The price of business: keeping energy costs down

Share this article

In the light of current high energy prices, we take a look at ways that businesses can try to keep their energy costs down by using tax reliefs, exemptions and allowances.

Key Points

What is the issue?

Businesses are experiencing significantly increased energy prices. The Energy Bill Relief Scheme caps wholesale energy costs for businesses until 31 March 2023 and is replaced by a less generous discount on energy prices from 1 April 2023 to 31 March 2024.

What does it mean for me?

Businesses are examining their energy costs more closely and seeking ways to reduce cost. There are reliefs, exemptions and allowances available to help reduce energy costs for business.

What can I take away?

For any business with high energy use it is worth checking the detail of climate change levy exemptions, climate change agreements, and energy intensive industries exemption that may be available.

© Getty images/iStockphoto

Business energy costs have been at record highs recently with an unprecedented level of intervention from the government. Business is supported by the Energy Price Guarantee until 31 March 2023, with a less generous Energy Bills Discount scheme to follow from 1 April 2023 to 31 March 2024 (see bit.ly/3H4SrnD).

For energy intensive industrial sectors, energy can represent a large proportion of total costs. There is a plethora of taxes and levies on energy, with a series of reliefs and exemptions available. There is an increased focus amongst industrial energy users in making sure that they are accessing and maximising all of the savings available to them to help relieve the cost pressure.

This article explores the reliefs, exemptions and allowances available, the sectors that qualify, and how to access them.

Climate change levy reliefs and exemptions

Climate change levy (CCL) is a tax on supplies of gas, electricity and some other fuels to business users.It is charged on energy bills by the energy supplier.

The main rates of CCL are 0.775p/kWh for electricity and 0.568p/kWh for gas. Compared to the current Government Supported Price of 21.1p/kWh for electricity and 7.5p/kWh for gas, CCL represents an additional cost of 4.7% for electricity and 7.6% for gas.

Some businesses are eligible for reliefs and exemptions from CCL, but they have to be claimed. Below we cover the reliefs and exemptions that are most likely to have the broadest application.

Supplies for non-business use by a charity or for domestic use and community heating schemes are excluded from CCL. The definitions of charitable and domestic use mirror the VAT rules, and the VAT reduced rate generally applies where the supply is excluded from CCL. Examples of where this may apply may include universities, which are charities, that may use some energy for their non-business research use, and pubs or shops that may have accommodation on site resulting in some domestic use.

There is a CCL exemption available for operators of mineralogical and metallurgical processes. Broadly, mineralogical processes involve the manufacture of glass, ceramic, refractory, cement, lime, plaster, concrete and stone products. Metallurgical processes involve the manufacture of iron and steel, precious metals, aluminium, lead, zinc, tin, copper, other non-ferrous metals and their products. There is detailed guidance on the processes that qualify in Annex A of HMRC’s Excise Notice CCL1/3 (see bit.ly/3X1ArQz).

To claim the exemption, the operators of eligible processes need to complete form PP10 to calculate their relief entitlement and send it to HMRC. The operator should then take the percentage figure calculated on form PP10, put it onto form PP11 and send it to their energy supplier so that the energy supplier can apply the relief directly to the energy bill. Separate forms need to be completed for gas and electricity.

Energy intensive businesses can also claim CCL discounts of 92% for electricity and 86% (or 88% from 1 April 2023) for gas until 31 March 2025 if they have entered into a climate change agreement. These are voluntary agreements made between Industry Associations and the Environment Agency to reduce energy use and carbon dioxide emissions. The government is currently consulting on a replacement scheme to continue to support affected sectors when the current agreements end (see bit.ly/3ZncLYq). Climate change agreements cover a wide range of sectors from chemicals, plastic and paper to supermarkets and agricultural businesses such as pig and poultry farming. A full list is available at bit.ly/3ZjUfAh.

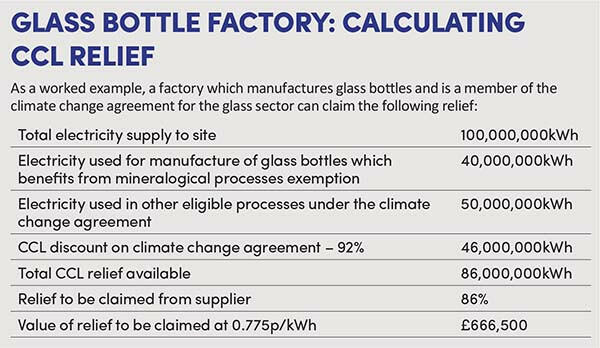

CCL discounts for energy used under a climate change agreement are also claimed through the use of forms PP10 and PP11. See the example above Glass bottle factory: calculating CCL relief for how CCL works in practice.

On-site generation of electricity

Investment in on-site generation is increasingly favourable in the light of increased energy costs, which have increased the return on investment and reduced payback periods.

Renewable electricity generated on-site is outside the scope of CCL.

For businesses that have a heat need, or local heat offtake available, combined heat and power plants also receive favourable treatment under the CCL rules with exemptions available for fuel inputs, carbon price support and electricity self-supplies provided that the scheme is registered under the Combined Heat and Power Quality Assurance (CHPQA) scheme and meets the efficiency criteria to be good quality.

Business rates

The March 2022 budget announced the exemption of plant and machinery used in on-site renewable energy from business rates, effective from 1 April 2022 to 31 March 2035. This exemption makes it highly attractive to install roof top solar panels, wind turbines and battery storage to store and generate on-site renewable energy. In addition, there is 100% relief for eligible low-carbon heat networks, which have their own rates bill, and the storage used with electric vehicle charging points. With the 2023 business rates revaluation on the way, it is a good time for businesses with on-site generation to review their business rates to ensure they are receiving the reliefs available to them.

Capital allowances: super deduction

Expenditure on on-site generation, such as combined heat and power plant, can currently benefit from significant capital allowances tax relief, which give businesses tax relief for certain capital expenditure. Companies (only) can currently benefit from enhanced first year capital allowances for capital expenditure incurred between 1 April 2021 and 31 March 2023, on certain new items of plant and machinery.

The enhanced relief is split into two categories and the rate of relief varies depending on the nature of the expenditure:

- 130% super deduction (increased from 18% per year): ‘apparatus’ used in the business that is not classed as special rate plant and machinery, including significant elements of combined heat and power plants; and

- 50% first year allowance (increased from 6% per year): for expenditure on special rate plant and machinery. This includes integral features such as air-conditioning, general power and lighting and solar PV panels; plus, assets with an expected useful economic life of 25 years or more.

Although the enhanced reliefs are due to come to an end on 1 April 2023, they are currently part of an HM Treasury consultation into the capital allowances regime. The consultation was launched in the summer of 2022 and we expect the spring 2023 budget on 15 March to include details of any extension or replacement to the super deduction and 50% first year allowance.

The previous enhanced capital allowances scheme, which provided 100% tax relief for certain energy and water efficient plant and machinery, was considered too cumbersome and was discontinued for expenditure after April 2020.

Energy intensive industries exemption scheme

The UK has a number of policies and schemes to incentivise and increase the share of electricity generated from low carbon and renewable sources. These include Contracts for Difference (CFD), Renewables Obligation (RO) schemes and the Small-Scale Feed-In-Tariff (FiT). The cost of funding these policies is borne by electricity consumers through levies added to their bills.

The energy intensive industries exemption scheme supports energy intensive businesses in sectors which suffer from international competition by exempting eligible businesses from up to 85% of the charges arising from the costs of CFD, RO and FiT.

The UK Energy Security Strategy published in April 2022 committed to continuing to help industries in the UK that face higher industrial energy prices. The Department for Business Energy and Industrial Strategy (BEIS) consulted on changes to the scheme in August 2022 with a view to potentially increasing the amount of exemption provided. In the consultation document, BEIS published a comparison of the taxes and levies borne by extra-large industrial consumers in other European countries, showing the UK as second only to Germany, and both countries paying almost double the price per KW borne by Poland, which followed them in the size of levy (see bit.ly/3ZntElM).

In order to benefit from these savings, eligible businesses must apply to BEIS and be approved for an energy intensive industry exemption certificate. The business then provides the certificate to their energy supplier, which applies the savings directly to their energy bills.

Eligible businesses must meet the following two tests:

- the ‘sector level test’, which requires that the business must manufacture a product in the UK within an eligible sector (defined by a four-digit NACE Code); and

- the ‘business level test’, which is the requirement to pass a 20% electricity intensity test.

Additionally, the business must not be an ailing or insolvent economic actor, have at least two quarters of financial data and be able to provide evidence of the proportion of electricity used to manufacture the product for a period of at least three months.

Eligible sectors

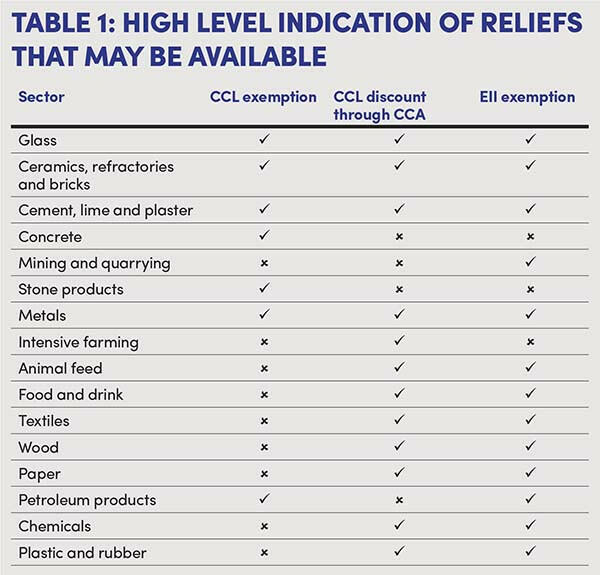

BEIS guidance for applicants sets out a list of sectors that qualify for the ‘sector level test’, along with their four-digit NACE code (see bit.ly/3ZrRuN0). There are 71 eligible NACE codes listed, which have a lot in common with the mineralogical and metallurgical processes eligible for CCL exemption and sectors eligible for CCL discounts through climate change agreements.

Table 1 above contains a high level summary of some of the eligible sectors with an indication of the reliefs that may be available, depending on the specific activities and NACE codes. Given the breadth of sectors that qualify it is not a fully comprehensive list. For any business with high energy consumption, it is worth checking the details of CCL exemptions, climate change agreements and energy intensive industry exemptions available.

Energy intensity test

The energy intensity test requires that business can show that their electricity costs amount to 20% or more of their Gross Value Added (GVA), an adjusted measure of earnings, over a reference period, normally based on the accounting period.

There is a specified method for calculating both electricity costs and GVA to ensure that all applicants are treated in the same way, regardless of the actual price they have negotiated for their energy. GVA is defined as earnings before interest, tax, depreciation and amortisation (EBITDA), excluding extraordinary items and staff costs.

For businesses with both eligible activities and ineligible activities, the energy intensity test is conducted at entity level, including all uses, but the relief will only be available for the portion of the electricity used in the eligible activities.

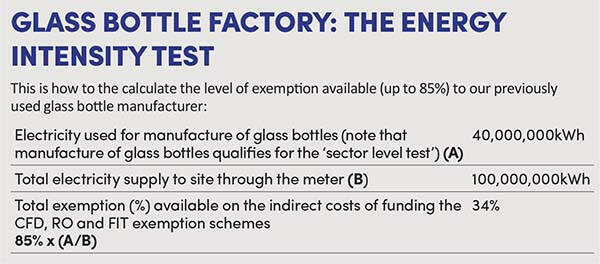

There is a detailed application form for businesses to complete, and BEIS can also require that applications are accompanied by an accountant’s report from the company’s auditors. See the example Glass bottle factory: the energy intensity test for how this works in practice.

Energy efficiency improvements

As noted above, expenditure on new more efficient equipment and plant and machinery will qualify for capital allowances relief against your businesses operating profits, currently at enhanced rates. This can also include expenditure on the installation of thermal insulation to existing buildings that qualifies for capital allowances at the special rate of tax relief.

Conclusion

With the current high cost of energy for business users, there is increased focus on using available cost saving mechanisms.

For industrial businesses with high energy use, there is a wide range of reliefs, exemptions and allowances to help.

On-site generation of electricity is increasingly attractive due to the improved return on investment resulting from higher energy prices. Some forms of on-site generation, such as renewables and combined heat and power plants, benefit from favourable CCL treatment. Maximising both business rates savings and capital allowances can help to further support the business case for investment.