Purchase of own shares and multiple completions

Share this article

Peter Rayney looks at multiple completion buy-backs and the potential ER risk

Background

Company share buy-backs are frequently used as an important tool in succession planning. Typically, the owner manager will sell all his shares back to the company under a purchase of own shares (POS) transaction, leaving the next generation or the senior management team in place as the new owners.

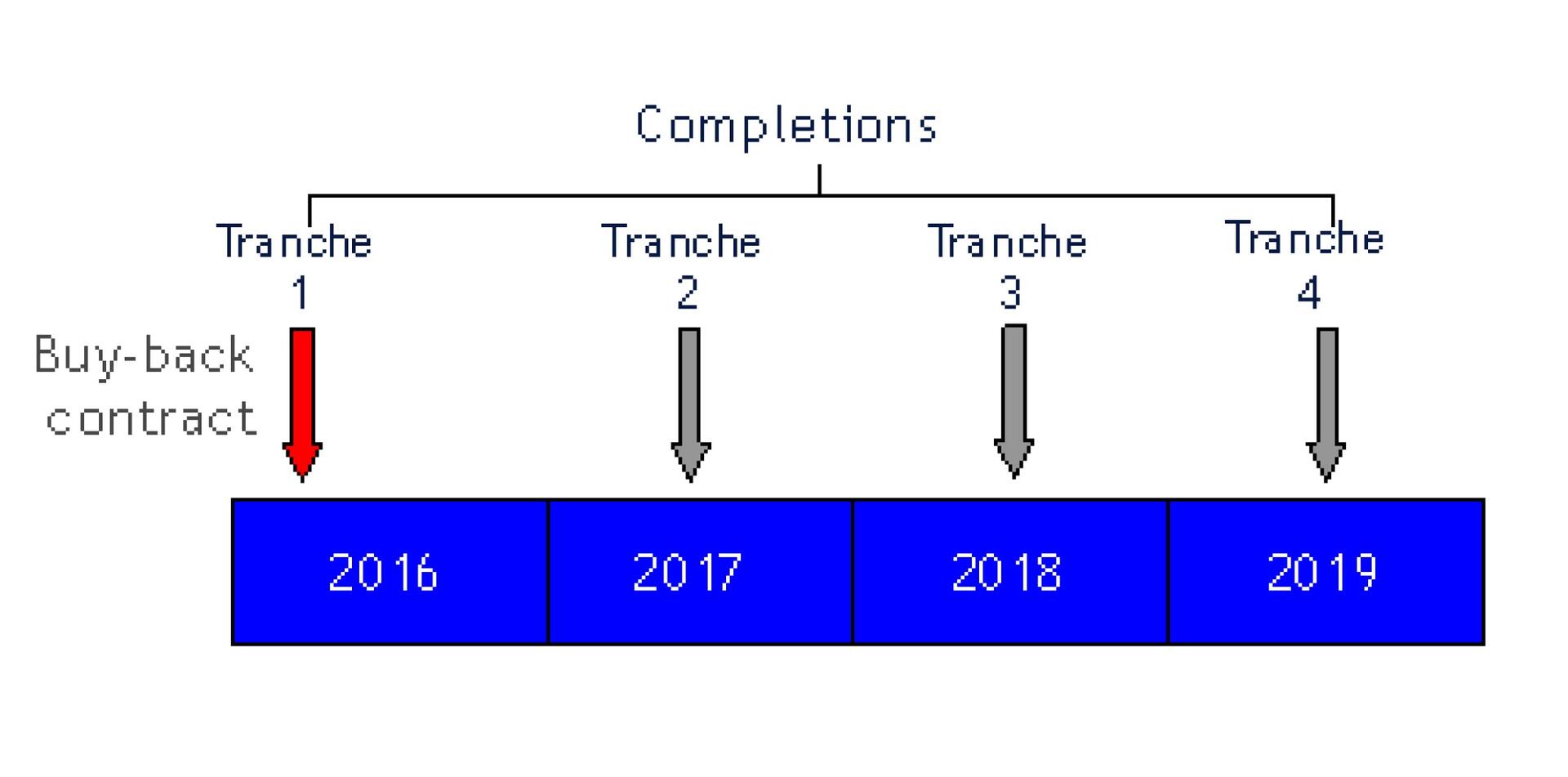

Financing a POS is not always easy. Company law demands that the purchase price for the shares bought back by the company is paid immediately (S691 (2), Companies Act 2006). It is not therefore possible for a company to buy-back its own shares for a deferred consideration. However, because of the (often) substantial sums involved for the POS consideration, many owner managers have used the ‘multiple completion’ mechanism. Broadly speaking, a multiple completion POS agreement involves the owner manager contracting to sell their shares back to the company, but with the legal completion of the buy-back subsequently taking place in tranches, as illustrated below:

A multiple completion contract enables the company to finance the purchase price over a number of years out of its (surplus) trading cash flows. Provided it is properly structured and implemented this mimics a ‘deferred consideration’ deal whilst remaining compliant with company law.

Prevailing tax treatment

In carrying out multiple completion deals, tax advisers still place reliance on the (then) Inland Revenue ruling in 1989. In a statement the Inland Revenue confirmed its agreement to a POS being made in instalments, as reported in the ICAEW technical release 745 issued in April 1989.

Para 10 (b) of the release states:

‘‘They [the Inland Revenue] take the view that as the beneficial ownership of the shares is regarded as passed at the date of the contract, a disposal for capital gains tax purposes will have taken place by the vendor at that time notwithstanding payments at later dates.’’

Practical experience has also shown that HMRC has generally given POS tax clearances under s1044, CTA 2010 for properly structured POS multiple completion deals.

Hitherto, tax advisers and HMRC has accepted the following technical analysis for a multiple completion POS:

- For CGT purposes, the disposal of the entire beneficial interest in the shareholding takes place at the date of the contract (s28, TCGA 1992). Importantly, this means that if the seller shareholder qualifies for the (‘no distribution’) ‘CGT’ treatment and also entrepreneurs’ relief (ER), the full amount of the POS proceeds should attract the beneficial 10% rate (but see possible change in HMRC’s stance below).

- Under the multiple completion route, the selling-shareholder gives up their beneficial interest in the repurchased shares on entering into the contract and therefore the ‘substantial reduction’ test does not apply. Thus, the seller cannot subsequently take dividends or exercise voting rights over the shares. Thus, since the ‘seller’ loses beneficial ownership of all the shares on entering into the contract, the various ‘connection’ tests imposed by s1042 and s1062, CTA 2010 are not in point.

- However, HMRC has always insisted that it is not legally possible to give up voting rights via the POS contract. If a shareholder still legally holds the shares, HMRC consider that they are still able to exercise their voting rights at a company meeting. Assuming this view is correct, the selling shareholder would be ‘connected’ with the company under CTA 2010, s 1062(2)(c) where the voting rights on the ‘non-completed’ POS shares exceed the 30% limit. However, if this is likely to be a potential issue, HMRC also accept that the problem can be corrected by converting the relevant ‘non-completed’ element of the shares into a separate class of non-voting shares.

- The subsequent ‘multiple completion’ of the POS of the remaining tranches of shares is simply a legal process and normally has no bearing for tax purposes.

Possible change in HMRC analysis

At the CIOT 2016 Autumn Conference, a leading tax barrister indicated that he was working on a case which involved HMRC denying a substantial amount of ER on a particular ‘multiple completion’ POS. HMRC have resisted the seller’s ER claim, by applying an entirely different tax analysis to multiple completion contracts, which goes against the hitherto accepted view outlined above.

It seems that HMRC is now applying a very literal reading of s28, TCGA 1992, which fixes the CGT disposal date. Section 28 applies where ‘an asset is disposed of and acquired under a contract’. HMRC’s argument is that there is strictly no acquisition under a POS. This point is not clear-cut, although we do tend to rely on this view when it comes to claiming a freely available capital loss on a POS! (Since there is no acquisition the ‘connected party’ loss rules should not apply – see s18 (3), TCGA 1992.)

Thus, if HMRC is right on the s28, TCGA 1992 point, then the ‘timing rule’ would not apply to the POS transaction. This means that the timing of the disposals would fall within ‘capital sums derived from assets’ legislation in s22, TCGA 1992. Consequently, under a multiple completion contract, a CGT disposal would arise each time part of the POS proceeds is received. Since the seller would have resigned as a director at the date of the POS contract, they would not be able to make a competent ER claim on the subsequent tranches of consideration received under a multiple completion POS. Under this analysis, the seller should be able to obtain ER when the initial tranche is paid (since this will normally be received at the date of the POS contract. The remaining tranches are likely to suffer CGT at 20%.

Unfortunately, sellers will not be able to rely on obtaining a competent POS clearance under s1044, CTA 2010. This simply confirms that the amount payable to the shareholder under the POS transaction is not treated as a distribution (and is therefore subject to CGT). The clearance doesn’t provide any confirmation that ER is available.

Current advice on multiple completion POS deals

It must be remembered that this point has not yet been litigated. Most tax advisers would hope that an appellate tribunal would take a purposive view on the application of s28, TCGA 1992 and not seek to deny ER on a literal construction of the legislation. It is likely that this point was never even contemplated by the draftsman or indeed by Parliament.

Multiple completion POS deals do not involve any form of tax avoidance. The arrangements simply enable the company to ‘defer’ part of the purchase consideration in a ‘Companies Act’ compliant manner. In fact, under the conventional analysis, all the CGT is paid up-front on the basis of the contract date under s28, TCGA 1992- so where is the mischief in that!

However, tax advisers should take this development into account in structuring current multiple completion POS transactions. Until the s28 TCGA 1992 issue is settled, I suspect that more prudent advisers will either seek to implement a straightforward POS or a ‘Newco buy-out’. (A ‘Newco buy-out’’ will typically involve using a new company (‘Newco’) as the acquisition vehicle to buy-out the shares of the departing shareholder with the existing shareholders ‘swapping’ their shares under the share exchange rules in s135, TCGA 1992.) But what an unnecessary palaver!