The Office of Tax Simplification publishes its review findings

Share this article

The OTS reflects on what its mission should be and its ambitions for simplification in the tax system, as well as legacy issues impacting tax reporting and collection.

The Office of Tax Simplification published its review of simplification (see bit.ly/3AIpTwW) on 18 July – just before Parliament rose for the summer recess. The report was triggered by a formal request from the previous Chancellor and the Financial Secretary, following the Treasury’s five-year assessment of the OTS.

The Financial Secretary wrote:

‘The review recommends that the OTS “undertake a project to articulate its approach to and interpretation of ‘tax simplification’, including clarifying its aims as an organisation, and the success measures for assessing its progress”. The Chancellor and I would like you to commence this work as a formal OTS review, focusing on conclusions that can inform how the OTS, and government, should prioritise simplification efforts over the next five years. I look forward to agreeing the detail of the terms of reference in the coming weeks, and to hearing your plans for own-initiative work over the coming months.’

It is useful for the OTS to reflect periodically on what its mission should be and what the ambitions for simplification in the tax system should be.

The purpose of simplification

The first place to start is to declare that simplification is not a policy goal in itself. Rather, it should be a core consideration for the government to support taxpayers through the design, implementation and administration of tax policy at every stage in the policy making process, and when measuring the success of a policy after implementation.

The primary purpose of taxation is to raise funds to support the provision of public services. Parliament may also have other objectives for a given tax policy, such as redistribution, supporting growth and productivity, encouraging or discouraging certain behaviours, and compensating for market failure. There are times when policy design will mean that simplification has to take a back seat. For example, there is the question of equity: different rates, thresholds and allowances all add to the complexity of the tax calculation, but they also ensure that the burden of tax is felt less by those who can afford to pay it less.

The purpose of simplification is to make it easier for taxpayers to comply with the policy and potentially to make it cheaper to comply. Simpler tax policies could also be cheaper for HMRC to operate, which could free up resources to aid other areas of tax. Simpler tax is also easier for taxpayers to understand, which helps us to make better business and family choices. Finally, broader understanding of the tax system and ease of compliance promotes trust, which is a vital ingredient in general support for the tax system.

The policy making process

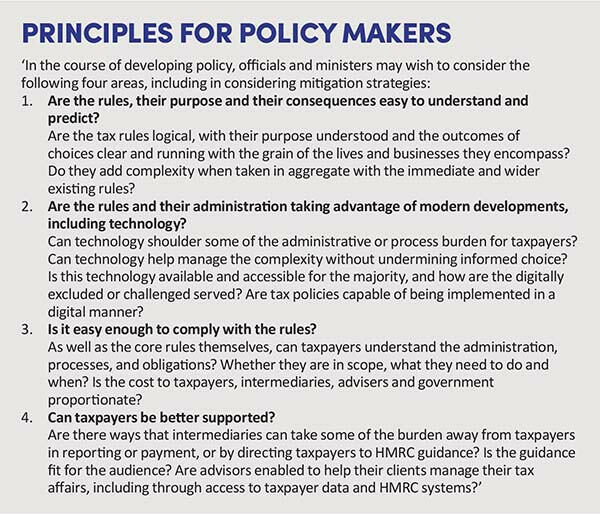

The report recommends that the principle of simplification should be embedded in the general tax policy making process – but without making it part of a checklist (see Principles for policy makers).

Those of us outside the policy making process perhaps do not realise the speed with which policies are developed, in response to political intent. Governments are elected for a maximum of five years and thus have limited time to make changes they view as important for the country, its economy and its tax system. There are also more technical changes to consider, but even those need to fit into a delivery timetable.

Public and private sector IT systems have a big part to play in future delivery of tax policy – and they may often act as a constraint. The OTS looked at the UK’s idiosyncratic tax year end in 2021 and it is obvious to everyone that a 5 April year end is a hindrance to taxpayers, intermediaries and to HMRC. Yet it is not simple to change it to the much more obvious 31 December or 31 March. This is because there are some legacy systems in HMRC, DWP and in major private sector payrolls which could not make any change easily or quickly. The UK will be much better enabled to make policy in a more easily deliverable manner when all such legacy systems have been modernised and ideally transformed.

Tax reporting and collection

One of the core principles of the UK’s tax system is that it depends on intermediaries, who collect or withhold tax and report to HMRC. Employers are likely to hand over about £210 billion in PAYE this year. VAT-registered businesses will pay into the exchequer £154 billion (before VAT refunds of £23 billion). Businesses collect alcohol, tobacco and fuel duties, insurance premium tax, environmental levies and the apprenticeship levy.

However, there is more scope for intermediaries to support reporting to HMRC, even if not tax collection. For example, banks and building societies provide HMRC with data on interest received by individuals. The format of this data means that it is useful for HMRC’s audit activities, but it is not easy to integrate it into personal tax accounts for wider use, including pre-population.

Going forward, more services from intermediaries should be a key part of future tax administration, to the benefit of all of us. We should all support investment in the forthcoming Single Customer Account (including devising a better name!) as the hub to receive data from a wide range of third parties and public bodies for display to us – and to receive our updates and corrections.

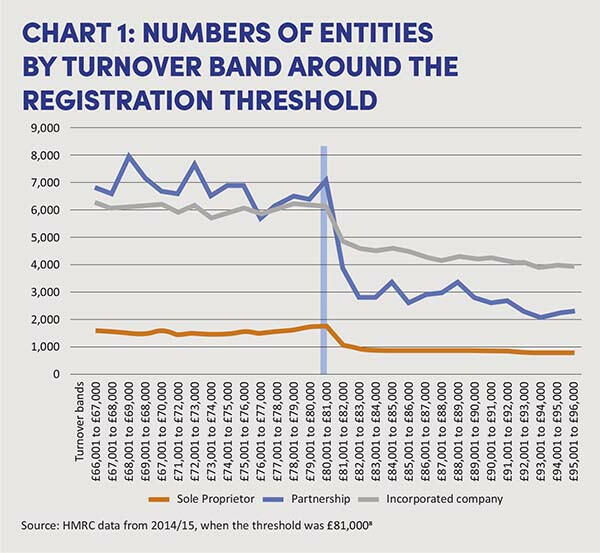

One of the areas that has traditionally been considered as an aid to simplification is the tax threshold – the level at which an individual or business starts to pay tax. Increasing a threshold means that there are fewer taxpayers. This is not always a good thing. One of the best examples of the problems created by a threshold is the VAT registration threshold, where regular readers may recall my June article.

Businesses are well aware that going above the threshold triggers VAT on the whole of their sales, albeit with a reduction for VAT currently paid on business purchases. This means that there is an incentive to keep trading just below the threshold – since going just above it is likely to reduce the business’s net profit. Given the impact of inflation today, some of the businesses operating just below the threshold will find it hard to avoid going over it and we should expect that the government will be asked to help.

There are two options: increasing the threshold; or adopting a new smoothing mechanism to help businesses move into VAT in a more gradual way. Putting up the threshold does not solve the underlying issue: it simply moves it up a bit. A smoothing mechanism – say a lower effective rate of VAT in a range above the registration threshold – may be a much more resilient and long-lasting approach. It could unlock current barriers to micro business growth.

Simplification should always be a core part of policy design and implementation. Ideas from taxpayers, agents and the business community on how to improve our systems will bring benefits to us all. Please therefore send the Office of Tax Simplification your ideas and share your experiences; they inform how we can all help government build and manage a better tax system.

You can contact the OTS at: [email protected]