Reverse charge challenges

Share this article

Neil Warren goes back to basics to explain how and when the reverse charge system applies in the UK VAT system

Key Points

What is the issue?

In order to accurately record reverse charge entries on VAT returns, an understanding of how and why the rules apply is very important. The article considers the mechanics of the reverse charge, helped by practical examples.

What does it mean to me?

If you act for clients who only make exempt supplies, or who make taxable supplies below the VAT registration threshold, then the reverse charge rules on services purchased from abroad mean that they might need to register for VAT in some cases. It is important to understand how this process works in practice.

What can I take away?

Don’t forget that a reverse charge entry in Box 4 of a VAT return (input tax) must always consider whether any or all of the expense relates to exempt, private or non-business activities. If the answer is ‘yes’, then the input tax claimed must be blocked or reduced accordingly.

A radical reverse charge system was due to be introduced for the construction industry on 1 October 2019; however, it was cancelled at the eleventh hour to give businesses an extra 12 months to prepare for the new rules.

There is no doubt that many advisers find the principles of the reverse charge very difficult to grasp. I even remember sitting with one accountant during a cricket match who was trying to work the charge out by means of old-fashioned T-accounts!

Therefore, in this article I will consider some practical examples of how the reverse charge works in practice, and also the purpose behind these procedures, which are an important part of the UK VAT legislation.

Reasons for having a reverse charge system

The main outcome of the reverse charge process is that the customer does not pay VAT to the supplier but instead declares output tax on their own VAT return in Box 1. There are two main reasons why this procedure is adopted:

- Services purchased from abroad: If a UK customer buying taxable services from abroad accounts for output tax on a supply, it avoids overseas suppliers having to get UK VAT registration numbers, which would be a time consuming and unnecessary burden for the supplier.

- Anti-fraud measure: The logic in other reverse charge situations is simple: if a UK supplier is not paid 5% or 20% VAT in the first place by his customer, and the customer declares the output tax on his own VAT return instead, the supplier cannot disappear into the wilderness without declaring and paying output tax to HMRC on a VAT return. The tax yield therefore increases as a result of the reverse charge mechanism. HMRC have introduced the reverse charge to trade sectors, where they consider missing trader VAT fraud to be a major problem.

Services purchased from abroad

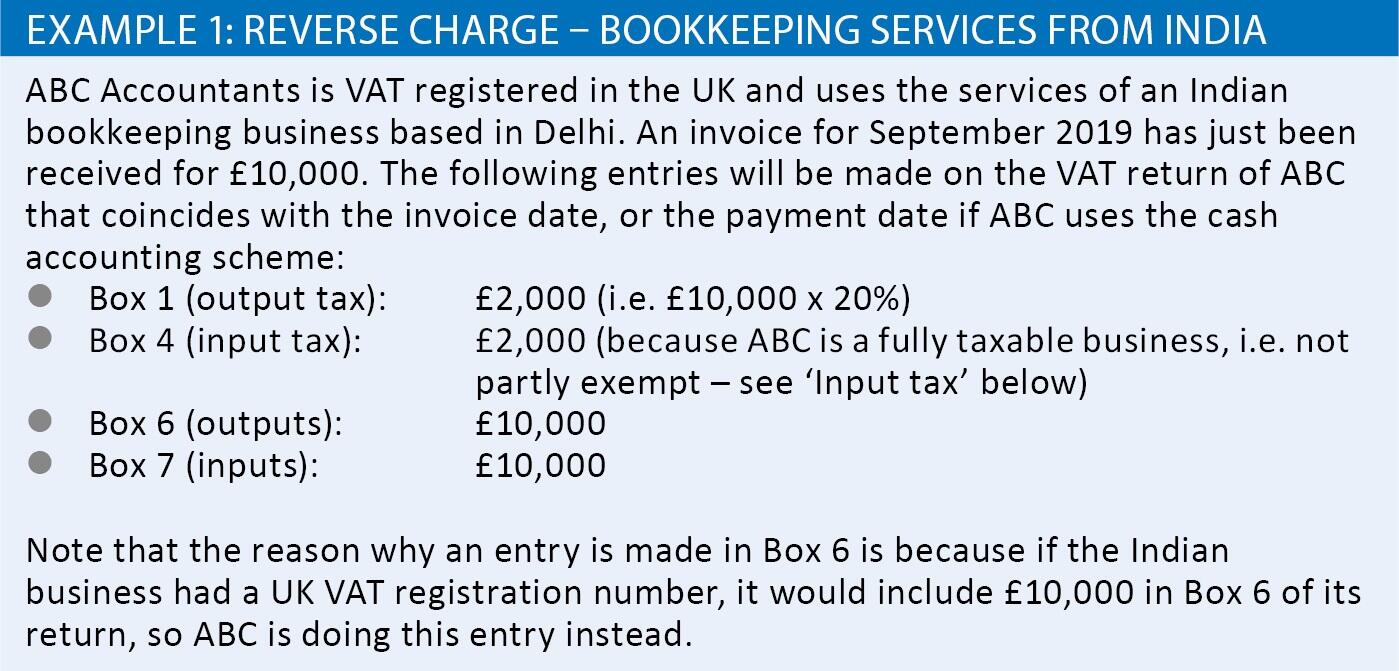

An important opening tip is given in the subtitle, namely that the reverse charge applies to services received from abroad and not just from EU suppliers. To understand the workings of the process, see Example 1: Reverse charge – bookkeeping services from India.

The logical way to look at the figures in this example is to consider what VAT return entries would have been made if the legislation required the Indian bookkeeper to get a UK VAT number.

The bookkeeper would charge and be paid £2,000 VAT from ABC and include this amount in Box 1 of its return, also recording the net sale in Box 6,

i.e. £10,000.

ABC would then claim input tax in Box 4, again £2,000, with the net purchase being included in Box 7. So, with the reverse charge system, the same boxes are being completed but the Box 1 and Box 6 entries move from the supplier to the customer. That is the reverse charge system in a nutshell.

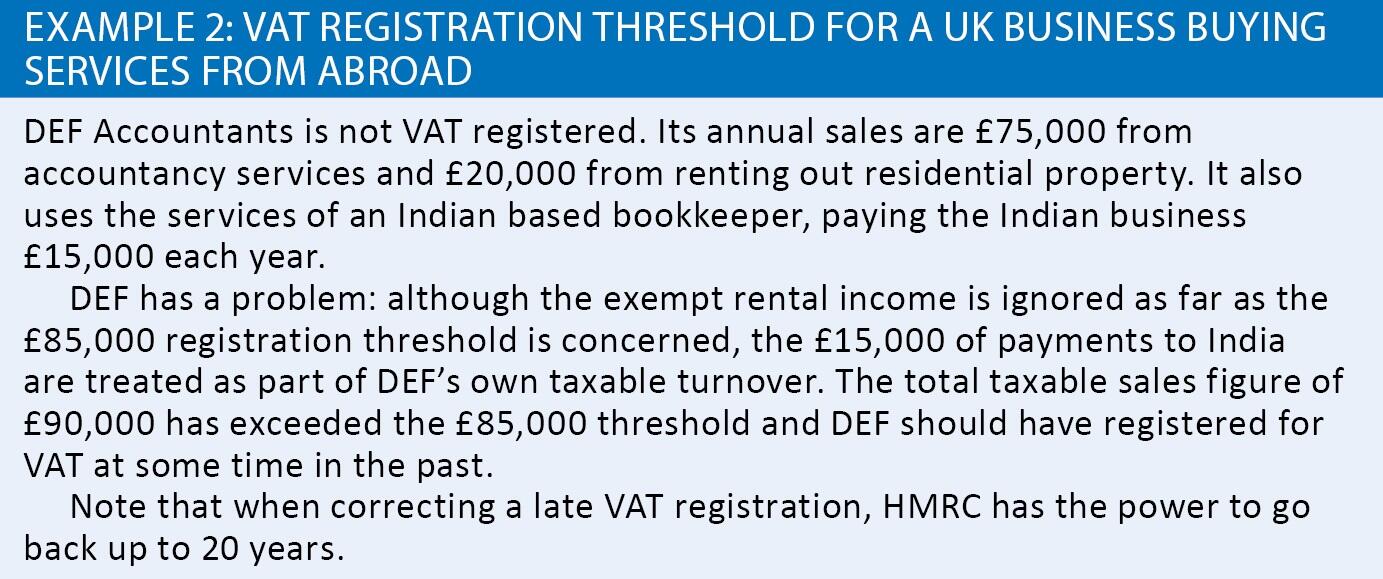

VAT registration threshold

A twist to the tale that applies to services purchased from abroad but not in other reverse charge situations is that the payments made to overseas suppliers form part of the £85,000 VAT registration threshold for an unregistered UK business.

This assumes that the service in question would be VATable in accordance with UK legislation, i.e. not exempt from VAT. This outcome often causes a raising of the eyebrows: how can expenditure be included in a test that is always based on sales?

See Example 2: VAT registration threshold for a UK business buying services from abroad.

The reason that this bizarre outcome forms such an important (and often underestimated) part of our VAT system is because it prevents exempt businesses from buying VAT free services from overseas suppliers, instead of paying a UK supplier 20% VAT that cannot be reclaimed. In other words, the rules help to ensure that a level playing field is achieved and the system does not work against UK suppliers. I will extend this principle in the next section about ‘input tax’.

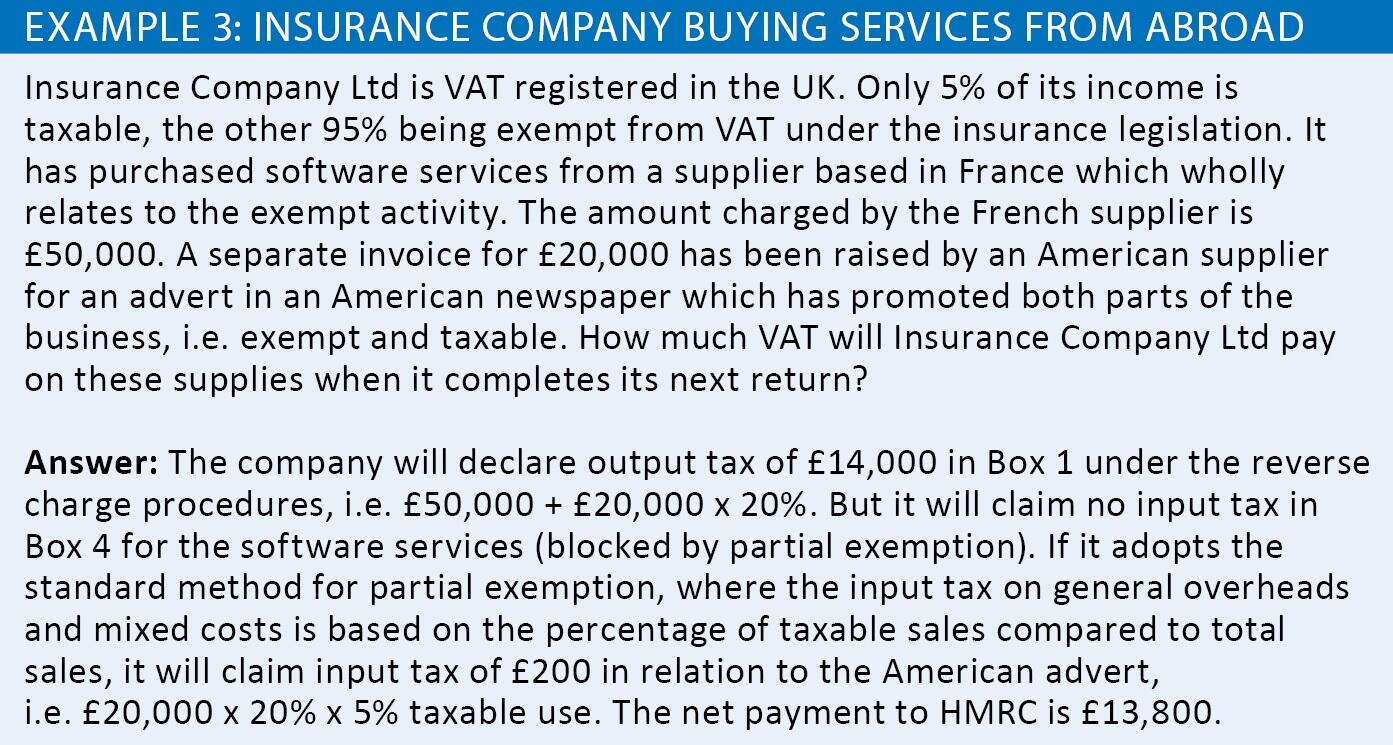

Input tax

A common myth (or misunderstanding) is that the Box 4 entry for input tax is always the same as the Box 1 entry for output tax. It is not!

When UK customers make reverse charge entries on their VAT returns, they must put the Box 4 entry through exactly the same tests as they would with the VAT on a domestic purchase invoice that has been received from a UK supplier:

- Does the supply include any non-business or private use element?

- Does it partly or wholly relate to exempt supplies?

If the answer to either of the above questions is ‘yes’, then input tax needs to be restricted. In other words, the Box 1 output tax declaration will exceed the Box 4 input tax claim, producing a net VAT payment to HMRC.

See Example 3: Insurance company buying services from abroad.

Anti-fraud reverse charge situations

Other reverse charge situations in the legislation focus on particular industries, with an anti-fraud motive being the reason for their introduction. The principles for domestic supplies captured by the reverse charge are mainly the same as for overseas services, the main outcome being that VAT is still declared by the customer and not the supplier. But an important difference is that the rules are only relevant if both the customer and supplier are VAT registered. The affected trade sectors for domestic reverse charge supplies are set out below:

- Suppliers of ‘specified goods’:

- mobile phones and computer chips with effect from 1 June 2007; and

- wholesale gas and wholesale electricity with effect from 1 July 2014.

- Suppliers of ‘specified services’:

- emission allowances from 1 November 2010;

- wholesale telecommunications from 1 February 2016;

- renewable energy certificates from 14 June 2019; and

- construction services between builders from 1 October 2020.

The suggested strategy if you have clients in the above sectors is to review HMRC’s VAT Notice 735 and refer to the relevant section allocated for each category. For example, supplies involving mobile phones and computer chips are only subject to the reverse charge if the invoice value exceeds £5,000 excluding VAT (VAT Notice 735 s 6).

Invoicing by suppliers

An important feature of reverse charge supplies made by UK suppliers is that suppliers need to check the VAT status of their UK customers, e.g. to be satisfied that the customer is properly registered for VAT with a genuine VAT number. In reality, it all comes down to knowing and understanding your customers. And the other important issue is that sales invoices raised by suppliers that are subject to the reverse charge should include a clear message to the customer to account for output tax under the reverse charge procedures.