A new category

Share this article

Neil Warren shares his thoughts in a question and answer article on the introduction of a new category for ‘limited cost traders’ who will use a rate of 16.5% from 1 April 2017

Key Points

What is the issue?

The new limited cost trader category being introduced on 1 April 2017 will affect an estimated 123,000 VAT registered businesses in the UK. So the new rules will need to be fully understood by advisers and clients so that action can be taken as necessary.

What does it mean to me?

The 16.5% category will apply to any scheme user that spends less than 2% of its gross sales on goods or less than £250 in a VAT quarter. There are specific exclusions in the definition of goods that need to be recognised. All scheme users who are limited cost traders will pay more tax because the highest existing rate for any category is 14.5%.

What can I take away?

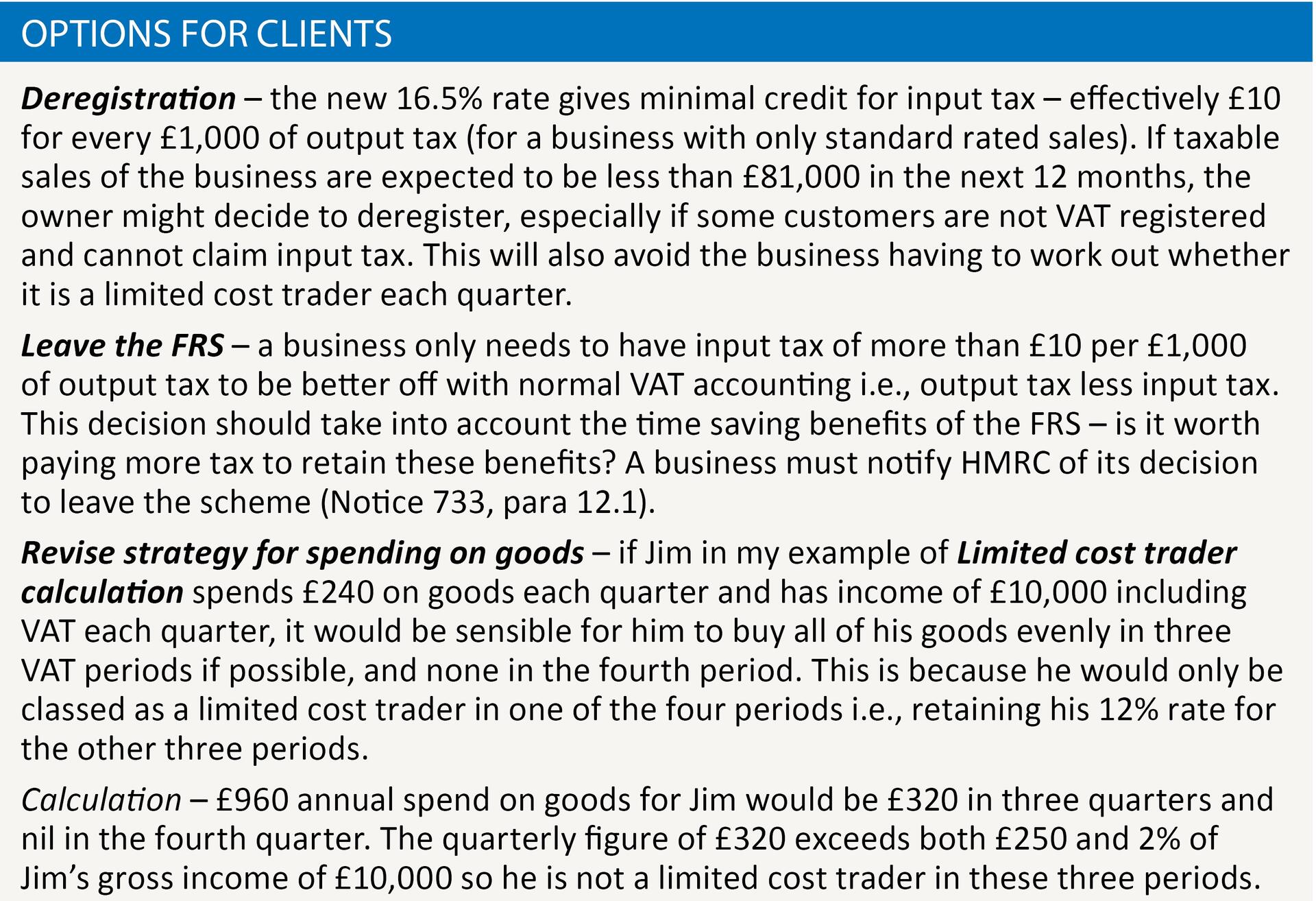

The loss of tax savings for existing scheme users might mean it is better for the business to either deregister or revert to normal VAT accounting when the new rules are introduced.

The flat rate scheme (FRS) has been an important part of the VAT system since April 2002, and has saved thousands of pounds of tax for many SMEs compared to normal VAT accounting. It has also simplified accounting systems and therefore saved time and money for users, and reduced the risk of VAT errors being made. But that outcome will change on 1 April because an estimated 123,000 out of 411,000 existing scheme users will be classed as limited cost traders and will need to account for VAT of 16.5% on their gross business income rather than 12% or 14% as they do with current arrangements in most cases. The aim of the new rate is to supposedly tackle aggressive abuse of the scheme by labour-only agency workers but it will affect all users who have low spending on goods i.e., including the honest traders. The impact of the proposed changes will need to be considered by advisers on a business by business basis, and I will analyse the key issues in this article.

How does the FRS work?

To set the scene, the FRS means that a business never claims input tax unless an expense relates to capital goods costing more than £2,000 including VAT. A newly registered business can also claim input tax on pre-registration expenses in the same way as a non-scheme user if it uses the FRS for its first VAT period.

The VAT payable is based on a flat rate percentage being applied to gross business income (but not outside the scope income), with the relevant rate depending on its trading activity.

There are 55 different categories, including two 12% sweep up categories for ‘any other activity that is not listed elsewhere’ and ‘business services that are not listed elsewhere’.

These categories are relevant for a business that does not have an exact DNA match with any of the other categories.

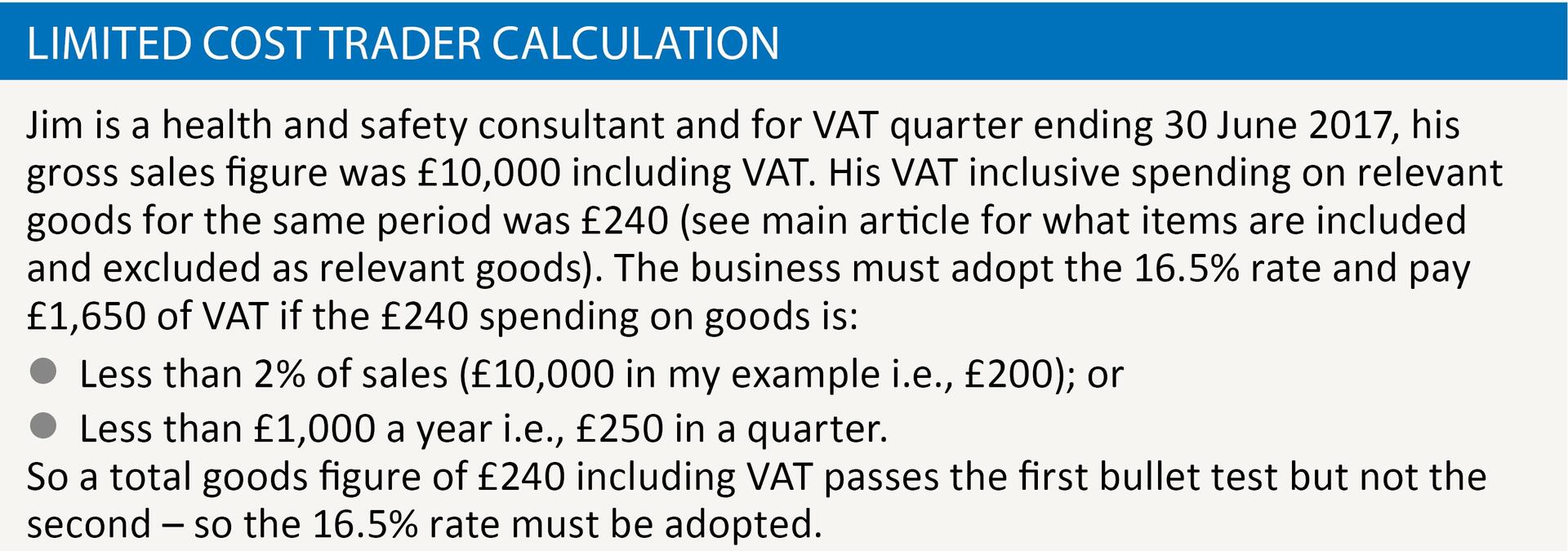

Case study: what is a limited cost trader?

Jim is a health and safety consultant who uses the FRS category of 12% for ‘business services that are not listed elsewhere’. This is correct because there is no specific category for health and safety consultants.

With effect from 1 April 2017, Jim will need to consider if he is a limited cost trader on each occasion that he completes a VAT return. Here is a summary of the new rules:

- Jim must calculate his VAT inclusive spending on ‘relevant goods’ for the quarter including VAT. The phrase ‘relevant goods’ excludes vehicles, road fuel and motor parts, as well as food, drink and capital items. Supplies of gas and electricity are included in the calculations because they are goods, whereas rent, telephone and Internet charges are services, and so are excluded. As an extra twist, the draft legislation confirms that only expenses that are wholly business are included in the calculations. This means, for example, that a gas or electricity bill with part business and part private use must be excluded completely.

- Note – if Jim operated a transport business, using the FRS category for ‘Transport or storage, including couriers, freight, removals and taxis’, he would be able to include spending on vehicles, road fuel and motor parts in his calculations as long as he owns or leases a vehicle in his business.

- Jim must check if the amount spent on goods is either less than £250 for the quarter (£1,000 is the annual figure in the draft legislation and would be relevant if a business uses the annual accounting scheme) or less than 2% of his VAT inclusive sales for the same period. If the answer is ‘yes’ to either of these two tests, he must adopt the 16.5% category as a limited cost trader. If the answer to both tests is ‘no’, he will adopt his 12% rate in the usual way.

- See Limited cost trader calculation

What are the impacts of the proposed changes?

HMRC issued a policy paper on 23 November 2016 titled ‘VAT: tackling aggressive abuse of the Flat Rate Scheme’. This paper recognises that ‘the new 16.5% rate will remove the cash advantage for those businesses with limited costs’, i.e. all businesses are affected and not just the supposed tax avoiders. It also revealed some interesting statistics:

- The new limited cost trader category will increase the annual tax yield by £130m.

- Two thirds of FRS users are registered for VAT on a voluntary basis (annual taxable sales are less than £83,000) and HMRC anticipate that the new category will mean that ‘many of them may decide to deregister’

- The limited credit for input tax that is evident with the 16.5% rate means that an estimated 4,000 FRS users will revert to normal VAT accounting, i.e., output tax less input tax.

- HMRC quote an average figure of £390 in cost savings for a business that chooses to deregister after 1 April 2017.

So to summarise the above facts, advisers will be faced with three main choices when considering the impact of the new rules – see Options for clients.

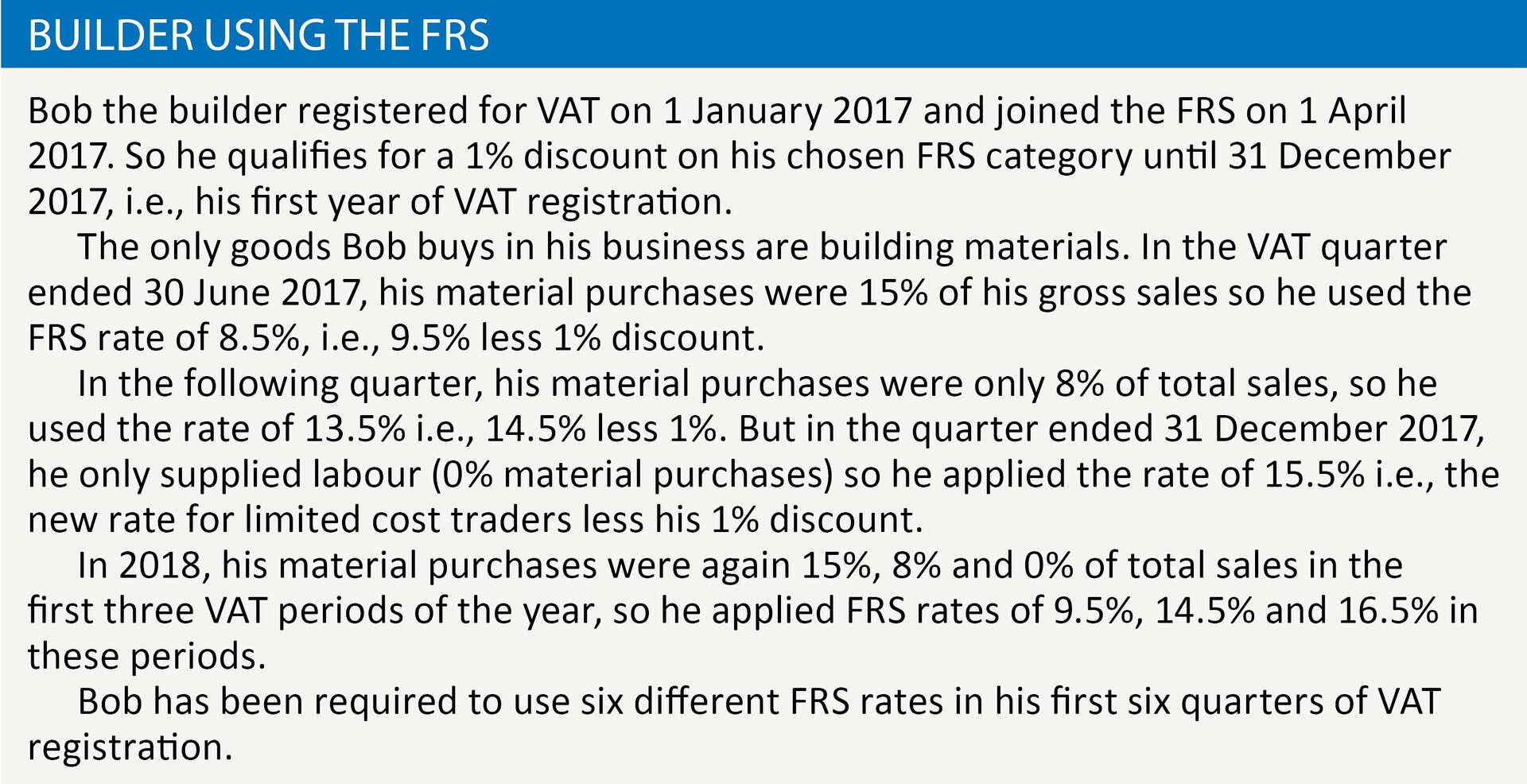

How will the new rules affect builders?

Everyone agrees that the new 16.5% category will not assist the ‘simplification’ aims of the FRS but it will be even more complicated for builders because the FRS already has a ‘goods’ twist (or building materials to be precise). If a builder spends more than 10% of his gross turnover on materials, he can use a lower FRS rate of 9.5%. If the material purchases are less than this figure, the FRS rate is 14.5%.

The new 16.5% rate means that if the material purchases (plus spending on other goods) are also less than 2% of total sales or more than 2% of total sales but less than £1,000 a year, the builder must apply the 16.5% rate. A newly VAT registered builder will also get a 1% discount on his relevant category in his first year of registration, so he might end up with one of six different FRS rates. See Builder using the FRS.

Conclusion

This article is based on the draft secondary legislation published on 5 December 2016 – HMRC confirmed an eight-week period from this date for affected businesses to make comments. So it is possible that the draft Statutory Instrument might be amended.

HMRC have confirmed that an online tool will enable current and prospective FRS users to determine whether they are limited cost traders, which is very welcome. But I suspect that most users will either deregister or revert to normal VAT accounting.