Providing support

Share this article

Catherine Rosell considers the areas in professional standards that in-house members of CIOT and ATT may need extra support

Key Points

What is the issue?

Recent years have seen increasing compliance and self-certification requirements that have been introduced through legislation.

What does it mean to me?

All members of the CIOT and ATT are bound by a number of rules and regulations, like Professional Rules and Practice Guidelines (PRPG), Professional Conduct in Relation to Taxation (PCRT), PII and CPD Regulations, CCAB Anti-Money Laundering Guidance, Money Laundering Regulations 2007 Registration, Monitoring and Compliance Scheme and the Taxation Disciplinary Scheme.

What can I take away?

This article examines areas that a recent working party considers that in-house members need support in. We recommend members consider these areas carefully.

All members of the CIOT and ATT are bound by Professional Rules and Practice Guidelines (PRPG), Professional Conduct in Relation to Taxation (PCRT), PII and CPD Regulations, CCAB Anti-Money Laundering Guidance, Money Laundering Regulations 2007 Registration, Monitoring and Compliance Scheme and the Taxation Disciplinary Scheme.

The CIOT and ATT websites have areas dedicated to professional standards as they apply to members in commerce and industry, which can be found on the CIOT and ATT websites.

A working party, consisting of several members employed in commerce and industry as well as members of the CIOT and ATT Joint Professional Standards Committee, was brought together in 2017 to discuss the differing pressures faced by these members. Through those discussions, the team determined in their experience the key matters affecting in-house members and where they may require additional support. The increasing compliance and self-certification requirements that have been introduced through legislation in recent years were considered as well as practical everyday matters specific to a role in commerce and industry. In addition, although the rules contained in Professional Rules and Practice Guidelines (PRPG) and Professional Conduct in Relation to Taxation (PCRT) apply equally to all members, much is practice-specific and therefore the Committee wished to produce clear guidance on how to deal with particular situations that is focussed specifically for members in commerce and industry.

Some of this guidance is reproduced in this article but is representative only and should not be relied upon in isolation; the full guidance, which has been approved by the Professional Standards Committee and, where relevant, reviewed by Legal Counsel and discussed with HMRC, is available in the professional standards area on the CIOT/ATT websites.

Senior Accounting Officer

The Senior Accounting Officer regime (SAO), introduced by FA 2009, is a particular focus for members employed in commerce and industry. Many of our members, if not the SAO themselves, may report to the SAO or otherwise be required to provide assurance to their organisation’s SAO of that systems and processes are appropriate for tax reporting purposes, or, if they are not, what the business is doing to address any issues that might exist. The emphasis of the SAO legislation is to change behaviours within companies to ensure tax accounting arrangements are fit for purpose and to improve compliance across a number of regimes. It involves people, policies and processes from end to end within the business. As a result of this legislation, tax has had to be brought onto the agenda of company board meetings and has generally raised the profile of tax in businesses within the regime.

The guidance document produced by the working party collates the available HMRC guidance with our collective experience of implementation and monitoring of a control framework to produce a suggestion of what good practice would look like in this regime.

A factor that can influence how a company approaches SAO compliance is the decision regarding who the SAO should be. The legislation identifies the relevant person to be the director or officer who has overall responsibility for the company’s financial accounting arrangements. In some organisations this may be the CFO or the Finance Director who sits on the Board. In others, particularly larger organisations, there may be several SAOs. The SAO needs to be in a position to influence what happens within the company, but there needs to be a balance between their responsibility and influence and their understanding of the detail of the risk and control framework. For this reason, there may be several SAOs, with the assurance requirements cascading throughout the organisation, so that the whole business is working to meet the SAO requirements. The responsibility in relation to certification to HMRC cannot, however, be delegated and this can help maintain a high profile for tax within the organisation where the SAO is a senior officer or director or sits on the Board.

Publication of tax strategy

This self-certification is further extended by the requirement for qualifying large businesses to publish their tax strategy, another move by HMRC that has brought tax to the attention of UK Boards. The HMRC guidance is prescriptive in setting out what HMRC expects organisations to disclose within the published strategy as well as how it should be disclosed. Further, the tax strategy should be approved by the organisation’s board of directors and be in line with the overall strategy and operation of the business.

Thus the publication of the strategy can be seen as a way of improving the transparency of businesses in relation to their tax affairs and is designed to describe to HMRC and other stakeholders the tax risk appetite of the organisation’s leadership. The full HMRC guidance is available on GOV.UK.

Operational considerations

As well as high level strategic changes in relation to taxation, certain operational situations have also been identified that either give members working in commerce and industry cause for concern or where they have indicated they would welcome guidance. Frequently asked questions raised by members in commerce and industry have been addressed by the committee in the form of an FAQ document, in which the answers follow closely the approach in PCRT but have been drafted with a specific focus on members in the commerce and industry workplace.

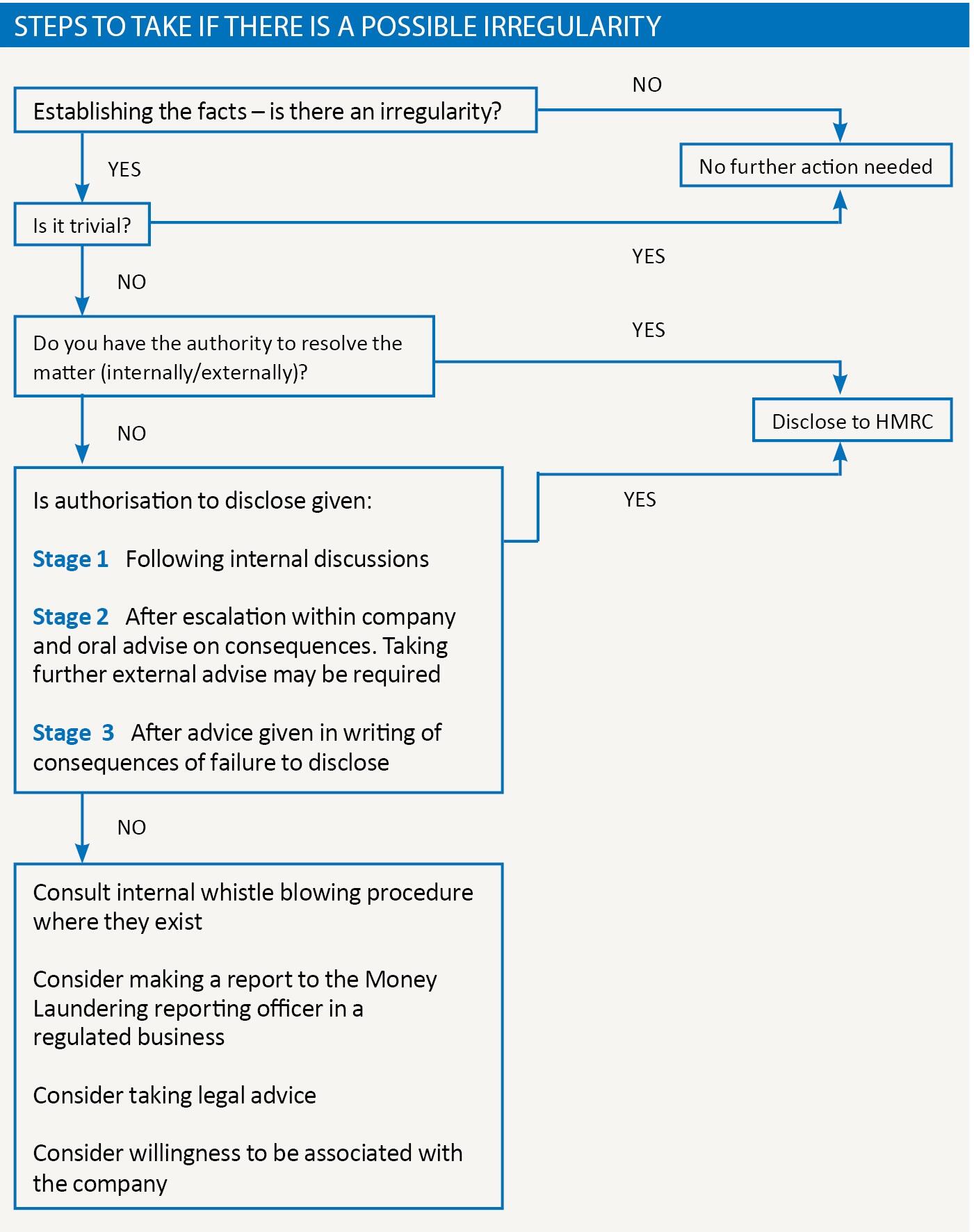

Irregularities

Of particular concern is what a member should do if they find an irregularity in the company’s tax affairs, or if they disagree with the tax technical position adopted by a colleague. For a member in practice facing a similar situation in relation to a client, where all attempts to reach agreement or resolution have failed, they may consider whether to cease to act for that client. For an in-house member this may not be a practical solution. Although in extreme circumstances they may consider whether they wish to remain associated with the organisation, they may not be in a position for financial or other reasons to be able to leave the business entirely.

‘Irregularities’ in the context of the document is intended to include all errors whether the error is made by the member, senior colleagues (including the SAO where relevant), junior colleagues, an external adviser, HMRC or any other party involved in the company’s tax affairs or tax accounting records.

An irregularity may result in the company paying too much tax or too little tax, or may result in inaccuracies in the SAO’s certificate on tax accounting arrangements. In any case the member should first consider their responsibilities under PRPG and PCRT and must act correctly from the outset. A flowchart setting out the steps a member should take if there is a possible irregularity is included within the guidance note and should be read in conjunction with the commentary that follows it in that note and referred to within the flowchart.

Differences of opinion

‘Differences of opinion’ refer to circumstances where there is internal disagreement within the organisation regarding a technical or procedural issue. Where there is a difference of opinion on an irregularity the member should refer to the circumstances where colleagues may each consider they have a tenable position on the way to proceed, for example, differing interpretations of the legislation.

As with irregularities, different opinions may significantly increase or decrease the company’s tax bill, in which case the member should work with colleagues and the company’s professional advisers to establish the correct technical position and the approach to be adopted. This is the case whether senior staff disagree with more junior staff or vice versa. On occasion it may not be possible to resolve a difference of opinion, in which case the guidance sets out how the member should proceed. In all cases, and as with irregularities, it is important to establish the facts, confirm company policies and procedures that may cover the position and discuss with senior colleagues, escalating within the organisation as necessary. Should the member consider their own position is at risk, they should consider taking specialist legal advice.

Advising in a personal capacity

The final section of the commerce and industry-specific guidance discusses what members should do if they are approached by colleagues to request advice relating to their personal tax affairs. Generally, members employed as in-house tax advisers are responsible for the tax compliance affairs of the employer and not those of the organisation’s employees. Occasionally, staff within the company who are aware of the member’s tax knowledge will ask for assistance with matters that may or may not be related to their employment.

While a member is not obliged to give advice in a personal capacity and, in fact, in most situations it is likely to be prudent to decline, should the member agree to do so they should ensure they are fully aware of the obligations upon them even if providing advice for no consideration.

Points to consider, as well as the fundamental principles contained in PRPG and PCRT that apply to all members, include:

- whether they are qualified to give the advice requested;

- whether their employment contract permits them to give advice in a personal capacity;

- whether they have suitable insurance cover provided by their employer.

If giving advice on a paid basis outside their usual employment the member should ensure they comply with the relevant PII and AML obligations.

The full document and detailed guidance for these frequently asked questions is available here for CIOT and here for ATT.