasury’). Nevertheless, under general capital gains tax principles, the disposal of all the shares occurs when beneficial ownership of the shares is lost. This will usually be when the POS contract is executed.

Thus, provided the relevant business asset disposal relief conditions are satisfied throughout the two years before the disposal date, the selling shareholder should be able to access the 10% capital gains tax rate (up to the £1 million lifetime gains limit). Of course, it will be appreciated that the seller must usually have held the shares for five years to bring the POS within the ‘capital gains’ regime (s 1035).

The way forward

It is unfortunate that HMRC’s current application of the ‘connection test’ is likely to frustrate many legitimate multiple completion POS agreements, which seek to obtain capital gains treatment. There would, of course, be no problem in the rare cases where the exiting shareholder requires the ‘default’ distribution treatment.

In some cases, there may be scope for adjusting the phasing of the POS completions to ensure that the seller satisfies the ‘connection’ test immediately after the first tranche of shares are purchased.

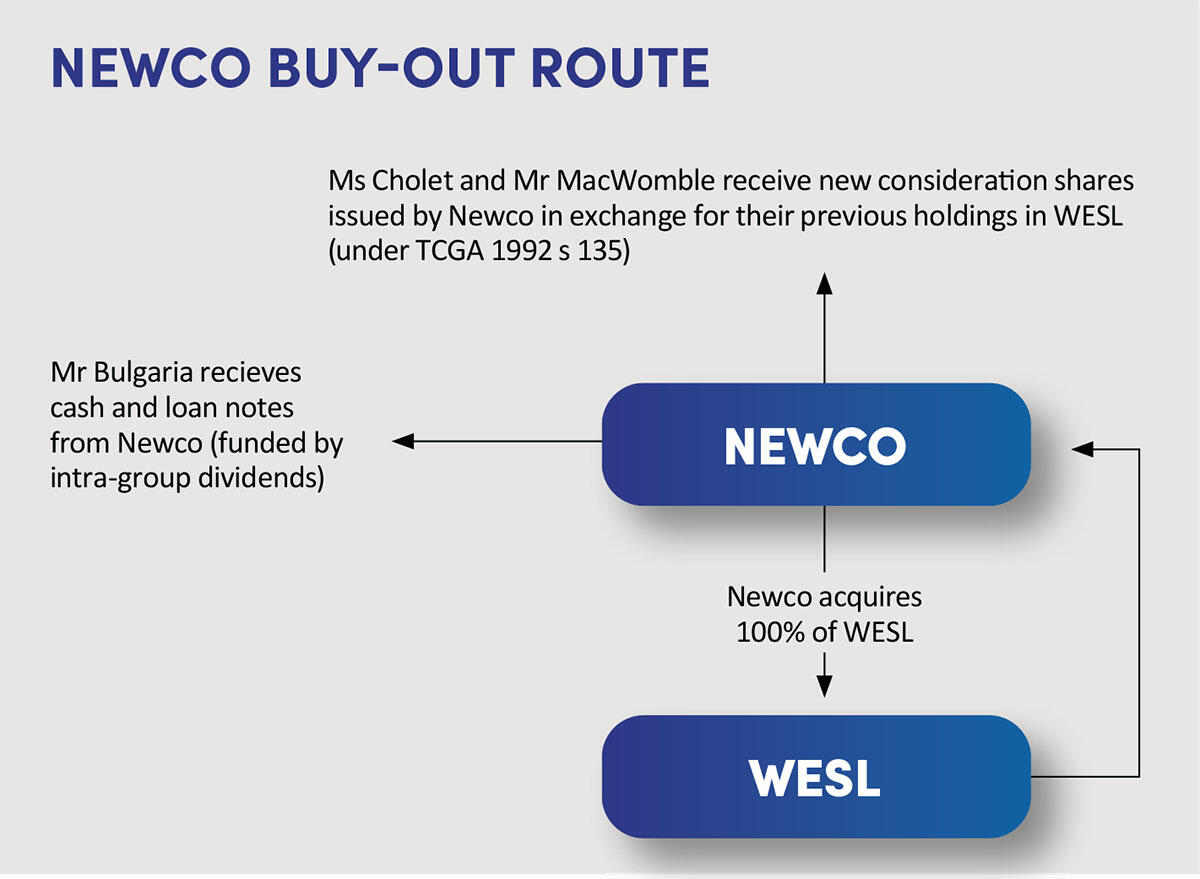

However, if this is not possible, tax advisers will probably need to use a ‘Newco buy-out’ structure to acquire the outgoing shareholder’s shares. This will typically involve using a new company (‘Newco’) as the acquisition vehicle to buy-out the shares of the departing shareholder – with cash and/or loan note consideration. The ‘continuing’ shareholders would ‘swap’ their shares under the share exchange rules in Taxation of Chargeable Gains Act 1992 s 135.

A typical Newco buy-out structure that might be implemented (as an alternative to the proposed POS) in the Wimbledon Environmental Services Ltd example is shown above.

This buy-out structure is not ideal, since it involves the creation of an additional company (Newco), increased stamp duty charge (reflecting the value of WESL) and so on. On the other hand, it is possible for Newco to issue loan notes for the deferred consideration. These loan notes could be secured by a charge over the business’s assets, which is likely be attractive to the seller.

The CIOT acknowledges the problems for multiple completion POS agreements that are likely to be created by HMRC’s recently confirmed approach on the ‘connection’ test. We shall continue to work with HMRC to see whether a solution can be found on this issue.