Nowhere to hide?

Share this article

Harriet Brown considers the uncertainties that an HMRC discovery assessment can cause

Key Points

What is the issue?

Is there anything a taxpayer can do in the face of a discovery assessment and what recent

cases tell us about that

What does it mean to me?

How to approach dealing with a discovery and how this differs from that to take in an enquiry

What can I take away?

Some positive points about prospects of successfully challenging an HMRC discovery assessment

Discovery assessments – under s 29 of the Taxes Management Act 1970 (TMA 1970) – are a perennial concern for tax advisers and taxpayers alike. HMRC has two primary ways to challenge a taxpayer’s return. First, it can enquire into an individual taxpayer’s return under s 9A TMA 1970. They may do so only ‘up to the end of the period of 12 months after the day on which the return was delivered’, assuming it arrived on time. Thus, the period for an enquiry to be opened is quite short.

The other option is a discovery assessment. The period in which this can be made is much longer. The limits for making an assessment are set out in s 34 and s 36 TMA 1970. In the first instance, this is four years after the end of the year of assessment to which it relates; in the second it is six years after the end of the year of assessment if careless behaviour caused the tax loss and 20 years after the end of the year of assessment if deliberate behaviour caused it. Thus discovery assessment vastly extends the timescale in which an enquiry can be brought. This reduces the certainty for a taxpayer who cannot, on the ending of the period in which an enquiry can be made, rely on their tax return being final.

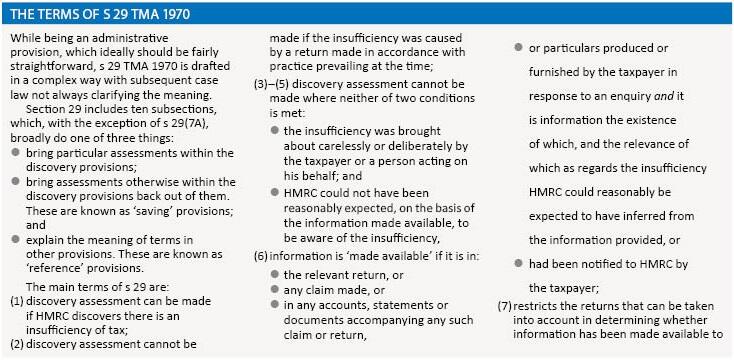

Interpretation of s 29

The discovery provisions have, and continue to be, the subject of much case law. The first important point to make is that the courts have interpreted discovery widely. In Cenlon Finance Co Ltd v Ellwood [1962] AC 782 at 796–797 Lord Simonds said:

‘I can see no reason for saying that a discovery of undercharge can only arise where a new fact has been discovered. The words are apt to include any case in which for any reason it newly appears that the taxpayer has been undercharged and the context supports rather than detracts from this interpretation.’

This makes it difficult, although not impossible, for taxpayers to argue that there has been no discovery. In Charlton v R & C Commrs [2013] STC 866 the court explained that no new information, of fact or law, was required for there to be a discovery. The only requirement was that it had ‘newly appeared’ to an officer, acting honestly and reasonably, that there was an insufficiency in an assessment.

This could be for any reason, including a change of view, change of opinion, or correction of an oversight. The requirement for newness did not relate to the reason for the conclusion reached by the officer, but to the conclusion itself.

This illustrates the breadth of the provisions, potentially giving HMRC far-reaching powers to recoup tax losses. Such a view of the provisions being almost undefeatable was widely adopted after the 2004 case of Langham v Veltema 76 TC 259.

This case was yet another example of HMRC’s discovery assessment being upheld, when the court considered two issues described by Auld LJ as:

‘The first issue is whether awareness or inference of actual insufficiency is required to negative the condition, or would awareness that it was questionable do? The second issue is, what is the relevant information before the inspector on the basis of which he could be said to have been reasonably expected to be aware of an insufficiency?’

Veltema addressed two issues with interpretation of s 29: the level of certainty of awareness of an insufficiency required and the extent to which information outside s 29(6) can be taken into account. On the first, Auld LJ said:

‘It is plain from the wording of the statutory test in s 29(5) that it is concerned, not with what an inspector could reasonably have been expected to do, but with what he could have been reasonably expected to be aware of. It speaks of an inspector’s objective awareness, from the information made available to him by the taxpayer, of ‘the situation’ mentioned in s 29(1), namely an actual insufficiency in the assessment. If he is uneasy about the sufficiency of the assessment, he can exercise his power of enquiry under s 9A and is given plenty of time in which to complete it before the discovery provisions of s 29 take effect.’

On to the second issue, Auld LJ said:

‘The inspector is to be shut out from making a discovery assessment under the section only when the taxpayer or his representatives, in making an honest and accurate return or in responding to a s 9A enquiry, have clearly alerted him to the insufficiency of the assessment, not where the inspector may have some other information, not normally part of his checks, that may put the sufficiency of the assessment in question. If that other information when seen by the inspector does cause him to question the assessment, he has the option of making a s 9A enquiry before the discovery provisions of s 29(5) come into play. That scheme is clearly supported by the express identification in s 29(6) only of categories of information emanating.’

It is from the Veltema case that we have the concept of a hypothetical officer (as in the reference in subsection (5) to an officer) Auld LJ described the relevant issue as being:

‘Whether, as the Inspector contends, only awareness or an inference by him of an actual insufficiency in the self-assessment, though not necessarily its precise extent, would have disentitled him from making a discovery assessment under section 29(5), or whether, as Mr Veltema contends, an awareness or inference by the Inspector of circumstances suggesting a possible insufficiency and the need for some basic check did so.’

The Court held that it was the former. Thus Veltema, not to mention numerous other cases in which HMRC has successfully defended a discovery assessment, gives the impression that the Revenue’s powers when embarking on one are almost unlimited. This is not the case and offers an important lesson in what should be included in a white space disclosure and the grounds on which a discovery assessment can be challenged.

Recent cases: what we can learn

Freeman v HMRC [2013] UKFTT 496 (TC) concerned the proper application of ss 29(2) and (5) TMA 1970.

The facts were:

- the taxpayer swapped shares in a company for loan notes under a reorganisation;

- the exchange was disclosed to HMRC in a white space disclosure on the 1997–98 tax return;

- loan notes subsequently redeemed in 2002–03 were entitled to taper relief as long as they were not, as the taxpayer believed, qualifying corporate bonds (QCBs);

- the 1997–98 return was enquired into in 2000. The taxpayer’s advisors told HMRC that the taxpayer’s view was that these were non-QCBs, which HMRC agreed was likely to be the case;

- the loan notes were not non-QCBs, and so were not entitled to relief; and

- an assessment was issued in 2007.

The First-tier Tribunal (FTT) held:

- the term ‘discovery’ means coming to a conclusion, or having reason to believe, which in turn gives rise to an assessment of tax;

- in Charlton, the FTT introduced the additional requirement of newness, which includes a situation where the original inspector changed their mind or a new inspector took a different view;

- also in Charlton, the Upper Tribunal confirmed all that is required: ‘…is that it has newly appeared to an officer, acting honestly and reasonably, that there is an insufficiency in an assessment.’ This could be for any reason, including a change of view, change of opinion, or correction of an oversight;

- in relation to what might reasonably be expected of an HMRC officer, complex cases will require a different standard of the hypothetical officer. In particularly complex cases, the taxpayer may disclose factual information, but an officer may not reasonably be expected to be aware of an insufficiency of tax due to the complexity of the relevant law; and

- there is no single benchmark of the knowledge and experience the hypothetical officer should expect to possess. The officer cannot be taken to know every fact known to HMRC, nor are they expected to carry the entire corpus of knowledge relevant to their job in their head. An officer in a specialist unit would inevitably have more specialist knowledge.

The FTT held that the disclosure on the 2002–03 return did make clear to any hypothetical officer that the loan notes were acquired in exchange for shares and not subscribed de novo for cash. To that extent, the officer should have been on notice that issues relating to capital gains tax taper relief might be relevant. However, the disclosure on the return was not sufficiently complete and comprehensive.

What saved the taxpayer in Freeman from being a straightforward case within s 29 was the information provided to HMRC on the enquiry and the interaction with the defining terms of s 29(6). The court held:

- enclosing the loan notes under cover of a letter in the earlier enquiry satisfied all the requirements of s 29(6)(d)(ii), other than the notification of its relevance to the insufficiency for the tax year in question, that is, 2002–03;

- there is no time requirement for notification in writing in s 29(6)(d)(ii); and

- since subsection (d)(ii) has no temporal restriction, the loan note instrument that was supplied in 2000 would have alerted an officer, that its terms would have affected liability in 2002–03 because that was the year of the final redemption.

- the taxpayer had provided enough information through an earlier year enquiry – more than two years before the year of assessment to which the discovery assessment related – to show that neither of the conditions in s 29(3) was met.

Another example of the successful defence of a discovery assessment was in Fisher and others v R & C Commrs [2014] SFTD 1341. The facts in this case were:

- the appellants had filed tax returns and, at the times they were submitted, enquiries had been opened into the returns for each of the four previous years;

- in the enquiries for the earlier years, the notices expressly stated that the earlier enquiries would form part of the ongoing enquiries; and

- no notice of enquiry was given for either 2005–06 or 2006–07, but discovery assessments were issued in 2009 for both years.

On these facts it was held that the hypothetical officer – by the time the enquiry windows closed – would have been aware of s 739 being in contention, and the taxpayers succeeded in overturning the discovery assessments.

These cases give important indications as to how the scope of the discovery provisions is circumscribed. Some key points are:

- The scope of the information that must be taken into account under s 29(6) in determining whether information has been ‘made available’ is wider than HMRC has previously contended. Only the returns and claims (and documents provided with them) are restricted to the two immediately preceding chargeable periods – information provided in an enquiry, for an example, can be provided at any time.

- It appears that there will be consideration given to the context in which information is provided to HMRC – as in Fisher, where the context of the existing enquiries was highly pertinent to what the hypothetical inspector could reasonably have been expected to infer.

- It is rare, although not impossible, for a taxpayer to win on the basis that there has been no discovery, since the Veltema approach has been widely adopted in cases since 2004.

- There is, however, a requirement for newness as shown in Charlton. This relates not to the reason for the conclusion reached by the officer, but to the conclusion itself. So it is necessary to carefully examine the circumstances of any discovery assessment made by HMRC.

- Care should be taken after the recent Court of Appeal decision in Sanderson v R & C Commrs [2016] EWCA Civ 19. Even if the actual officer involved in the case has the knowledge they require to raise an enquiry, it is not his knowledge that is relevant, but that of a hypothetical officer. Therefore, it is possible that such actual knowledge would not assist, since it is the ‘reasonable’ officer that must be considered.

Conclusions

There are two possible ways to put into effect the knowledge of the operation of s 29 gleaned from the continuing body of case law. First, in what information is provided to HMRC, both on returns and in response to enquiries. Note that, in Freeman, it was the response to an earlier enquiry that saved the taxpayer. Second, how to deal with a discovery assessment and when the correct approach will be to challenge such assessment by way of appeal.

In relation to the former, it is not enough to simply consider the information being provided to HMRC in terms of volume – the key point is whether the Revenue could have reasonably been expected to be aware of the insufficiency on the basis of that information. If you are aware of more than one possible interpretation thought could be given to simply noting the discrepancy in any white space disclosure, although this might simply draw an enquiry down upon your client. This is an area where much thought should be given and the possibility of taking further advice on the drafting of white space disclosures.

Challenging a discovery assessment must be done through an appeal to the FTT. It should not be assumed that every discovery assessment will stand up. Careful consideration should be given to the circumstances and, in particular, any information provided with returns or claims for the two years preceding the year to which the assessment relates and any information provided in response to an enquiry. It will also be necessary to keep considering the rapidly developing body of case law.

However, recent cases indicate that the discovery provisions do not give HMRC carte blanche to make an assessment and advisers must consider whether such assessment has been validly made, notwithstanding the complex terms defining HMRC’s power considered here.