Public tax transparency

Share this article

Dr Christian R. Ulbrich and Charalambos Antoniou describe how to establish trust in the increasingly transparent world of tax, and share an insider’s view from Carl Emanuel Schillig

Key Points

What is the issue?

The general trend towards a much more transparent world of tax is leading us towards a debate around public tax disclosures. The public tax transparency topic is gaining strong momentum.

What does it mean to me?

This topic will add another dimension to the role of the tax function. An integral part of its role will be to provide support in developing a clear internal and external tax communication strategy and managing potential reputational risks.

What can I take away?

In an increasingly transparent tax environment, public tax transparency should be considered as an appropriate strategic response.

The 2007/08 financial crisis has prompted increasingly close scrutiny of the tax affairs of large corporations and ongoing efforts to broaden the tax reporting requirements for individuals, multinationals and intermediaries.

Examples of additional tax reporting requirements for individuals include FATCA and the Common Reporting Standard for the Automatic Exchange of Information (AEOI). We have now seen new reporting obligations for multinationals, e.g. country by country reporting to tax authorities (CbCR under the BEPS Inclusive Framework) in over 50 countries, as well as for intermediaries and taxpayers, e.g. the EU’s DAC6 tax disclosure rules.

The EU’s proposal for the mandatory publication of something closely resembling the CbCR submitted to tax authorities is still under discussion. Specific sectors, including the extractive industries and banking, are already required to publicly disclose certain country by country information. Some jurisdictions, including Australia and the UK, are even further ahead when it comes to aspects of tax transparency rules.

Tax administrations and other stakeholders are also gaining more insights by way of a growing number of tax-related leaks (including the Offshore Leaks, Lux Leaks, Panama Papers, Bahamas Leaks and Paradise Papers) and many other new sources of data opened up by digital technologies. We’re seeing an increase in the exchange of data and information between tax administrations, as well as endeavours to impose real-time reporting and analysis requirements, particularly in emerging markets.

Some major investors are cottoning on to the theme (see ‘Tax and Transparency’ by Norges Investment Management). Frameworks such as the UN supported Principles for Responsible Investment and the Global Reporting Initiative (GRI) are including tax transparency within their scope. The topic is also being pushed by industry-owned action groups such as The B Team Responsible Tax Principles. In addition, studies are investigating the nature of tax payments, commissioned by NGOs and politicians to back up calls for greater tax transparency.

We strongly believe that all these developments are indicators of a general trend. As better analytical tools and even more digital data become available, we predict that the world of tax will inevitably become much more transparent, with tax authorities themselves evolving in the very near future. Digitalisation in general has often gone hand in hand with greater transparency, so it’s reasonable to assume that the same will apply to tax.

As result, the role of the tax function will change in the future. Unfortunately, managing technical tax risks well and ensuring that an organisation is complying with the rules is no longer sufficient. It’s time for the tax function to join forces with other functions within the organisation to start promoting its endeavours and the financial merits of the whole organisation to external and internal stakeholders. As part of its new role, the tax function has to provide support in the development of a tax-related communications strategy and the management of reputational risks.

Public tax transparency is about participating in the debate. If you want to do so, the time for action is now.

What is public tax transparency?

Public tax transparency isn’t just about disclosing how and where a company pays taxes. This information must be put in the right context.

A company’s contribution isn’t limited to corporate income taxes (which are often only a small part of the taxes collected and paid by a company).

The notion of tax contribution can also be construed to cover other income and non-income related taxes, including payments to governments in the form of duties, levies and royalties. Companies collect and administrate taxes related to their staff, customers and suppliers on the government’s behalf. The notion of public tax transparency can even be extended to include the additional economic contributions a company makes to the economies in which it operates by way of wages, investments and payments to local suppliers.

Public tax transparency involves preparing the relevant information so that it’s easily and quickly accessible. Statements should be presented in such a way that the target audience can understand them without further explanation. Taking all these factors into account, a better definition of public tax transparency would be ‘presenting easily understandable information on the broader economic contributions that taxpayers make by paying or collecting taxes in the environment in which they operate’.

It’s important to realise that the actual content of what is reported in the context of public tax transparency will vary from organisation to organisation. Each company has to think strategically about what exactly it wants to disclose, what points it intends to stress, and the specific context in which to set the data. Depending on your organisation’s needs and situation, it’s crucial to find the right focus and balance.

In general, public tax transparency might include your total tax contribution(s), a sound global tax strategy, your approach to technical and non-technical tax risks, and information extracted from the CbCR.

Why is public tax transparency important?

The benefits that an organisation gains from greater public tax transparency depend on its particular profile and circumstances. Some companies are in very different positions than others; first, decide if public tax transparency is even appropriate.

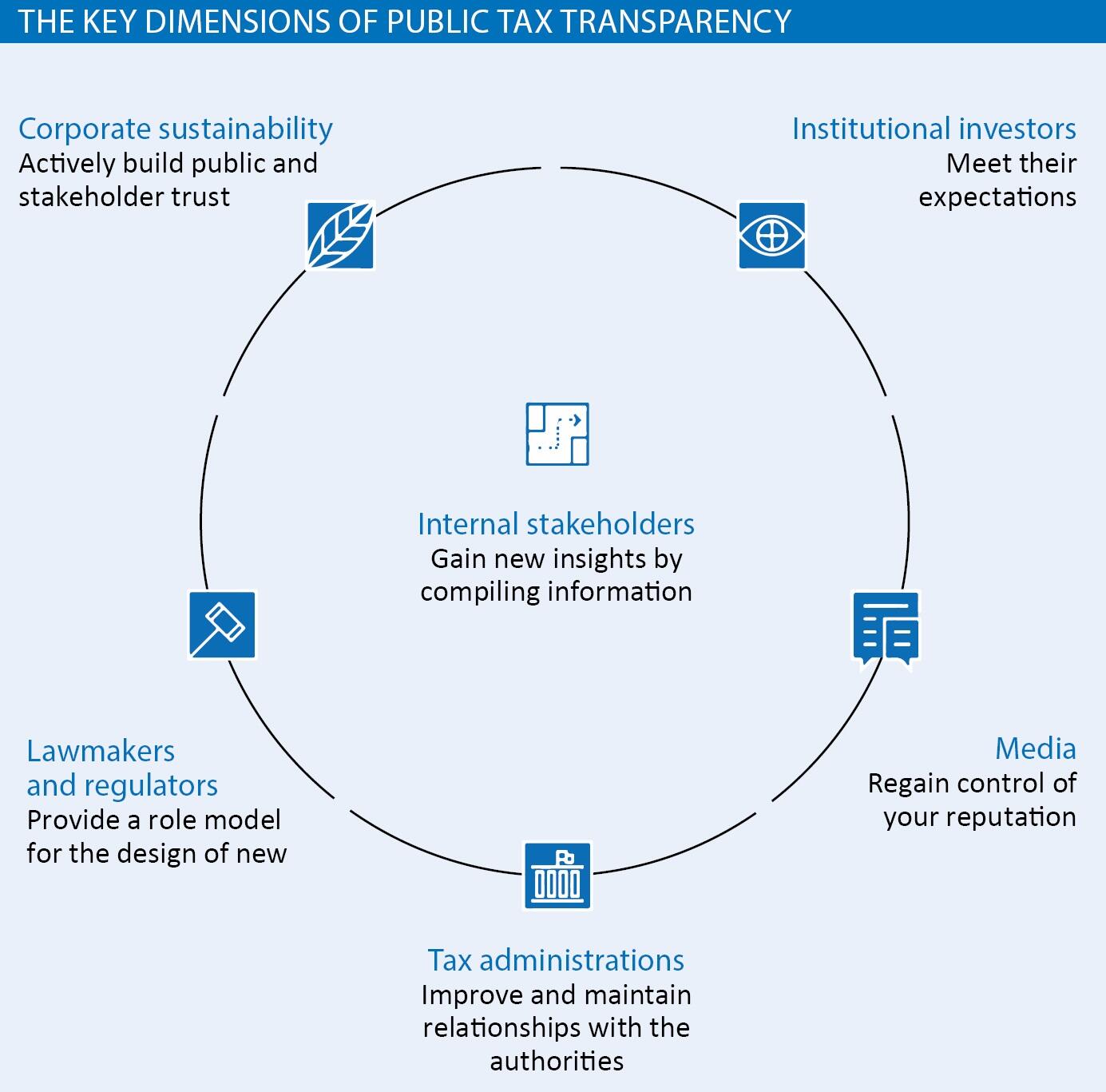

That said, we believe that public tax transparency can be very beneficial – in more ways than might be thought. We have identified five key dimensions (see diagram ‘The key dimensions of public tax transparency’) where public tax transparency will most likely be in your company’s direct interests in dealing with external stakeholders, plus a sixth dimension where you will indirectly benefit from the additional extracted tax data for preparing the report.

Conclusion

We are convinced that there is a new, digital and increasingly transparent world of tax just around the corner. Companies should be seriously considering whether to take steps to meet this more transparent tax environment and develop a strategic response.

Defining a smart approach to public tax transparency that matches each organisation’s circumstances may be part of this.

Interview: Carl Emanuel Schillig, Group Tax Director, Zurich Insurance Group

In March 2019, Zurich Insurance Group published a tax transparency report for the first time. How does it feel to become tax transparent?

Actually, it feels good. I’m thankful for the opportunity to disclose comprehensive tax-related information in the way we thought made most sense. It’s also a good feeling to be leading a global trend that’s here to stay.

Has Zurich received any negative media coverage of its tax affairs? Was this your motivation?

No, not at all. Negative media coverage wasn’t what drove us. The drivers were completely different.

So can you tell us then what the main drivers of this decision were?

We believe it is important that Zurich, as a provider of insurance coverage, acts as a responsible corporate citizen. This means that Zurich is committed to being a responsible taxpayer and, as such, a supporter of economic and societal development in the communities where it operates. We see the increase in tax transparency as part of our sustainability effort.

Also, we identified a clear trend towards more transparency and took the decision to stay ahead of the curve. In the last few years, we’ve observed many regulatory changes, all of which increase transparency. Initially, it was mainly individuals that were targeted, with FATCA and CRS. This soon extended to multinational companies with CbCR, the preparation of master and transfer pricing local files, and the publication of the tax strategy. Sooner or later, I expect that there will be further public reporting requirements.

We wanted to pre-empt this development and take advantage of the freedom we currently have to present the facts in a more holistic way that better reflects Zurich’s approach to sustainability.

Why did you decide to go live now?

In addition to the idea that we wanted to do something, we realised that institutional investors were getting increasingly interested in the topic. I guess that in the end, the letter sent out by Ethos Foundation in November 2018 created the necessary momentum to tip the scales.

When and how did you first come across the concept of public tax transparency? What was your reaction at that point?

That was already a couple of years ago. After the financial crisis of 2007/08, the whole debate about companies not paying their fair share of taxes started. I was sure that this debate wouldn’t just disappear again and, instead, would trigger requests for additional public tax disclosure. After a while, the first multinationals started extending their annual reports and disclosing information in greater detail.

I knew I also wanted to contribute to the debate. Finally, I realised that the best way to counter accusations of not paying your ‘fair share’ is to point out what you are really paying in taxes totally.

What features of tax transparency are important for you? Is there some aspect in particular you want to emphasise?

Besides illustrating the dimensions of the total tax contributions we make and how we support economic and societal development, for me it’s particularly important to disclose the tax strategy we have here at Zurich. The tax strategy is supervised by our Board of Directors and executed by the Group Executive Committee. We want to show our commitment to be a responsible taxpayer and complying with regulations in the countries we operate in.

Saying that, I want to stress that I have doubts about CbCR being a meaningful document if externally published. It’s very open to misinterpretation by people without a proper tax background, and it only tells part of the story.

What advantages do you expect? Is public tax transparency designed to address any stakeholders in particular?

For us, a particularly important group of stakeholders is institutional investors. I’m convinced that becoming publicly tax transparent will help us further strengthen their trust and confidence in our company.

We assume it was quite a ride beginning the day you decided to become publicly tax transparent until the day of publication this March. Can you describe the process? What were the milestones?

The first challenge we faced was to collect the necessary information. We had to persuade the local teams to collect information that they weren’t used to and not obliged to report in such detail for the consolidated Group IFRS accounts. Another important step was to consolidate the information we received. Only then could we start to generate the report.

The final report contains a lot additional information beyond reporting tax figures, and it’s not just a product of the tax department. It’s the result of intense interdisciplinary collaboration with other teams like Investor Relations, Communications and Sustainability.

Have you established an automated process to support your disclosures?

Yes. Though we started with Excel sheets, we finally managed to feed the information into our finance consolidation tool. This automation resulted in an efficient and effective data collection process.

Do you think that you’re spearheading a general trend? Will all major multinationals soon become publicly tax transparent?

As I said at the beginning of this conversation, I’m convinced that we’re leading a global trend. When I talk to my peers, I see this topic is hot, and more and more of them are interested in learning from our experience.

Was this step controversial within Zurich Investment Group?

Not as such. The board had been familiar with the topic for several years. From the beginning, we all agreed on the direction of travel. The discussions we had were more about the type and granularity of information we wanted to release, and how we could make sure that the information was disclosed in a meaningful way.

Finally, are there any steps you’re planning next?

I’m convinced that tax transparency is here to stay, and that it will even evolve in the coming years. We at Zurich Insurance Group will be carefully monitoring these developments and will act as ambassadors, advocating to a broader public the benefits of tax transparency.