Registered pension scheme reforms: abolition of the lifetime allowance

Share this article

Following the announcement of an increase in the annual allowance and the abolition of the lifetime allowance, we consider what the changes will mean for pensions.

Key Points

What is the issue?

In the Spring Budget on 15 March 2023, the chancellor announced an increase in the annual allowance and, more surprisingly, the abolition of the lifetime allowance.

What does it mean for me?

Where an individual starts to take their pension benefits after 5 April 2024, and the values are less than the lifetime allowance, the new regime will seem very similar to the old. For those who crystallise benefits both sides of 5 April 2024 it may be more complicated, and require far closer analysis, particularly if they have some older protections.

What can I take away?

The transition will also have major consequences for pension providers who will not only need to adjust to a new regime quickly but are expected to provide statements to members by 5 April 2025 where benefits were taken under the old regime.

The tax landscape for UK registered pension schemes has been evolving rapidly since the Spring Budget on 15 March 2023, when the chancellor announced an increase in the annual allowance and, more surprisingly, the abolition of the lifetime allowance.

The government’s stated aim was to encourage workers over 50, such as those in the NHS, to remain in work. The annual allowance reforms were straightforward and took effect from 6 April 2023. The lifetime allowance remains in force throughout the 2023/24 tax year, but the lifetime allowance charge ceased to apply from 6 April 2023. The lifetime allowance itself is intended to be abolished from 6 April 2024 with two new allowances introduced in its place.

Reforms affecting the 2023/24 tax year

Annual allowance

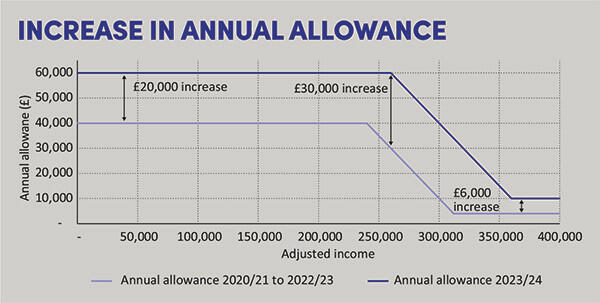

The chancellor announced at the Spring Budget that the annual allowance would increase from £40,000 to £60,000 from 6 April 2023, with a corresponding rise in the adjusted income limit, the point from which taper applies, from £240,000 to £260,000 (the £200,000 threshold income limit is unchanged). Additionally, both the minimum tapered annual allowance and the money purchase annual allowance were increased from £4,000 to £10,000. These reforms were legislated in Finance (No.2) Act 2023 ss 20-22.

Taxpayers at all income levels have higher annual allowance capacity, with up to £30,000 extra available compared to 2022/23, as demonstrated in the chart Increase in annual allowance.

As the changes in limits only affect the annual allowance from 2023/24 onwards, the old limits remain relevant until 2025/26 for the purposes of the annual allowance carry forward rules.

Lifetime allowance charge

The lifetime allowance remains in force for the whole of 2023/24. It therefore continues to operate as normal when determining the availability and quantum of certain lump sums. Notably, the 25% tax-free pension commencement lump sum is normally capped at 25% of the individual’s lifetime allowance (£268,275 if the individual is entitled to the standard lifetime allowance of £1,073,100).

Prior to 2023/24, if the value of benefit crystallisations exceeded the lifetime allowance, the excess was taxed at a flat 55% rate if the benefit taken was a lump sum, or 25% otherwise (e.g. if the excess was designated for flexi-access drawdown). The lifetime allowance charge was abolished by Finance (No.2) Act 2023 s 18 with effect from 6 April 2023, but other tax charges can apply in its place.

Under Finance (No.2) Act 2023 s 19, benefits that would have otherwise suffered a 55% lifetime allowance charge are instead treated as pension income of the recipient. The benefits affected by this rule are:

- serious ill-health lump sums;

- lifetime allowance excess lump sums;

- defined benefits lump sum death benefits; and

- uncrystallised funds lump sum death benefits.

For an additional rate taxpayer, this can effectively be a rate cut from 55% to 45%. The exact effect depends on the taxpayer’s particular circumstances, however. For example, the tax cost could be higher if the extra income reduces allowances. It could be lower if the individual has lower rate bands or tax reliefs available.

The 25% lifetime allowance charge was completely abolished, but in many cases, there will still be some tax due on the amount saved. For example, if the individual has £1 million in excess of their lifetime allowance that they choose to designate for flexi-access drawdown, doing this in 2022/23 would have resulted in a lifetime allowance charge of £250,000 and the remainder of £750,000 being available to withdraw as taxable income. In 2023/24, the full £1 million would be in the fund and available to withdraw as taxable income. The individual should still be better off than before, but the extra £250,000 will form part of any taxable income of the individual when they withdraw it.

Modification of lifetime allowance protections

Section 23 of Finance (No.2) Act 2023 provided for a significant relaxation in the ‘protection cessation events’ for enhanced protection and the three forms of fixed protection. Enhanced protection provides an exemption from the lifetime allowance charge, whereas fixed protection gives the individual a higher lifetime allowance than the standard amount. In both cases, the protections were lost if further pension savings were made, or certain other events occurred. These conditions could be problematic for those still in work, as they had to periodically opt out of workplace pension schemes to maintain their protections. Joining certain new death in service arrangements was also generally problematic.

With effect from 6 April 2023, protection cessation events only occur where the protection was claimed on or after 15 March 2023. The only affected protections that are still open for claims are fixed protection 2016 and enhanced protection. The latter can only be claimed where there is a reasonable excuse not to have claimed by 5 April 2009, so new claims are rare.

Individuals who claimed their protections before 15 March 2023 were free to resume participation in pension schemes from 6 April 2023 without losing protection. It was still possible to lose protection between 15 March and 5 April 2023, however, which may have caught out some taxpayers. Although loss of protection no longer results in a lifetime allowance charge, the lifetime allowance level remains relevant for some benefits taken in 2023/24 and for future benefits under the new regime from 6 April 2024.

Changes were also made to certain lump sum protections. Where individuals are entitled to higher tax-free lump sums than normal due to enhanced protection or stand-alone lump sum provisions, the tax-free amount was capped at the amount that could have been taken on 5 April 2023.

Reforms from 6 April 2024

In order to abolish the lifetime allowance, it was necessary for the government to design a new framework for pension benefits. Broadly, the goals of the reforms can be summarised as follows:

- keep the 25% tax-free pension commencement lump sum at the same level as before;

- tax other lifetime benefits at normal income tax rates; and

- prevent significant tax leakage that might otherwise arise in the absence of the lifetime allowance.

HMRC published draft legislation and a policy paper titled ‘Abolishing the pensions lifetime allowance’ for consultation on 18 July 2023 (see tinyurl.com/8a43adm6). The proposals went much further than the title suggested and included significant proposed reforms to the taxation of death benefits.

The draft legislation was substantially rewritten by the time it was published in the Autumn Finance Bill. Although the death benefit reforms were watered down, new charges were proposed on transfers to qualifying recognised overseas pension schemes (QROPS). The legislation is dense, and runs to about 100 pages, but the key takeaways are set out below.

The basic framework from 6 April 2024

Instead of the lifetime allowance, individuals will have two new allowances: a lump sum allowance; and a lump sum and death benefit allowance.

The default lump sum allowance is £268,275. This caps the amount that can be taken tax-free as pension commencement lump sums and/or the tax-free element of any uncrystallised funds pension lump sums.

The conditions that need to be met for a lump sum to be a pension commencement lump sum remain broadly the same as before. It is still the case that an amount equal to three times the lump sum must be used to provide pension income (e.g. designated for flexi-access drawdown).

The default lump sum and death benefit allowance is £1,073,100 (i.e. equal to the current lifetime allowance). This caps the amount that can be taken tax-free in aggregate during the individual’s lifetime and on death. This includes amounts counting towards the lump sum allowance, as well as the serious ill-health lump sums and most non-charitable lump sum death benefits for those who die under 75. For an individual who dies before age 75 holding only uncrystallised funds, this gives broadly the same outcome as under the current rules. The first £1,073,100 of the lump sum would be tax-free and the remainder would be taxed as income of the recipient.

Where the new rules differ from the old regime is where the lump sum is from a drawdown fund and the member dies before their 75th birthday. Under the current rules, the fund is tested against the lifetime allowance when it is designated for drawdown, but there is no further test on death. The fund can therefore be paid out tax-free, even if it has grown beyond the lifetime allowance. From 6 April 2024, the death benefit is only tax-free to the extent of the remaining lump sum and death benefit allowance, with the remainder being taxed as pension income of the recipient (although transitional rules may apply if the designation was made before 6 April 2024).

Effect of lifetime allowance protections

Where the individual is entitled to a higher lifetime allowance due to primary protection, individual protection or fixed protection, their lump sum allowance should be uprated accordingly. For example, someone with a lifetime allowance of £1.8 million due to fixed protection will have a lump sum allowance of £450,000. Similarly, their lump sum and death benefit allowance will be £1.8 million (i.e. equal to their lifetime allowance).

Enhanced protection is slightly different. As noted above, there is currently a cap on the pension commencement lump sum based on what could have been taken on 5 April 2023. The lump sum allowance will be based on this figure. The lump sum and death benefit allowance will be based on the value of the uncrystallised rights on 5 April 2024. Enhanced protection therefore will not protect future growth from tax charges.

Dependant, nominee and successor drawdown

One of the proposals put forward in HMRC’s July 2023 policy paper was the removal of the income tax exemption for pension income on funds from members who died before reaching age 75. This proposal has not been taken forward, so it will remain possible for unlimited amounts to pass tax-free if they are taken via dependant/nominee/successor drawdown rather than as a lump sum death benefits.

Transitional rules

Under the same July 2023 proposals,

pre-6 April 2024 tax-free benefits would have needed to be quantified to determine availability of the new allowances. This posed practical problems, as the pension providers might only know the percentage of lifetime allowance available rather than how past crystallisations were broken down. Under the revised provisions, when working out how much of the allowances are available for a crystallisation after 5 April 2024, the tax-free element of pre-6 April 2024 crystallisations is deemed to be 25% of the amount of lifetime allowance used. Where the taxpayer has complete evidence of the amount that was actually paid tax-free, they can apply for a certificate confirming the actual amount used. (This would be appropriate if the tax-free amounts were less than 25% of the amounts crystallised.)

Closure of protections and enhancements

Claims for fixed protection 2016 and individual protection 2016 will no longer be possible after 5 April 2025. Similarly, lifetime allowance enhancement factors that are currently available under Finance Act 2004 ss 220, 221 and 224 will close on 5 April 2025.

Changes to QROPS rules

Where a transfer is made from a registered pension scheme to a QROPS, the value is tested against the lifetime allowance. Previously this would have given rise to a 25% lifetime allowance charge on any excess. Without the lifetime allowance charge, there could be the potential for unlimited amounts to be transferred without any UK tax (assuming they were not subject to an overseas transfer charge).

From 6 April 2024, transfers will be tested against an overseas transfer allowance (equal to the lump sum and death benefit allowance), with the excess being subject to a 25% overseas transfer charge.

Conclusion

In straightforward cases where an individual starts to take their pension benefits after 5 April 2024, and the values are less than the lifetime allowance, the new regime will seem very similar to the old. For those who crystallise benefits both sides of 5 April 2024 it may be more complicated, and require far closer analysis, particularly if they have some older protections.

The transition will also have major consequences for pension providers who will not only need to adjust to a new regime quickly but are expected to provide statements to members by 5 April 2025 where benefits were taken under the old regime.