R&D changes: why you need to act now

Share this article

Changes to how companies gain relief for their R&D expenditure start after 1 April 2024. However, failure to consider the commercial and practical implications of the changes may cause problems down the line.

Key Points

What is the issue?

Changes made to the UK R&D relief schemes, for accounting periods starting on or after 1 April 2024, will significantly impact many companies’ ability to claim relief for the R&D activities they undertake.

What does it mean for me?

The changes are expected to impact which company in a supply chain has the entitlement to the R&D tax benefit. Early consideration of commercial arrangements will enable companies to plan ahead and prevent surprises later on.

What can I take away?

HMRC’s intention is that the R&D reliefs are included in project planning and management. Companies that take time to consider how best to document and evidence their R&D claim will be at an advantage if an enquiry letter lands on their doorsteps.

After months of debates and discussions within the R&D tax community, the Autumn Statement and associated Finance Bill confirmed the details of the significant changes being made to how companies gain relief for their R&D expenditure. Most changes will apply for accounting periods starting on or after 1 April 2024.

There have been numerous articles and alerts published that set out the details of the changes, but they can be summarised at a high level:

- Under the new merged scheme, most claimants will gain relief as an above-the-line credit on the same activities as the existing schemes. The notable exception is the treatment of contracted out R&D work where the entitlement to claim now rests with the instigator of the R&D.

- Where a company’s R&D expenditure represents more than the applicable percentage of the company’s statutory profit and loss expenditure, they may choose to claim under the R&D intensive regime. The intensive regime is effectively the existing SME scheme using the same treatment for contracted out R&D work as the merged scheme and can only be accessed by loss-making SME companies.

- Overseas expenditure is generally excluded from both the merged and intensive regimes unless the conditions to fall within the exemptions are met.

Taken together, these changes are expected to push R&D claims up the supply chain from the companies whose staff undertake the R&D to those companies that plan, initiate and fund the R&D projects. This may well reduce the number of overall claims, particularly in service providers such as consultancies, contract R&D organisations, manufacturing and design specialists.

The recent changes bring the UK in line with many overseas jurisdictions, for instance the US and Australia, where historically more information has been mandated for claimants. Companies with R&D activities in these jurisdictions should consider whether already existing processes could be used in the UK.

This article now focuses on the practicalities of changes in the R&D schemes, the treatment of contracted out R&D costs, the restriction on overseas costs and the additional compliance needed to make a claim.

Move to the merged scheme and interaction with the intensive SME scheme

After many years of both the SME super-deduction and old R&D expenditure credit, the R&D regimes are well understood. Having two regimes has led to complexity, particularly for SME companies that may have made claims under both regimes, so a move to a single regime without the SME criteria appears to simplify the situation for most claimants. Designing the merged scheme so that it provides an above-the-line credit aligns with the desire to improve the visibility of the incentive to management teams beyond the tax function.

The effort needed to identify which costs can now be included in a company’s claim will mean that many claimants will not see the benefits of simplification immediately. There is also still complexity where a claimant is an R&D intensive company and has the option to claim under an amended super-deduction regime.

Although at first glance the ‘in year’ cash benefit appears higher under the R&D intensive super-deduction, it is important that companies model the benefit fully before claiming under the intensive scheme. There are circumstances where an R&D intensive SME may get a better ‘in year’ cash impact by claiming under the merged R&D expenditure credit due to their tax position. Similarly, the benefits of the immediate cash credit may not match the value of the potentially surrendered losses when future plans are considered.

Those claimants that decide to claim under the intensive scheme will need to prove their SME status as well as their R&D intensity. For many claimants, particularly those where evidencing their SME status is complex or those who would need to claim under both regimes, the marginal increase in benefit may not be worth the additional effort.

Contracted out R&D

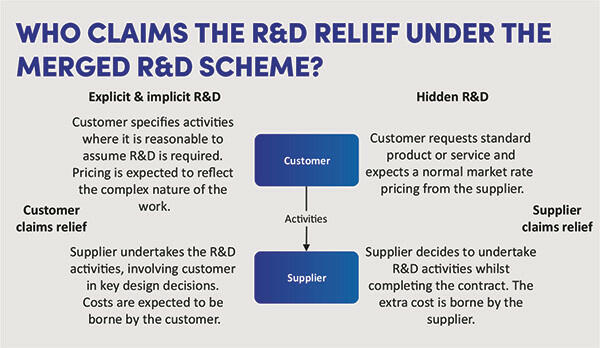

The determination of whether work meets the definitions to be eligible R&D has not changed. Where costs of R&D are contracted out, the new merged scheme moves from rewarding companies undertaking the R&D activities to those planning, initiating and funding it. R&D activities can now generally be split into four types:

- The company can claim for its expenditure on both in-house R&D work and payments for R&D that is intentionally contracted out.

- The R&D activities are contracted out to the company and the customer anticipates that R&D activity is needed. In this case, the company (supplier) doing the work cannot claim for R&D relief as the customer can make the claim.

- The R&D activities are contracted out to the company and the customer is ineligible to make its own claim for R&D relief; for example, the customer is an overseas entity so cannot claim, or is a group company which has elected to forgo its own claim.

- R&D activities are contracted out to the company where the customer is indifferent to the R&D. The company doing the work claims for R&D relief as the customer is not involved in the R&D.

The challenge will be identifying which projects count as contracted out R&D and who has the entitlement to make the claim. The current definition of contracted out R&D seeks to capture arrangements where there was an intention to contract out R&D at the time the contract was agreed. Many contracts will explicitly state that they include R&D. Other contracts will not mention R&D, but if the terms and surrounding circumstances make it reasonable to assume that the customer anticipated R&D would be required by the supplier (and any of its subcontractors) then these will also be captured.

Although Hadee Engineering Co Ltd v HMRC [2020] UKFTT 497 considered the meaning of contracted out R&D under the existing SME scheme, it may be persuasive when considering the meaning of contracted out R&D. The following factors influenced the judge’s decision when considering if activities had been contracted out to the company:

- The company was typically reimbursed on an hourly basis for its design time so no financial risk was borne.

- The customer provided the project concept and was heavily involved in the design.

- Commissions were for bespoke solutions and public information indicated that the work related to the customer’s pioneering processes.

What does this mean in practice for claimant companies? The actions needed are dependent on the company’s role, so taking the supplier and then the customer in turn the following issues arise.

Companies performing activities under contract (the supplier)

To claim R&D relief on activities it performs under contract, the onus will be on the company to show that the customer was indifferent to whether R&D would be undertaken at the time the contract was agreed; for example, showing that the contract pricing was based on it being routine activities (e.g. standard pricing and not for tailored or specifically bespoke activities). Retaining contemporaneous evidence of scoping and planning activities may also help to demonstrate that the level of technical customer involvement was relatively limited.

Companies should consider how their commercial teams communicate with customers, ensuring that it is clear what is being paid for and what the expectations associated with the offering are (i.e. can the work be agreed without meetings with the customer’s technical specialists or not).

Legal teams should be aware of attempts by customers to insert clauses asserting rights to R&D relief into contracts where there is no expectation in the customer negotiations that the project will involve R&D. Where a customer expects R&D to be undertaken so a supplier cannot claim the relief, the supplying company should consider their pricing structures, particularly where historically R&D relief has been used to increase the margin on customer projects.

Companies contracting out activities (the customer)

Historically, large companies have not been able to claim R&D relief in respect of R&D activities contracted out to third parties, so many companies will not have steps in their R&D claim processes to identify these activities and costs. The customer will need to show that they intended the supplier to undertake R&D, which should be evidenced through contemporaneous tender documents and contracts. Many suppliers will be used to claiming R&D relief for these activities themselves, so there will need to be discussions about the actual circumstances to agree where the entitlement to claim sits and any impact this has on pricing.

The legislation and explanatory notes are only concerned with whether a customer intends their supplier to undertake R&D at the time the contract is put into place. If a customer subsequently finds out that the supplier was undertaking R&D to fulfil the contract, then the customer will have no right to claim this ‘hidden R&D’. Companies may wish to rescope projects or include agreed phases in contracts if there is a significant likelihood of a change of scope leading to R&D activities being undertaken.

The biggest challenge for companies claiming contracted out activities is likely to be capturing the details needed to support their R&D claim, both the quantification and technical aspects. For large contracts, it may be necessary to consider inserting clauses providing that the supplier’s competent professionals will assist the company and its advisors with the R&D claim preparation. Equally, a company may consider asking the supplier to complete regular updates setting out the R&D activities, advancements and uncertainties and what proportion of the overall contract they represent. The ‘additional information form’ template might be used as a guide to the type of information that should be captured.

Supporting evidence

Currently, companies are not required to disclose details of their subcontractors on the additional information form, so there is no mechanism for HMRC to easily check whether double claiming has occurred. However, it must be anticipated that companies in sectors typically working under contract to others, such as consultancy, will be subject to high levels of HMRC scrutiny and will need to evidence their right to claim. Companies in these industries should keep contemporaneous records evidencing any discussions with customers demonstrating the agreed nature of the work.

The need for record-keeping was a point strongly highlighted in the recent ‘Guidance for Compliance 3’ guidelines for making R&D claims. If an enquiry is raised, HMRC may ask for all correspondence for a specific contract, as well as looking at publicly available information about the contract (e.g. in the Hadee case, HMRC referenced press releases by the customer).

Exclusion of overseas costs from the R&D regimes

The exclusion of most overseas expenditure has been well trailed, having first been broached back in Spring 2021. Guidance on the conditions for the exemptions that allow overseas R&D costs to be claimed has been promised by HMRC. It is not unusual for a company or group to have a mix of UK and overseas resources working on projects. In these scenarios there are several steps that could be taken:

- Companies should review their current claims to identify the level of overseas expenditure. It will be important to communicate the impact of this change to management for future investment decisions and financial management.

- Identify if there are readily available mechanisms for tracking the location of costs and how the claim methodology could be changed to incorporate this.

- Where it is believed the exemptions will apply, contemporaneous evidence should be kept regarding how the condition was met.

This evidence may include keeping:

- correspondence with regulatory bodies requesting overseas trials;

- evidence that the company sought a suitable location with the appropriate geographical conditions, but no such location exists in the UK; and

- documentation that shows the necessary facilities to undertake the R&D were not available and could not be reasonably replicated. For example, evidence of searches of existing geological survey data being undertaken or very specific equipment which cannot be reasonably replicated in the UK in the timescales needed.

Future updates to the additional information form

By now, many companies will have had their first experience of the additional information form and therefore will feel more comfortable about the details needed. However, there are more changes to come, as HMRC will update the additional information form once the restrictions on overseas expenditure come into effect.

From accounting periods starting on or after 1 April 2024, HMRC requires all entities to list the externally provided workers (the external resources who augment the company’s technical team) working on R&D activities, along with the staff provider’s PAYE reference, to confirm these individuals are UK based.

It is recommended that conversations are held with the staff providers about how to obtain this information sooner rather than later, as trying to get this information after a contract has been delivered may be challenging. If a company is unable to obtain the PAYE references of its externally provided workers, then HMRC will expect the associated cost to be excluded from the claim.

Prepare for the R&D changes

The design of the merged scheme and HMRC’s continued focus on the compliance process are all part of a wider drive to improve the cost effectiveness of the R&D reliefs by addressing the fraud and abuse that has been identified, and to respond to the criticism they have faced from the Public Accounts Committee, industry, professional bodies and advisers.

HMRC’s intention is that the R&D reliefs are not just a tax afterthought considered once year end is closed, but are also included in project planning and management. They are asking for more contemporaneous evidence, so it is clear that companies that take time to consider how best to document and evidence their R&D claim will be at an advantage if an enquiry letter lands on their doorsteps. This is a clear case where acting now will save time later and protect claim value.