Negotiating the minefield

Share this article

Lydia Challen explores the challenges facing the corporate tax function

Key Points

What is the issue?

The role of the tax function is changing within big businesses

What does it mean to me?

Going forward tax teams will need to take on increasing levels of responsibility for strategically important and potentially high profile decisions

What can I take away?

Now is the time to start preparing for BEPS, it’s going to be an enormous challenge for businesses and it is important to engage early with governments, national tax authorities and key advisers

Gone are the days of tax directors resigning themselves to a job in the shadows. Never has tax been as high profile and, as a result, the role of the tax function is increasingly complicated.

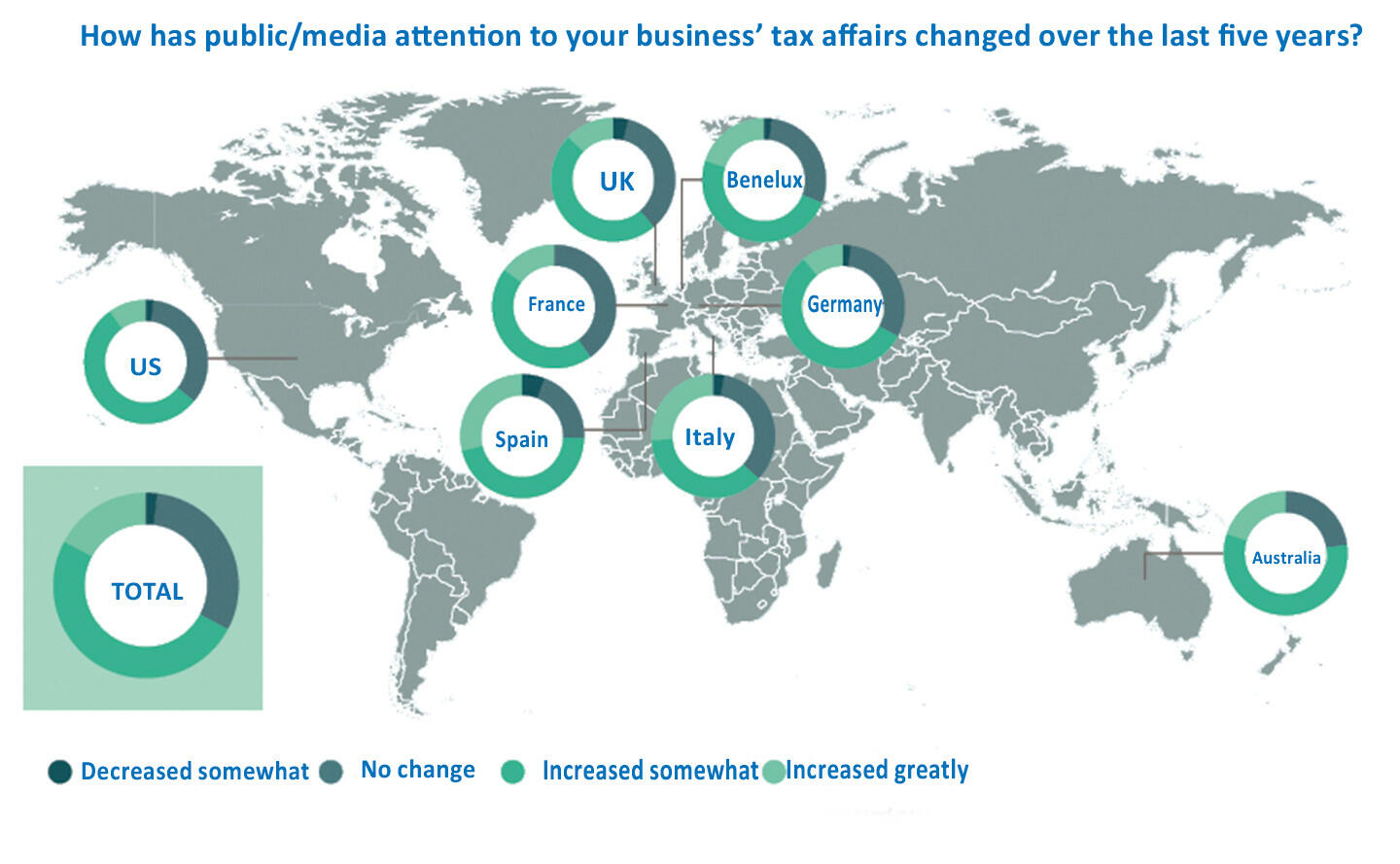

Today’s tax teams have to balance often competing interests, notably continued investor demands for greater financial returns against the reality that the tax authorities are adopting more aggressive ways to collect revenue. On top of that, even conventional tax planning may carry potential reputational risk, given the media and public interest in multinational businesses paying their ‘fair share’ as illustrated in the Table. The court of public opinion is not a particularly impartial – or even informed tribunal.

Table – Public/Media perception of corporate taxation

Add to that the uncertainties about what the international tax landscape will look like in a few years and increases in the compliance burdens faced by businesses, and one can see that the job of the tax director is not an easy one.

To understand the challenges facing tax teams in corporates around the world, Allen & Overy commissioned research examining the views and experiences of 350 senior executives – CEOs, CFOs, general counsel, tax directors and heads of audit committees – from a range of industries in western Europe, the US and Australia.

We know that tax has moved up the corporate agenda. The need for strategic thinking reflects its growing importance as a component of the overall corporate strategy. Some 59% of respondents said tax was ‘very important’ with 13% believing it to be ‘of the highest importance’ in terms of the overall corporate strategy. This contrasts with five years ago when 22% said it was ‘very important’.

As well as this, and a further reflection of the growing importance of tax, is that we can see how boardroom understanding of tax as an issue has considerably improved in the past five years. Some 71% of respondents said tax issues were now included as part of the overall business strategy; and 59% said tax was becoming more of a consideration when enforcing the reputation management strategy.

When asked about strategy, we found:

- 77% of respondents felt that investor influence on tax decisions had increased over the past five years;

- 72% said their approach to tax planning sometimes, or often, conflicted with tax authorities ideals; and

- 66% said the key objective for the tax function was to achieve the lowest effective tax rate (ETR).

This can be compared with what we found in relation to the changed role of the tax function:

- 88% of respondents said the board’s expectations of a tax director’s role had changed over the past five years; 26% said to a great extent;

- 59% said tax had become very important to the firm’s overall strategy, compared with 22% five years ago; and

- 69% noted that expectations of the tax director’s role had evolved towards being more strategic.

It is clear that the external influences are having an impact on the nature of tax teams and on how they are perceived within the business. From our own experience with clients we know that if the tax function is to operate at its best, good communication between the board and the tax director is key. Explaining complex tax issues in straightforward terms is an increasingly important skill for tax specialists. Conversely, boards need to give tax the time and attention that such a key strategic issue deserves.

However, assuming this new position and taking on this new responsibility will often be more difficult than it sounds, demonstrated by the fact that 21% of respondents lacked confidence in their abilities to manage and avoid tax risks. We think there are several reasons for this, ranging from the waves of new compliance work coming down the line to the potentially high-profile results of a misjudged tax strategy. Although the circumstances will vary between companies, the research highlighted four keys areas on which those with tax responsibility could focus:

- When pursuing the lowest ETR, boards need to consider how that will be interpreted by tax authorities, governments, NGOs, politicians, consumers and the media. This has to be assessed not just from the perspective of where the company is based, but in all the jurisdictions in which it operates. For example, numerous US-based multinationals facing high tax rates at home have faced negative publicity due to tax-avoidance strategies pursued elsewhere to reduce their overall ETR.

- Communication is key. There have been significant improvements in communication between the board and the head of tax. That should be maintained even if the issue of tax eventually fades from the headlines. Communication with investors and wider stakeholders will help to manage expectations about what the tax strategy can deliver.

- Brace for BEPS. This important OECD-led project due to be implemented in 2016 is yet another source of compliance work for corporate tax departments and will bolster an already considerable workload. Heads of tax are naturally preoccupied with the uncertainties BEPS brings, such as how individual countries will interpret the rules, cross-border implications and whether their firms will be winners or losers. This calls for engagement with governments and national tax authorities to encourage international consistency in the rules.

- Corporate strategy should be evaluated in view of its tax consequences to avoid unnecessary unforeseen costs later. This entails ensuring that the head of tax is fully aware of, and involved in, the board’s plans for the company. Equally, proposals for tax-driven transactions should be carefully analysed, within and outside the tax function, to identify downside risks or bear traps that may impede subsequent commercial activity.

Further information

A copy of the full report can be read here.