Not so simple

Share this article

The flat rate scheme is intended to simplify VAT returns for a small business with annual taxable sales of less than £150,000, but it has many complicated issues which are considered by Neil Warren in this Q&A article.

Key Points

What is the issue?

There are many potential pitfalls with the FRS which can result in errors on VAT returns if the various quirks are not understood. For example, input tax can only be claimed on capital goods costing more than £2,000 and not capital services such as the cost of building an extension to business premises.

What does it mean to me?

Advisers often assume that many income sources for a business can be excluded from the scheme, e.g. buy to let rental income or the proceeds from selling a car. This is not correct and it has a very wide application.

What can I take away?

Always be clear that HMRC view the scheme as a time rather than tax saver. So any requests to backdate an application to join the scheme will be refused if a business has already submitted its VAT return for a period.

I have a client who is eligible to join the scheme and will save a lot of tax compared to normal VAT accounting. He has asked if he can backdate his entry to create an extra tax windfall. Is this allowed?

Unfortunately, HMRC do not recognise the FRS as a tax saver, only as a time saver, i.e. to make the VAT return process easier for a small business. Their policy is that once a VAT return has been submitted, it is impossible to save time, so they will refuse any request to backdate the application. However, a retrospective request will usually be granted if returns are outstanding for earlier periods. This could be the case if a business is behind with its returns or is late registering for VAT, so has to complete a long period return. The reason that HMRC have strong powers is because the legislation only allows a taxpayer to join the scheme at an earlier date ‘as may be agreed between him and the Commissioners.’ (1995 VAT Regulations, SI1995/2518, Reg 55B).

Case law – in the recent First-tier Tribunal (FTT) case of Julian Goodman (TC4827), the tribunal supported HMRC’s decision to refuse the taxpayer’s request to backdate his joining date by two years in order to produce a VAT windfall of £7,500.

It seems unfair that a business has to include zero-rated and exempt income in the calculations, when no tax is collected from customers on these sales. Why is this the case?

The scheme percentages in the legislation take into account two important factors:

- The average input tax sacrificed by a scheme user – this is why, for example, a pub has a lower FRS percentage than an accountant (6.5% versus 14.5%).

- The fact that some businesses have more zero-rated and exempt sales than others – which is why the lowest of all categories is for a business involved in ‘retailing food, confectionary, tobacco, newspapers or children’s clothing’ (4%).

In practice, some businesses will pay more tax by adopting the scheme, and others less, compared to normal VAT accounting.

I understand that a quirk of the scheme is that buy-to-let property income is included in the calculations and also the sale of a business motor car. Is that correct?

Rental income earned from residential property is always exempt from VAT (unless it relates to holiday lettings which are standard rated). And income earned from land or buildings is always classed as ‘business’ in accordance with EU Law (‘economic activity’ is the EU word for ‘business’):

Article 9 – Directive 2006/112 – ‘The exploitation of tangible or intangible property for the purposes of obtaining income therefrom on a continuing basis shall in particular be regarded as an economic activity.’

However, if the property is in a different legal entity to the VAT registered business, there is no FRS tax to declare on the rental income. And don’t forget that jointly owned property is always classed as a partnership (HMRC Notice 742, para 7.2).

The car sale is a ‘loser’ because the gross receipts must be included in the FRS calculations.

So what income is excluded from the scheme?

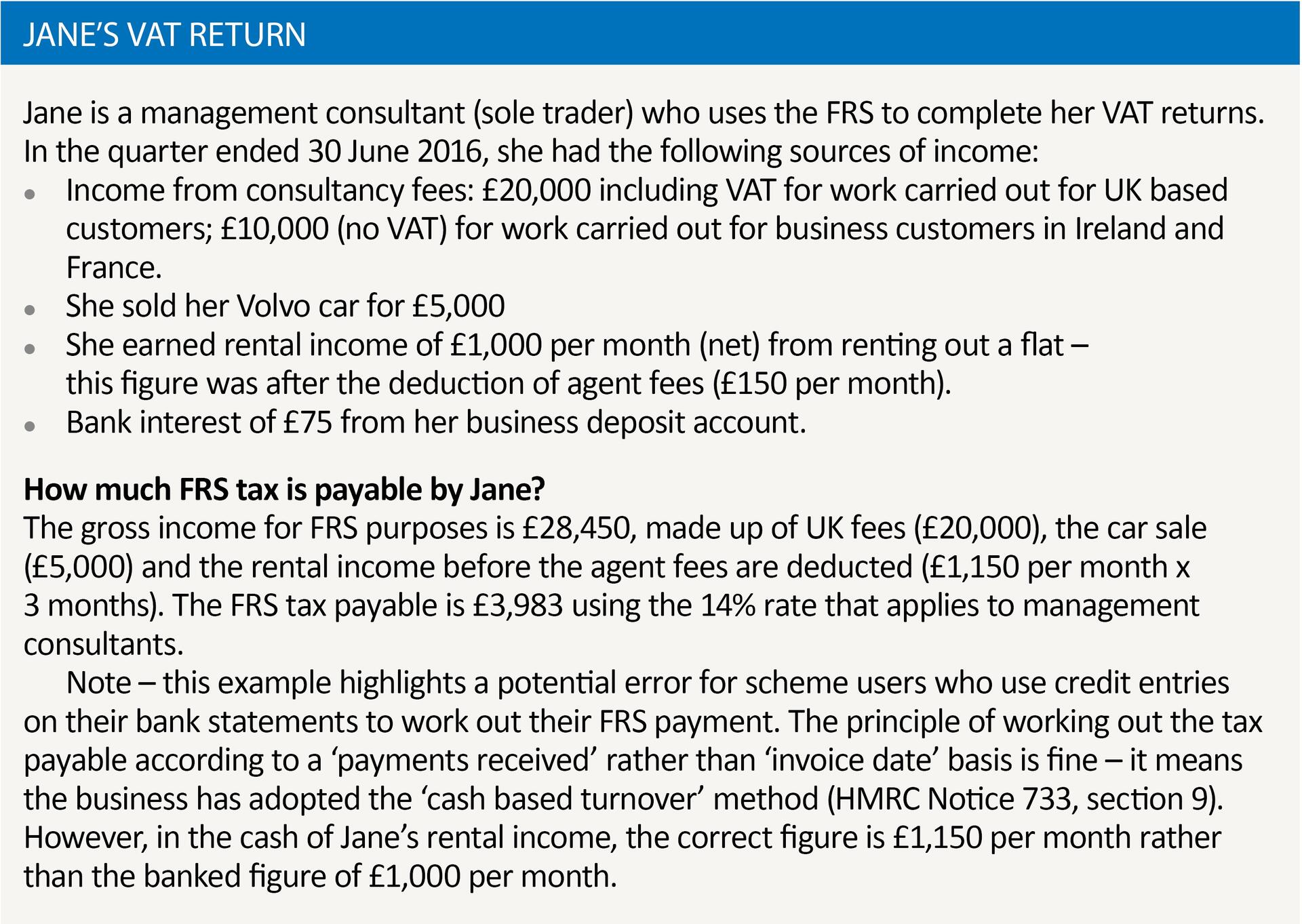

If a business has income that is outside the scope of VAT, then it is completely excluded from the FRS calculations, including Box 6 of the VAT returns (outputs box). This is good news for a business that provides services to overseas business customers, where the place of supply is the customer’s country in most cases under the general B2B rule. A business can also ignore bank interest earned in a business bank account because this income is classed as non-business (HMRC Notice 733, para 6.3). See Jane’s VAT return.

I am concerned that if a client chooses a category that HMRC disagrees with, an officer could go back and retrospectively assess tax for the last four years if HMRC’s choice has a higher percentage. Is this correct?

HMRC’s published guidance clearly states that an officer will not take retrospective action if the taxpayer has made a ‘reasonable choice’ of category (HMRC Notice 733, para 4.2). What does this mean in practice? An obvious example of an unreasonable choice would be a lawyer who chooses the category for a hairdresser or a builder who describes himself as a food retailer. The challenge is to keep a clear written record as to why a particular category was chosen at the time of joining the scheme.

On 4 May 2016, HMRC issued a revised Notice 733 in relation to the FRS, and the amendments are very welcome in section 4 (compared to the previous version of the notice) in confirming that HMRC’s views on FRS categories that apply to various businesses do not have the force of law. The notice states that a business should ‘use ordinary English’ in choosing its flat rate category, and confirms that ‘HMRC have offered an interpretation of each sector’ in their guidance (para 4.1). The revised notice has also removed the previous para 4.4, which indicated that all consultants should choose the category for ‘management consultants’ (14%) even if they did not ‘fit the traditional idea of management consultant’ and also excludes their view that engineering consultants and designers should always choose the category for ‘architect, civil and structural engineer or surveyor’ at 14.5%. This was the key outcome in the FTT cases of SLL Subsea Engineering Ltd (TC4256) and Idess Ltd (TC3638) where the courts concluded that ‘mechanical engineers’ were not ‘civil engineers’ because the latter work on land related projects whereas mechanical engineers work on plant and machinery. Mechanical engineers were therefore correct to choose the ‘business services not listed elsewhere’ category at 12% because there is no specific category for their business.

The starting point for a business adopting the FRS for the first time, and choosing its category, is to use the list of categories in the 1995 VAT Regulations, SI1995/2518, Reg 55K, which can be found with a direct link from para 4.3 of the revised notice. In areas of doubt (eg where there is no specific category for the business description) HMRC offer assistance in their guidance notes FRS7200 and FRS7300 (a link is given in para 4.1) which now reflect recent court cases.

What input tax can I claim if I use the scheme?

The basic principle of the FRS is that no input tax can be claimed because the relevant FRS percentages reflect the average input tax sacrificed by a business in its relevant category. However, there are three situations when a claim can be made:

- Pre-registration input tax. A scheme user can claim pre-registration input tax on its first VAT return on the same basis as a non-scheme user ie in relation to services purchased in the six month period before the date of registration and up to four years in the case of goods. This is good news because a scheme user also benefits from an extra 1% discount to the usual scheme percentages in its first year of VAT registration.

Note – it is important to be clear that the 1% discount only applies in the first 12 months of VAT registration and not the first 12 months that a business adopts the scheme. So if a business registered for VAT on 1 January 2016 and joined the FRS on 1 July 2016, it would only benefit from the 1% discount until 31 December 2016.

- Capital goods costing more than £2,000 including VAT. As an example, if a scheme user buys a van for £5,000 plus VAT, he can claim input tax. However, be aware that a claim must relate to capital goods and not capital services. I came across a recent situation where a hairdresser using the FRS claimed input tax on the cost of a salon refurbishment. This expenditure related to ‘construction services’, apart from one or two items such as hair drying equipment, which could not be claimed anyway because the total cost was less than £2,000.

- Post-deregistration expenses. A business that deregisters is deemed to leave the scheme on the day before it deregisters. This means that output tax must be accounted for on any business sales made on the final date of registration and therefore any standard rated stock or assets where input tax was claimed and the total value of the assets exceeds £5,000. It also means that input tax can be claimed on any expenditure incurred on the final day, and also on post deregistration expenses (eg input tax on services invoiced after a business has deregistered but relevant to the period it was registered, such as accountancy fees). A claim is made on form VAT427.

I understand there is a tax windfall with the scheme if I incur a bad debt. What is this all about?

This is correct:

For example, a management consultant raised an invoice for £3,000 + VAT to a UK customer, which was never paid and is now a bad debt that he has written off in his accounts. Even though he has not declared any FRS tax on this sale because he uses the cash based turnover method, he can claim a VAT windfall once the debt is more than six months overdue for payment (the usual bad debt relief period) as follows:

VAT that would have been paid by the customer = £600; less VAT that he would have paid using the FRS i.e. £3,600 x 14% = £504; Total to claim in Box 4 of his relevant VAT return = £96.

If he accounted for tax on an invoice basis (so would have paid £504 of VAT on an earlier return), his bad debt relief claim will be £600 ie producing a net gain of £96 in both cases. (HMRC Notice 733, section 14).