Real estate structures

Share this article

Dominic Lawrance considers the tax implications of foreign domiciliaries buying UK real estate and looks at the different structures possible

Key Points

What is the issue?

Where a foreign domiciliary, non-resident or UK resident, is looking to buy UK real estate, what are the applicable tax principles and when does use of some kind of structure still make sense?

What does it mean to me?

An inappropriate structure may be very costly in terms of unnecessary taxes, and bad advice could result in a negligence claim.

What can I take away?

Broadly, use by a foreign domiciliary of a non-UK company to buy and hold UK real estate is likely to make sense where that real estate is commercial. Use of a company may make sense for residential property, but normally only where the property will be let to third parties on a commercial basis.

In recent years the amount of UK real estate in ‘foreign’ ownership has become a topic of political sensitivity. There have been successive reforms to the tax treatment of UK land, including land that is indirectly owned; with much of the legislation being directed, implicitly or in some cases expressly, at those resident and/or domiciled outside the UK. The piecemeal nature of these reforms has led to a legislative framework of great complexity.

An understanding of this framework, and possible further changes to it, is essential when considering how foreign domiciliaries should acquire/own UK land. This article considers the position for non-residents and also UK resident non-UK domiciled individuals (‘RNDs’), and addresses both residential and commercial property.

Home ownership structures under the hammer

Until now, the focus of this restless change has been residential property. The first measure was the introduction of a punitive 15% SDLT flat rate for corporate purchasers of dwellings, subject to reliefs for (inter alia) commercially let properties. This was followed in 2013 by the introduction of ATED, an annual wealth tax on dwellings held by companies. This tax is subject to a number of exemptions, in particular for properties let on a commercial basis to unconnected persons. In practice, the burden of ATED has fallen almost exclusively on non-UK resident, foreign domiciled individuals, who (at least until recent reforms) have typically used non-UK companies to purchase UK real estate, as a means of avoiding IHT exposure.

In due course, ATED was joined by ATED-related CGT and non-resident CGT (‘NRCGT’), taxes applicable on the disposal of dwellings by companies within the scope of ATED, or by other non-UK resident persons.

The enactment in 2017 of Schedule A1 to IHTA 1984 was widely seen as the final nail in the coffin of corporate structuring for UK dwellings. This generally ensures that non-UK situated assets that derive their value from UK dwellings, such as shares in a non-UK incorporated property holding company, are within the IHT net even for individuals who are foreign domiciled. This is so regardless of the use of the property; unlike ATED, IHTA 1984 Sch A1 does not differentiate between properties used by connected persons and those commercially let to third parties. Where UK residential property is concerned, the scope to use a company or other entity as an IHT ‘blocker’ has largely been eliminated.

Gains tax tackled, again

Yet further changes are being made with effect from April 2019. The Finance Act 2019 has significantly extended the territorial reach of UK taxes on gains realised on, or in connection with, UK real estate. There are two aspects to this:

- Non-residents without a permanent establishment in the UK can now be taxed on gains realised on the disposal of UK commercial property. Until now, such tax exposure has only existed with respect to UK residential property.

- There is now scope for a UK tax charge on a non-resident disposing of an asset that is not itself UK land, but derives all or most of its value from UK land – whether such land is residential or commercial. Clearly, this is aimed at shares and securities issued by property holding companies.

There are various rebasing dates, depending on the nature of the disponer and of the asset. Importantly, ATED-related CGT is being abolished, and for any company currently within the scope of that tax, any ability to rebase to April 2013 or 2014 is being lost. However, for the avoidance of doubt, ATED itself is being retained.

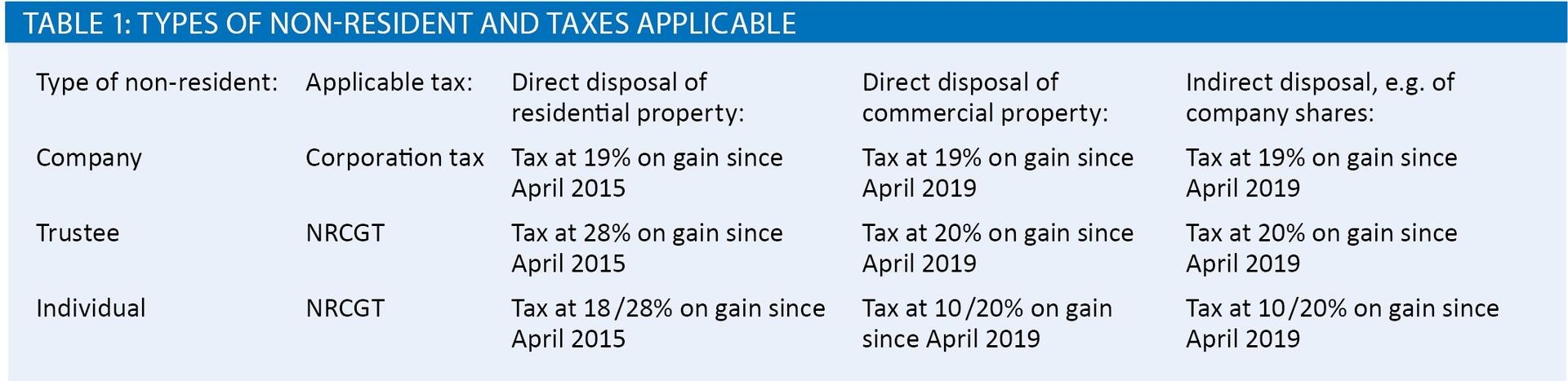

In very broad outline, the position from April 2019 is as shown in table 1:

Indirect disposals

The ‘all or most’ referred to above is shorthand for a more complex test set out in the legislation, contained in a new Schedule 1A to TCGA 1992. Broadly, the requirement is for the asset to derive at least 75% of its value from UK land, whether directly or through assets that themselves derive their value from UK land. It follows that a non-resident should not be taxed under the new rules on a disposal of an interest in a company whose value is represented, as to more than 25%, by assets other than UK land, and not deriving their value from UK land.

Moreover, the tax charge on indirect disposals will only apply if the person making the disposal has what the legislation calls ‘a substantial indirect interest’ in the underlying UK land. In relation to a company, the requirement is broadly that the person making the disposal has 25% or more of the voting rights, or an entitlement to 25% or more of a distribution or the proceeds of a liquidation. This requirement must be met at some point in the period of two years running up to the date of the disposal.

These conditions might suggest that the tax charge on indirect disposals under TCGA 1992 Sch 1A will be rather easy to avoid. However, the legislation includes a targeted anti-avoidance rule, that allows a GAAR-style counteraction of a tax advantage achieved through arrangements which have the sole or main purpose of causing a provision of TCGA 1992 Sch 1A to apply or, conversely, not to apply. It is easy to see great uncertainty being created by the sweeping and vague drafting.

There are two further points of note in relation to indirect disposals:

- The legislation provides no relief from economic double taxation. There is scope for the same economic gain to be taxed twice if a non-resident shareholder disposes of his shares, realising a post-April 2019 gain on which he is taxable under TCGA 1992 Sch 1A, and the company then disposes of the property, realising a gain which is taxable on the company. Indeed, there is scope for the same economic gain to be taxed many times over, e.g. if a multi-tiered corporate structure is simplified through the liquidation of holding companies.

- Non-resident trustees and individuals realising post-April 2019 gains caught by TCGA 1992 Sch 1A, in respect of indirectly-owned residential property will be taxed on such gains at ordinary rates, instead of the elevated rates that apply to residential property gains. This might be thought anomalous.

And there’s more

The process of amendment will not stop here. The Government has announced an intention to amend the rules on UK property income with effect from April 2020, so that from that date any such income accruing to a company will be within corporation tax. Currently, rental income of a non-UK resident company is subject to basic rate income tax in the company’s hands. Somewhat perversely, this change may, if it goes ahead, provide something of a tax break for non-resident corporate landlords, as the basic rate of income tax is 20%, whereas the Government intends to reduce the corporation tax rate to 17% in 2020 /21.

On top of this, the Government is currently ‘consulting’ on a 1% SDLT surcharge for non-UK resident purchasers of UK land, which according to the consultation document ‘will be legislated for in a future Finance Bill’. As is so often the case, the use of the future tense, rather than the conditional, says much about the nature of the ‘consultation’. It appears that a corporate purchaser of UK land will be treated as non-UK resident for the purposes of the 1% SDLT surcharge if it is non-UK resident for corporation tax purposes, or if it is UK resident for such purposes but is closely held and under the direct or indirect control of non-UK resident persons. It is unlikely to be possible, therefore, for a non-UK resident to avoid the surcharge by creating a UK resident company to purchase UK land.

Where will it end?

The regime for the taxation of UK land is clearly in a state of evolution, and it is hard to know whether we are nearer the beginning or the end of the process. The Finance Act 2019 may represent the first phase of a programme to align the tax treatment of UK residential and commercial property. Obvious questions are whether in coming Finance Acts, further steps will be taken in this direction, and whether further measures will be taken to eliminate tax advantages that are currently available through the use of corporate vehicles.

As matters stand, there are still some differences between the treatment of UK residential and commercial property, and between direct and indirect holdings. In particular:

For non-UK domiciled individuals, who are not deemed domiciled, there is a huge difference in the IHT treatment of UK residential and commercial property, if held via a company whose shares are non-UK situated. If the property is residential, the shares in the company are within the IHT net, under IHTA 1984 Sch A1. That is not currently the case for non-UK situated shares in a company where the property is commercial; such shares still qualify as excluded property in the hands of a non-UK domiciled, and non-deemed domiciled individual. It would not, however, be surprising if this difference in treatment was eliminated in due course. From a drafting perspective, extending IHTA 1984 Sch A1 to cover commercial property would be easy.

Sales of UK real estate obviously attract SDLT. By contrast, shares in non-UK incorporated companies, with non-UK share registers, can in principle be sold without any UK duty, even where the company’s sole asset is UK real estate. Companies are not currently ‘transparent’ for SDLT purposes. However, it is conceivable that this too will come to be seen as a missed opportunity, and that SDLT will become chargeable on indirect land sales.

What structuring is still possible?

Foreign domiciliaries who are looking to acquire UK real estate now can only sensibly act on the basis of what the law currently is, coupled with future measures which are known to be in the pipeline. Taking that approach, the first question is whether there are any situations in which it may make sense for a foreign domiciliary to use an entity to acquire UK land. The second question is whether there are other situations in which, if UK land is already held by an entity, there is benefit in it being retained.

As noted above, there are still significant differences between the treatment of UK residential and commercial property. IHT avoidance through the use of a property holding company is still possible where the underlying property is commercial. The shares in such a company are excluded property in the hands of a non-UK domiciled and non-deemed domiciled shareholder, provided that as a matter of general law those shares are non-UK situated (e.g. on the basis that they are registered, and the register is kept outside the UK). In addition, the penal 15% SDLT rate for corporate purchasers of UK residential property is inapplicable to commercial property purchases.

These points mean that, under current law, there is a strong argument in favour of a non-UK domiciliary, who is not deemed domiciled, using a non-UK incorporated company to acquire UK commercial property, so that the value of the property is shielded from IHT. Going forward, it is unlikely to make much difference to the overall tax analysis whether the company is resident in the UK, under the central management and control test, or not. However, for an RND, it may be preferable for the company to be managed and controlled from the UK, so that there is no possibility of the company’s income/profits being attributed to him under the transfer of assets abroad legislation.

By contrast, where UK residential property is concerned, the argument in favour of using a company to purchase the property is at best more subtle, and at worst non-existent. There may be an advantage where the property will be let to third parties on commercial terms, or will be redeveloped, so that the 15% SDLT charge will not apply to the purchase, and relief will be available from ATED, and subsequent rental profits or redevelopment profits will benefit from the (currently) attractive UK corporation tax rate, instead of personal income tax rates. But it is hard to make any kind of case in favour of creating a company to buy and hold residential property that will be used by the shareholder or connected persons. The 15% SDLT charge, ATED and the absence of IHT protection together make an expensive cocktail.

When it comes to UK residential property that is already held by a company, the question of whether it is preferable to buy the property or the company can be complex. The scope to avoid SDLT on the purchase is obviously attractive, despite the risks and extra transactional costs involved in buying a second-hand company. Where the foreign domiciled individual elects to buy the company, with the object of using the property personally, there are usually strong arguments in favour of collapsing the company after the purchase, so that the property is held directly. These include elimination of ATED and avoidance of possible benefit in kind charges if the individual is deemed a shadow director.

However, here too the tax and other considerations can be complex, and need to be weighed carefully. For example, if the company has been purchased by a RND, could the liquidation of the company result in a remittance of funds used to make the purchase? The adviser really does need to have done his or her homework.