Process in place

Share this article

Nandeesh Mehta considers the challenges for R&D claims made by companies, and the importance of putting a process in place to ensure that claims are being processed accurately

Key Points

What is the issue?

Although R&D relief has been around for a while, the R&D credit scheme introduced in 2013 by HMRC (mandatory since 31 March 2016) has led to a range of considerations for large companies claiming R&D relief.

What does this mean to me in practice?

The change meant that R&D claims in large companies look very different to the claims made by small companies. Although the accounting for R&D claims in small companies is relatively simple, it’s not the case for the R&D credit scheme used by large companies.

What can I take away?

A group of large UK companies with multiple R&D claims should keep a tracker as the timing of these claims often leads to accounting challenges. It is recommended that such companies have a process in place to ensure that the R&D claims are being processed accurately (seven step process in the legislation) and that the credit (where relevant) is being accounted for correctly. This can be challenging where you have R&D claims in a mix of profit making and loss making companies and where the R&D spend is accounted for differently, i.e. either as revenue expenditure or capitalised expenditure (tangible or intangible assets).

Background

R&D is a corporation tax relief that normally reduces a company’s tax bill. The way a company claims tax relief depends on the size of that company.

Generally, a company can only claim for R&D tax relief if an R&D project seeks to achieve an advance in overall knowledge or capability in a field of science or technology through the resolution of scientific or technological uncertainty and not simply an advance in its own state of knowledge or capability. The types of costs that usually qualify, subject to further rules to consider, are staff costs, software or consumables, subcontracted R&D costs or externally provided workers.

In broad terms, the Small or Medium-sized Enterprise (SME) Scheme applies to companies with less than 500 employees with either an annual turnover under €100 million or a balance sheet under €86 million. A group of companies must be taken as a whole when applying these thresholds. Otherwise the company must claim under the Large Company R&D Expenditure Credit (‘RDEC’) Scheme (also referred to as the ‘above the line’ or ‘ATL’ credit scheme).

In SMEs, where costs qualify for R&D relief, the tax relief on allowable R&D costs is 230% (from 1 April 2015). This means that for every £100 of qualifying costs, an SME could reduce their taxable profits by an additional £130 on top of the £100 spent. For large companies, the RDEC scheme gives tax relief at 11% (was 10% prior to 1 April 2015) on the amount of qualifying R&D expenditure but the mechanics are fairly complex which usually result in an effective benefit of 8.8%. This is a slightly more favourable result than the previous ‘super deduction’ scheme for large companies which used to give tax relief at 130% (effective benefit of 6% based on a 20% corporation tax rate). The SME and RDEC schemes give very different results and this article only considers the RDEC scheme (which is for large companies) in further detail.

RDEC scheme

The RDEC scheme was introduced in Finance Act 2013, and if elected, applied to R&D expenditure incurring on or after 1 April 2013. The previous ‘super-deduction’ scheme was available until 31 March 2016 after which the RDEC scheme was mandatory.

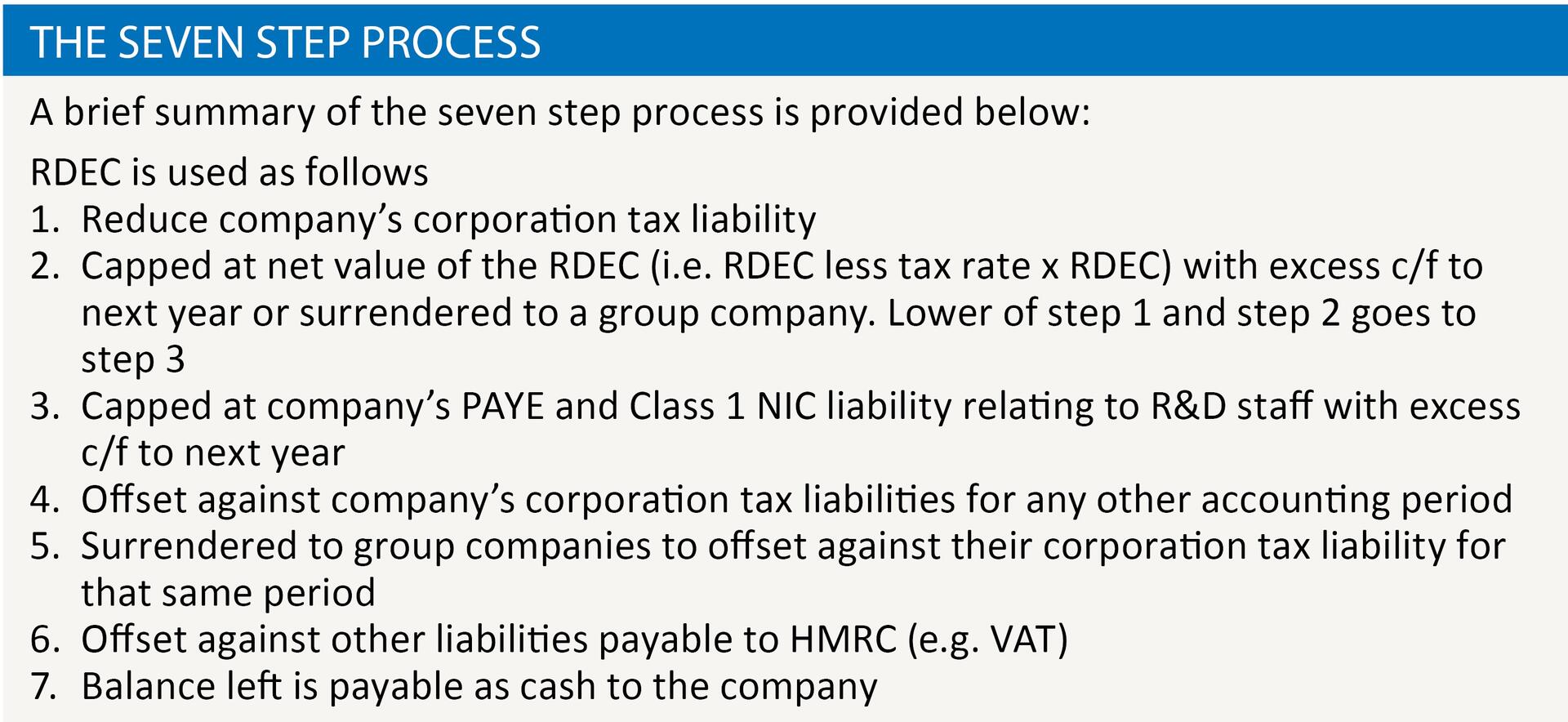

The benefit of the RDEC scheme continues to be based on a company’s qualifying R&D expenditure but a key change is that subject to certain limitations, the credit could result in cash back to loss making companies. There is a 7 step process to follow before HMRC pays this cash to the company. See the seven step process boxout.

Overall, this means that RDEC will be of monetary value to claimants irrespective of their tax position, providing greater certainty of relief, and increasing the incentive for R&D investment in the UK.

It is expected that a significant number of companies will benefit from the receipt of cash (e.g. loss making companies). Although there is limitation on cash receipts based on a PAYE/NIC cap (in the seven step process), it is not expected to affect many entities.

Accounting for RDEC scheme

RDEC is presented ‘above the line’ in a company’s statutory accounts and not as a reduction to income tax expense. It was an explicit aim of the government to design the new scheme such that it had the attributes of a ‘grant’ so it could be accounted for ‘above the line’ to further incentivise innovative investment by large companies.

For most companies, R&D expenditure is expensed to the profit and loss account. In such cases, the RDEC is calculated as follows:

Qualifying R&D expenditure x 11% (was 10% before 1 April 2015) = RDEC

This credit can be recognised ‘above the line’ which incentivises Finance Directors to boost their profits for the year. The accounting challenges are due to the timing of these credits. For a company with a year ended 31 December 2015, the R&D claim may not be finalised and submitted until 31 December 2017. Finance Directors are normally keen to recognise the RDEC in their results for FY15. So this normally means an estimate is included in the FY15 accounts which should get tracked until the final claim is submitted following which a true up exercise should be carried out to adjust it to the actual RDEC (as submitted to HMRC).

For example, say the following RDECs were included in the FY15 and FY16 accounts:

£20k credit in FY15 accounts (estimate relating to the FY15 R&D claim)

£10k credit in FY16 accounts (estimate relating to FY16 claim)

Say the actual R&D claims eventually turned out to be:

FY15 claim made by 31 December 2017 of £150k giving an actual FY15 credit of £16.5k

FY16 claim made by 31 December 2018 of £50k giving an actual FY16 credit of £5.5k

The above results in the FY17 accounts needing a true up adjustment of £3.5k (£20k less £16.5k) in respect of the FY15 R&D claim and the FY18 accounts needing a true up adjustment of £4.5k (£10k less £5.5k) in respect of the FY16 R&D claim.

The above shows why it is important to track the credits as in a given year the accounts might include a combination of a current year estimate (that year’s estimated R&D claim) as well as prior year true ups (based on actual claims made in the tax returns). A tracker is therefore recommended to keep year by year analysis of actuals vs estimates across the set of companies claiming R&D. There is a further challenge where the R&D expenditure is capitalised as an intangible asset (considered below).

Loss making companies

For loss making companies the RDEC can be ‘surrendered’ to other profitable UK group companies (subject to caps in some cases) thereby lowering their corporation tax liabilities and hence the overall group’s corporation tax liability. Where the credit is ‘surrendered’ in this way, accounting for these credits should be considered carefully as some group companies may pay each other for such credits.

Where a loss making company gets the RDEC in form of cash back from HMRC, they have to wait until HMRC processes the tax return (which includes the R&D claim) to receive this refund. This should be accounted for appropriately by showing a corporation tax debtor on the balance sheet until the cash is actually received.

Intangible assets

R&D costs capitalised as an intangible asset are fairly complicated to deal with when it comes to its accounting. They should effectively follow the accounting principles of a government grant. This means that the RDEC is ‘capitalised’ (either separately within deferred income or by reducing the intangible asset – depending on the accounting standard) and amortised over the useful life of the related intangible. The impact is that the RDEC is recognised over the life of the intangible asset rather than as an immediate credit in the P&L. This results in accounting challenges (especially deferred tax) and a tracker is required to follow the recognition of the RDEC over the useful life of the related intangible (including making any adjustments each year for estimates included vs the actual R&D claim).

Tangible assets

Tangible assets which qualify for R&D simply get 100% capital allowances in year of expenditure and there is no RDEC to consider on these. It’s worth noting that a deferred tax liability is created (as it has no tax value against the accounting Net Book Value of the asset) and this reduces over time as the depreciation charge unwinds each year.

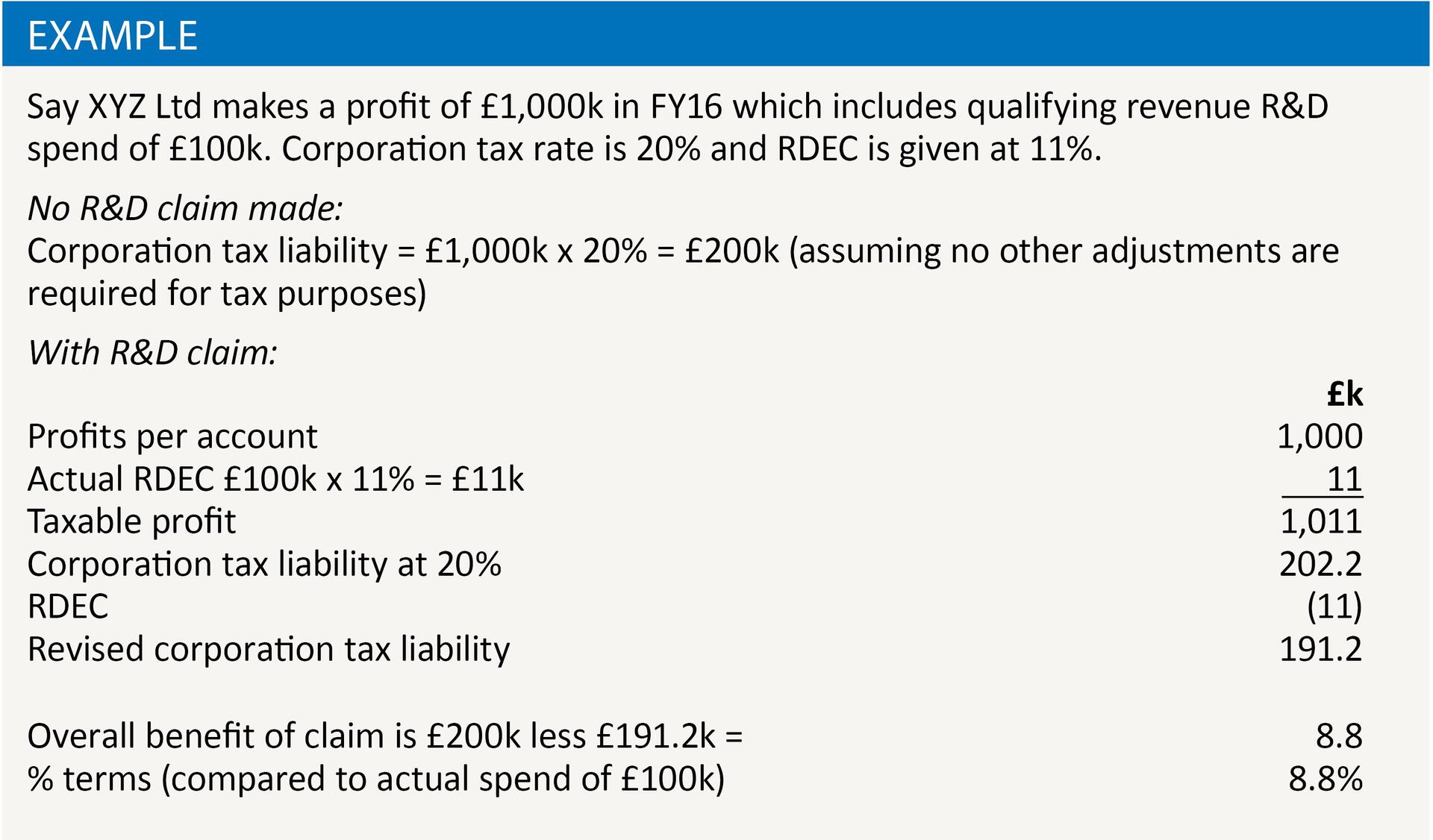

What is the overall benefit of an R&D claim and how is it calculated?

The effective tax benefit of an R&D claim for large companies is 8.8% (from 1 April 2015) of the R&D spend. This is explained in the example.

Budget 2017 announcement

The Chancellor of the Exchequer, Philip Hammond, announced in his Spring Budget on 8 March 2017 that they are going to consider further improving the R&D scheme. No further details were given but hopefully the changes may also lead to a simplification of the accounting required under the RDEC scheme.

Conclusion

The RDEC scheme introduced by HMRC has led to various accounting challenges for a group of large UK companies with multiple R&D claims across a mix of profit and loss making companies. It is therefore important to keep a tracker to monitor the estimates vs actual RDECs each year so that the true up adjustments are easier to calculate. This tracker should be updated at least on an annual basis, and where the RDECs are fairly large, early conversations with your auditors are recommended.