Ongoing change

Share this article

Charlotte Barbour provides an update on recent developments in Scottish taxation

Key Points

What is the issue?

The Scottish government has used its new tax powers to make various changes, including setting five rates of income tax for 2018/19, the collection of Scottish income tax (SIT), and made changes to Land and Buildings Transaction Tax.

What does it mean to me?

The Professional Bodies (CIOT, ICAS, LSS) have called for an annual process to be put in place and it is encouraging to note that included in the Scottish Government’s legislative programme for 2018/19 is a pledge to reform the way in which devolved tax decisions are planned, managed and implemented.

What can I take away?

The tax powers in Scotland Acts 2012 and 2016 have now, broadly, been implemented. For the future, one can expect ongoing change as the Scottish Parliament begins to fully utilise and fine tune its powers.

This time last year there was much anticipation: what would the Scottish Government do with the new powers that gave it full control over the income tax rates and bands for non-savings, non-dividend (NSND) income? In an innovative and helpful measure before the Budget, the Scottish Government issued ‘The Role of Income Tax in Scotland’s Budget’ (published November 2017) to encourage public debate and inform their decision making. Since then, five rates of income tax have been set for 2018/19 and Scottish income tax (SIT) has been collected from Scottish taxpayers by HMRC. Of interest over the last year has been the forecasting of SIT versus actual receipts, and some fine detail around who is a Scottish taxpayer. There has been considerable change to Land and Buildings Transaction Tax (LBTT) bringing into sharper focus the need for a proper process for changes to devolved tax legislation, Air Departure Tax (ADT) is on hold, and there have been some decisions from the Scottish First-tier Tribunal Tax Chamber which provide helpful direction. The Scottish Budget is to be on the 12 December.

Scottish income tax

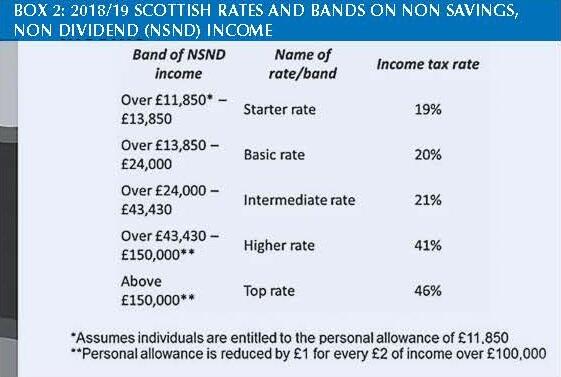

SIT was implemented on 6 April 2017 (replacing the Scottish Rate of Income Tax which had been in place for one year) and its profile has been raised as the differentials between north and south of the border have increased across thresholds and rates, and from one year to another. The direction of travel with five bands and a more progressive charging structure was set last year. (See box 2.)

SIT does not sit in isolation – and bringing in five income tax bands makes its interaction with other parts of the income tax system an administrative nuisance, particularly in relation to withholding tax, or giving tax relief at source. The Scottish basic rate now applies to a band of income between £13,850 and £24,000 whilst new rates of 19% and 21% were introduced below and above this. This has led to issues around giving tax relief at the correct rate, affecting pensions tax relief in the main, but also with other anomalies or complications arising on items such as Gift Aid tax relief, tax relief for landlords on residential property finance costs, deficiencies relief, and the basic earnings assessment for childcare. HMRC had previously prepared three technical notes (Clarifying the scope of Scottish Income Tax powers (Nov 2016), Clarifying the scope of the Scottish rate of Income Tax (Dec 2014), and Clarifying the Scope of the Scottish Rate of Income Tax (May 2012)) and further guidance was issued for pension arrangements operating on a relief at source basis in February 2018. The fundamental problems are not fully resolved however, and the issues may re-emerge if rates diverge further.

Differentials in the higher rate threshold for Scottish taxpayers compared to the rest of the UK continue to disadvantage some Scottish taxpayers’ in relation to claims for Marriage Allowance. Whilst amendments to UK legislation were made last year to enable any Scottish taxpayer on starter, basic or intermediate rates to be eligible, the allowance remains more restricted for Scottish taxpaying couples. The interaction of thresholds for income tax and national insurance in 2018/19 also lead to those Scottish taxpayers who are employees with earnings between the two higher rate thresholds of £43,430 and £46,350 suffering a combined marginal rate of 53%; on self-employed earnings the combined marginal rate is 50%.

The definition of a Scottish taxpayer is to subtly alter, in order to interact with the definition of a Welsh taxpayer, from 6 April 2019 onwards. The changes may have been hard to spot because they are contained in the Wales Act 2014 s 11 as amendments to the Scotland Act 1998 and the Government of Wales Act 2006. They will come into effect from 6 April 2019 under The Wales Act 2014 (Commencement No. 2) Order 2018, SI 2018/892, which was made in July 2018.

The fiscal apparatus

Structural changes continue to take place. The Scottish Government is reorganising its finance function to include a dedicated taxation resource, with the appointment of a Minister for Public Finance and the Digital Economy, and the establishment of a post of Director of Taxation; this is a welcome development.

There are other institutional developments as the fiscal bodies become established and move from start up to an operational phase. In May 2018 Revenue Scotland issued its new corporate plan for 2018–2021. The Scottish Fiscal Commission, a statutory body, issued its second economic forecast in May 2018. This document proved controversial with SIT revenues forecast to be lower by £209m compared to the February 2018 forecast. Further questions around the forecasting, and collection, of the amounts of SIT arose with the publication of the outturn figures for 2016/17 by HMRC in their annual report (supplemented by a technical note on Scottish taxes).

Devolved taxes

Land and Buildings Transaction Tax (LBTT) has been notable in that since its commencement in April 2015 there have been several changes to it. These have included:

- A new charge to tax – additional dwelling supplement, introduced from 1 April 2016 by way of primary legislation Land and Buildings Transaction Tax (Amendment) (Scotland) Act 2016; amended by a Scottish Statutory Instrument (SSI 2017/233) on 30 June 2017 The Land and Buildings Transaction Tax (Additional Amount-Second Homes Main Residence Relief) (Scotland) Order 2017 and the amendment then made retrospective, which requires primary legislation, with Land and Buildings Transaction Tax (Relief from Additional Amount) (Scotland) Act 2018.

- A new relief – first-time buyer relief, introduced by SSI 2018/221 The Land and Buildings Transaction Tax (First-Time Buyer Relief) (Scotland) Order 2018 (‘The Order’) which came into effect on 30 June 2018.

- Removal of anomalies – for example around group relief, which has been addressed in the most recent LBTT Technical Update.

There remain further potential changes in the pipeline, such as to provide seeding relief, which has recently been the subject of a Scottish Government consultation. Advisers also need to be mindful that a provision in the original LBTT legislation regarding commercial leases comes into practical effect from April 2018 because a three yearly return is required.

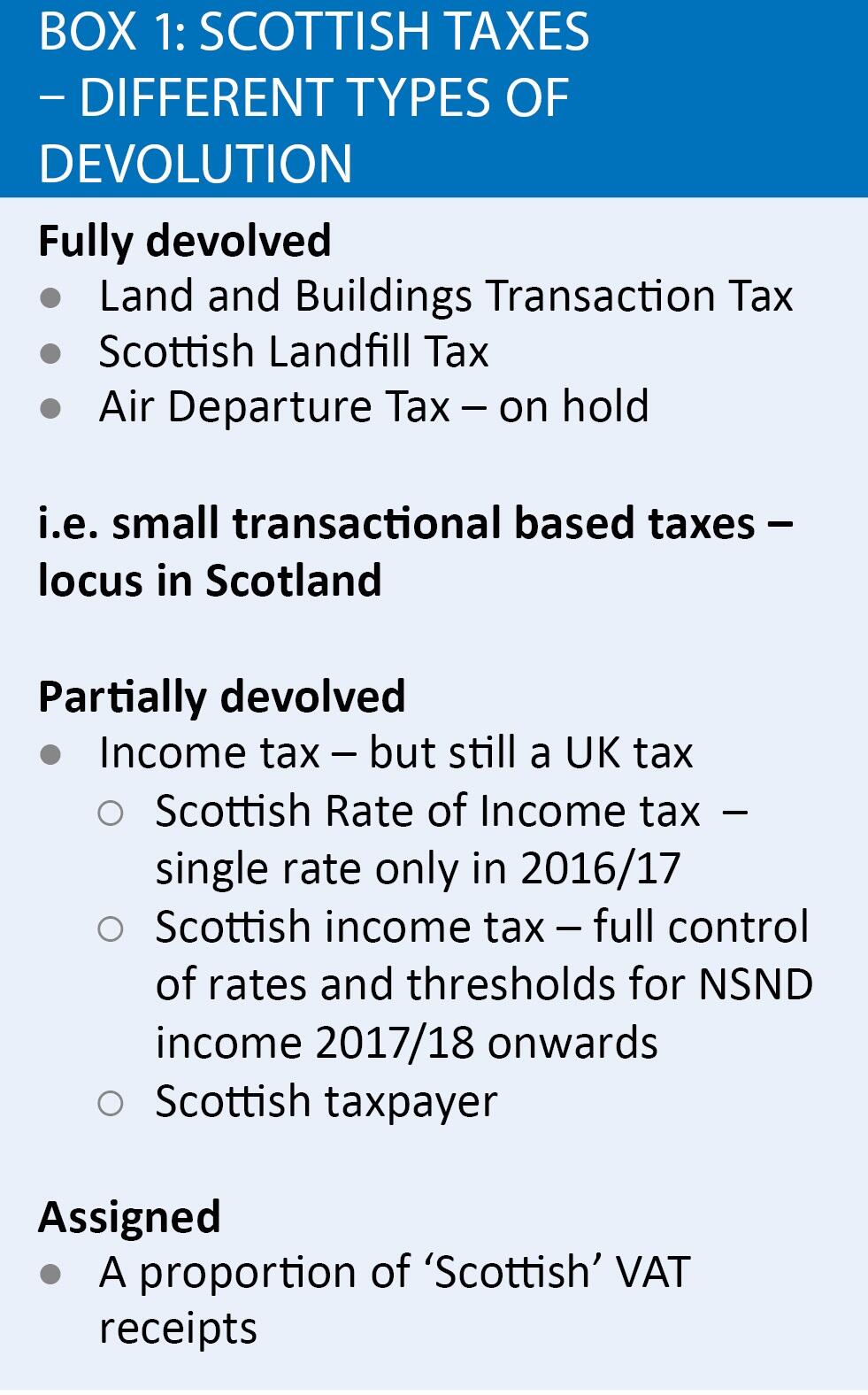

See box 1 for a summary of devolved and non devolved taxes, and box 2 for a summary of Scottish rates and bands on non savings and non dividends.

Process

A major concern around the changes introduced to LBTT is that there is no regular process for bringing forward and considering such amendments. So far, there is only a limited annual procedure for a Scottish rate resolution setting the income tax rates and bands. The Professional Bodies (CIOT, ICAS, LSS) have called for an annual process to be put in place and it is encouraging to note that included in the Scottish Government’s legislative programme for 2018/19 is a pledge to reform the way in which devolved tax decisions are planned, managed and implemented (page 61).

Air Departure Tax

Air Departure Tax (ADT) is currently ‘on hold’. The legislation is in place – the Air Departure Tax (Scotland) Act 2017 received Royal Assent on 25 July 2017 and was designed to replace the UK levy Air Passenger Duty (APD) from April 2018. The delay in implementation is due to state aid rules. Passengers carried on flights from airports in the Scottish Highlands and Islands have been exempt from APD since 2001, but transfer of the exemption to the new ADT requires notification to and assessment by the European Commission in compliance with EU law. In June 2018 the Scottish and UK Governments agreed that it would not be possible to introduce ADT in April 2019 – instead, APD at the UK rates and bands, with the Highlands and Islands exemption, will continue to apply in Scotland until further notice.

Devolved tax tribunal decisions

From 24 April 2017 the First-tier Tax Tribunal for Scotland was abolished and its functions and members transferred to a Tax Chamber within the newly-established First-tier Tribunal for Scotland.

There have been seven first-tier decisions published since then; five regarding LBTT and two SLfT of which four were about Penalties, one on procedure, and two on Additional Dwelling Supplement. The key points of broader interest in these are first, the need to follow due process in the Revenue Scotland and Tax Powers Act 2014 (RSTPA) and, second, that UK case law may be relevant. As noted in Straid Farms Ltd [2017] FTSTC 2, paragraph 30, ‘…the Explanatory Notes to RSTPA state: “The effect of [the legislation] is that the jurisprudence concerning the proper bounds of the tax authority’s role is imported into the devolved tax system. This jurisprudence includes not only case law from the UK jurisdictions but other English-speaking jurisdictions.”’

VAT assignment

The Scotland Act 2016 provided for the assignment of a proportion of Scottish VAT; this is expected to be in place from April 2019. In essence, VAT assignment is a funding mechanism, designed to introduce a further link between funding and the performance of the Scottish economy, although at the time of writing the precise mechanics have yet to be announced. The Scottish Government is working with HMRC and HM Treasury to produce a model of VAT liabilities in Scotland using a regional version of HMRC’s VAT Theoretical Tax Liability (VTTL) model.

Never a dull moment…

The tax powers in Scotland Acts 2012 and 2016 have now, broadly, been implemented. For the future, one can expect ongoing change as the Scottish Parliament begins to fully utilise and fine tune its powers.