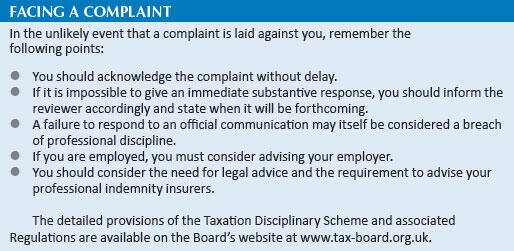

Providing a fair hearing

Share this article

In this second of two articles, Brian Palmer sets out what happens once a referral has been made to the Taxation Disciplinary Board

Key Points

What’s the issue?

The Taxation Disciplinary Board (TDB) is empowered to deal with complaints alleging breaches of professional standards and guidance, the provision of inadequate professional service, and conduct unbefitting a professional person.

What can I take away?

Where it has been established that breach of discipline has occurred, a Disciplinary Tribunal may impose such penalties as it considers appropriate in accordance with powers given to it, after taking into account the gravity of the breach and the facts and arguments presented.

What does it mean to me?

The TDB ensures that there is a fair and independent investigation of every complaint referred to it and also ensures the fair treatment of any member against whom a complaint is made.

The purpose of the Tax Disciplinary Board (TDB) is to ensure that tax advisers maintain the highest professional standards of conduct and to exercise professional discipline over those who fail to comply. It is empowered to deal with complaints alleging breaches of professional standards and guidance, the provision of inadequate professional service, and conduct unbefitting a professional person. After all, it is of paramount importance that public confidence in our profession is maintained.

The TDB is there to support and maintain the high professional standards of the CIOT and ATT; and to handle complaints quickly, impartially and effectively. It promises to:

- operate economically;

- have easy to understand policy and procedures; and

- publish simple guidance for complainants and members.

What happens when a complaint is received?

A complaint is normally received by the TDB’s Executive Director. As a first stage, complainants are advised that bringing a complaint to the TDB is no substitute for initially seeking redress through the complaints procedure of the member or the member’s firm. Complainants can also possibly seek redress through the courts, although it has to be recognised that for many a referral to TDB is a less stressful and more cost effective solution. While the Board can decide on whether a member has complied with professional conduct regulations relating to fees, it does not offer legal advice or intervene in fee disputes. In summary, there are three ways in which a member (or student) can be referred to the TDB:

- a complaint by a member of the public;

- a referral by HMRC; and

- a referral by CIOT/ATT.

Review stage

At the outset, the complainant is sent a standard complaint form to complete. Once returned, it will be examined

by a TDB officer (the reviewer), who is expected to consider whether the complaint falls within the Board’s jurisdiction, and has been submitted within 24 months of the events which form the subject matter of the complaint.

Assuming these criteria have been met, the reviewer will forward the complaint, together with a full pack of related correspondence, to the member, inviting them to respond with any observations they might wish to make. The member’s response is, in turn, forwarded to the complainant. The member is then given a further opportunity to comment.

While rare, there are occasions where the reviewer considers a matter to be trivial or vexatious and the complainant will be advised accordingly. If the complainant objects to that decision, they are entitled to request that the matter be considered by an investigatory assessor. The investigatory assessor is an independent person appointed by the Board. It is more common

that the reviewer refers a complaint for examination by the Investigation Committee. Typically, it takes three or four months to reach the referral stage.

The Investigation Committee

An Investigation Committee is made up of three or five members recruited by the Board. They are drawn, in part, from the TDB’s sponsoring bodies, with the balance being made up of lay members. All are required to preserve the TDB’s independence. To ensure that this happens, lay members are always in the majority and usually include a legally qualified member.

The role of an Investigation Committee, which meets in private, is to consider the documentary evidence prepared and submitted to it by the reviewer in order to determine whether there is a prima facie case (an arguable case to answer) against a member. If deemed appropriate, the Investigation Committee will instruct the reviewer to undertake any further enquiries considered necessary in order for it to be apprised of the full facts relevant to the allegation.

Once the committee is satisfied with the material before it, it may either dismiss the complaint or find that there is a prima facie case to answer. Where it is considered that there is a prima facie case, the Investigation Committee may still decide to take no action, if the matter is not serious enough to merit a sanction. Otherwise, the case will be referred to the Disciplinary Tribunal.

Both parties will be advised of the Investigation Committee’s decision and the reasons for it. They will also have the right of appeal to an investigatory assessor (if either party objects), whose decision is final. The assessor may either uphold the Investigation Committee’s decision or ask for it to be considered by a new Investigation Committee panel.

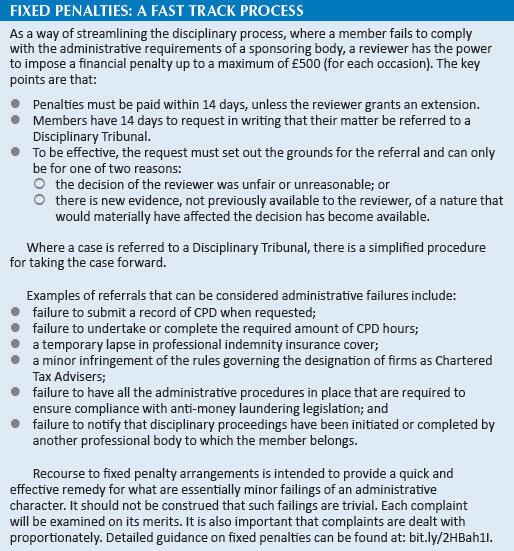

Interim orders

While it is common for prima facie cases to go straight to the Disciplinary Tribunal, an interim order may be applied. These were introduced in 2016, as an additional layer of protection where it is considered to be in the public interest, or necessary for the protection of the public, that a member’s membership should be suspended pending the full hearing of disciplinary charges by a Disciplinary Tribunal.

The Disciplinary Tribunal

The tribunal is composed of three members, two of whom are lay members and one of whom is a member of either of the sponsoring bodies. The chairman of the Disciplinary Tribunal is legally qualified.

The Disciplinary Tribunal’s role is to consider the evidence presented to it by a lawyer (the presenter) acting on behalf of the Board and the member (who may also be legally represented), and to determine whether or not the alleged conduct is proven and to make a finding accordingly. However, a Disciplinary Tribunal, unlike an Investigation Committee, sits in public with both parties given an opportunity to attend, even if they do not wish to give evidence.

A member will be advised if a complaint against them has been referred to a Disciplinary Tribunal and at the same time they will receive details of a proposed date, time and location for the hearing. This should be acknowledged as soon as practical and, where applicable, giving valid reasons preventing attendance.

Prior to the hearing, the member will be informed of the charges, invited to set out their response and to indicate what, if any, evidence they intend to rely upon. In addition, they are required to name any witnesses they might intend to call upon.

The Disciplinary Tribunal process and procedure, the right to be heard and to call witnesses, if required, are explained in the material issued by the clerk to tribunal. While a member may opt to present their case in person, it is for them to consider whether to appoint external advice and counsel.

Where it has been established that breach of discipline has occurred, a Disciplinary Tribunal may impose such penalties as it considers appropriate in accordance with powers given to it, after taking into account the gravity of the breach and the facts and arguments presented.

The tribunal has a wide range of sanctions available to it, including:

- a requirement to apologise;

- the ability to fine or issue an admonishment; and

- suspension or, in the most egregious instances, expulsion.

There is also a power to award compensation where the tribunal has made a finding of inadequate professional service. If a finding is made against a member, a Disciplinary Tribunal will normally make an award of costs.

The tribunal’s decisions will be sent in writing to both the member and the complainant, with reasons given for its decisions. They will also normally be published; however, the member has a right of appeal.

The Appeal Tribunal

A member or the Board may apply for a hearing before the Appeal Tribunal following a decision by a Disciplinary Tribunal. Like a Disciplinary Tribunal, this body normally sits in panels of three: two lay members and a member of either sponsoring body. The chairman of the Appeal Tribunal is legally qualified. The Appeal Tribunal may uphold, modify or overturn any finding of a Disciplinary Tribunal. Its decision is final within the process. Members can only appeal on the grounds that:

- there has been a misapplication of the relevant rules and/or the relevant law;

- the findings or sanction(s) were unreasonable; or

- new evidence has become available which, had it been available earlier, would materially have affected the original findings.

The appeal request will first be considered by a Disciplinary Assessor to ensure that the appeal comes within the specified grounds. If permission to appeal is granted, the case will be heard by an Appeal Tribunal.

Conclusion

The TDB is there to ensure that there is a fair and independent investigation of every complaint referred to it and also to ensure the fair treatment of any member against whom a complaint is made.

The good news, as you would expect, is that the number of referrals to TDB is low. Therefore, if you conduct yourself in a professional manner you are unlikely to be exposed to the disciplinary process.

The disciplinary rules and procedures exist to protect the public. In so doing, they also protect members. Equally importantly, they enhance the standing and reputation of the tax profession and as a member of that profession this is advantageous to you and your fellow members.

The TDB aims to ensure that all complainants are treated fairly. If you are unhappy with the way your case has been handled, you may complain to the Board who will review the case.

Help and support

A referral to the TDB can be a stressful experience. Members can contact the Professional Standards team at [email protected] or [email protected] to discuss any aspect of the professional standards rules and guidance. While they cannot comment on the particulars of a case, they can explain how the rules should work in practice.

The Members Support Service (tel: 0845 744 6611), which aims to help those with work related personal problems, can also provide a listening ear. An independent, sympathetic fellow practitioner will listen in the strictest confidence and give support.

Part One of this series, ‘Facing a complaint’ by Heather Brehcist, was published in Tax Adviser in October 2019.